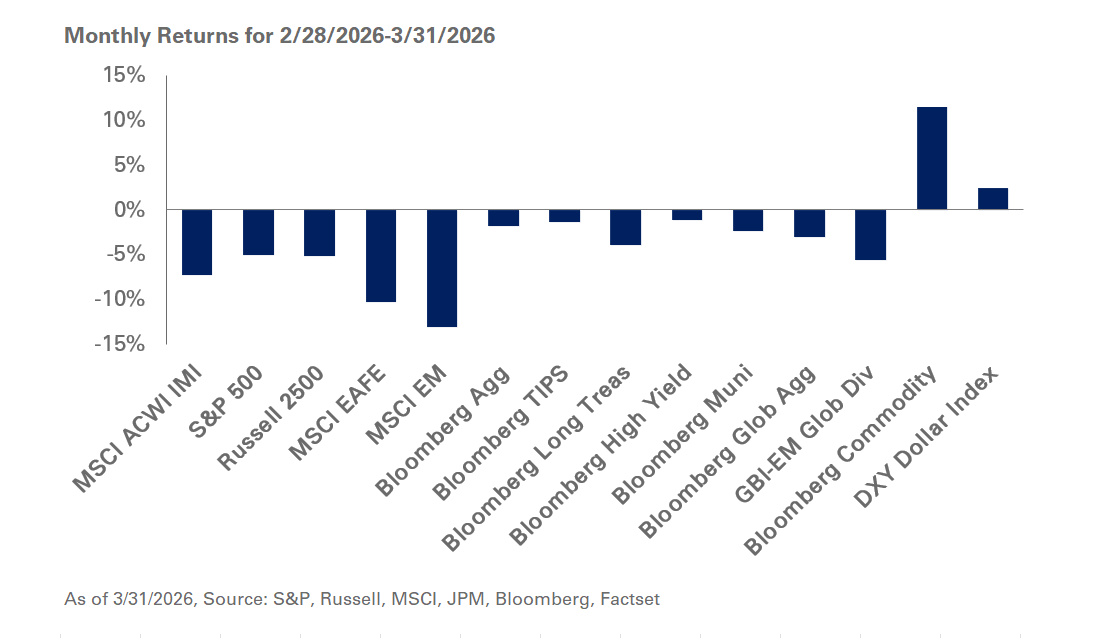

Markets were roiled in March as geopolitical tensions escalated amid the war in Iran. Oil prices spiked 51% last month, finishing at just about $100 a barrel, amid heightened uncertainty around the fate of the Strait of Hormuz, a waterway that is a key point of contention and leverage as it ferries a third of global crude oil to mostly Asia. Energy markets will likely remain volatile as tensions and agreements evolve for the remainder of the conflict. Equities declined sharply in March, weighed down by rising energy prices; industrials and consumer discretionary sectors were the hardest hit, down 8.4% and 7.3%, respectively. Value held its own against growth, helped by higher prices in the energy sector. The S&P 500 was in the red, down 5% while non-U.S. developed and emerging markets stocks fell double-digits due to their greater vulnerability to higher energy prices.

On the macroeconomic front, inflation data showed moderate price increases with CPI up 2.4% in February. Unemployment data remained stable, though job growth appeared subdued. GDP growth for the fourth quarter of 2025 was revised lower to 0.7% from an initial estimate of 1.4%. Meanwhile, the Federal Reserve kept the federal funds rate unchanged for the second straight meeting.

In fixed-income markets, the Bloomberg U.S. Aggregate Bond Index posted losses as yields rose amid uncertainty around the higher cost of energy and its impact on inflation. Fed funds futures markets reversed course, pricing in 0 cuts by the end of March from the earlier anticipated three cuts.

The yield on U.S. 10-year Treasury notes rose to 4.32% in March, along with global yields across Europe and Japan rising 20 to 60 basis points. We advocate maintaining exposure to equities and seeking opportunities to rebalance across market segments should stocks materially under- or out-perform. We also recommend investors remain disciplined and stick to long-term strategic asset allocation targets. Within equity portfolios, we suggest balancing exposure of the earnings power from the largest S&P 500 names with value and quality companies across the globe.

However, we advise being mindful of portfolio equity positions and monitoring outsized tracking error levels associated with the top 10 index

names of ACWI IMI. Furthermore, we advise investors hold high-quality liquid assets and stay underweight to non-investment grade public debt, so as to have appropriate safe-haven fixed-income exposure to maintain liquidity and for downside protection.