Geopolitical tensions roiled markets in the first quarter of 2026 as the United States and Israel waged a war on Iran, sending equity markets lower, fixed-income yields higher while disrupting global energy supplies. The price of oil shot above $100 a barrel, driving costs higher across the energy complex. The spike in energy prices flowed through the economy with the Consumer Price Index posting a 0.9% rise in March; still, broader inflation measures remained relatively muted with Core CPI (ex-food and energy) increasing only 0.2% for the month.

That said, market volatility in April appears to be stabilizing with equities rallying as the market holds out hope for a lasting truce. Should we see a resumption of military strikes with greater breadth, markets are likely to experience an accelerated drawdown, especially in the event of a significant attack by Iran or the U.S. on oil or natural gas facilities in the region.

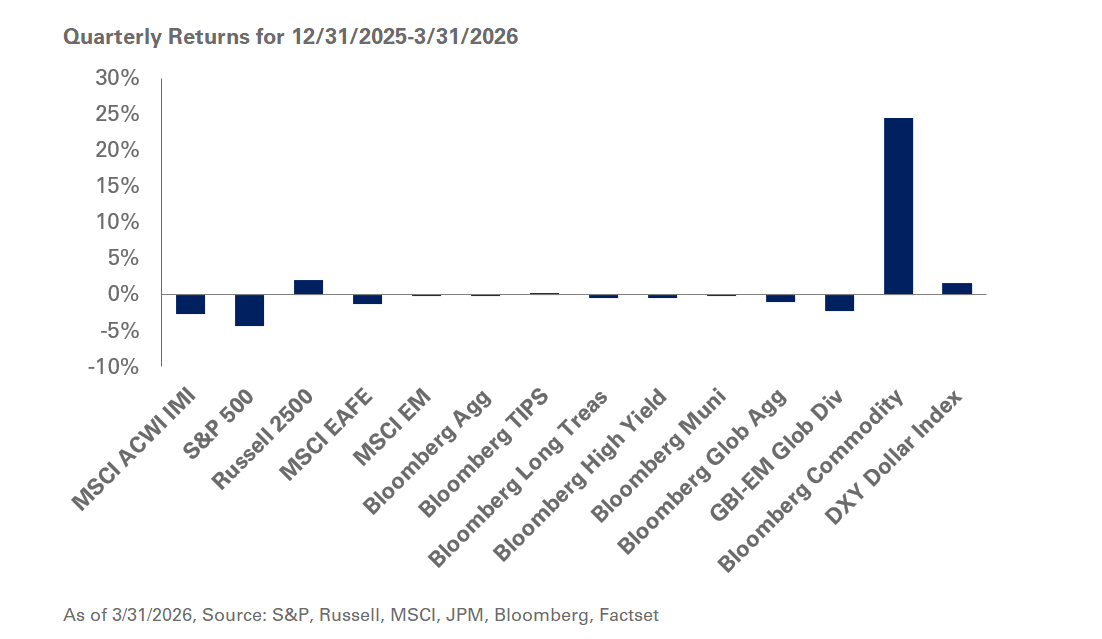

For the three months ended March 31, equity markets were broadly lower with a few bright spots. The S&P 500 ended the quarter down 4.3% with sentiment shifting lower amongst AI names along with the market drawdown associated with the war in Iran. However, value in the U.S. remained in the black with large-caps and small-cap value stocks posting returns of 2.1% and 5%, respectively.

Markets outside the U.S. bore the brunt of the negative price pressures due to the war in Iran with some European and Asian markets down more than 10% in March. While both MSCI EAFE and emerging market stocks performing well in the first two months of the year, they ended the quarter in the red, down 1.2% and 0.2%, respectively.

Fixed-income markets were also challenged in the first quarter as inflation concerns, a rising U.S. dollar, and a liquidity squeeze pushed government bond yields higher across the world. 10-year Treasury yields were 15 basis points higher for the quarter, ending the period with a yield of 4.3%. Outside the U.S., yields on German, British and Japanese bonds moved even higher. U.S. TIPS were in the black in the first quarter, up 0.3%, according to the Bloomberg U.S. TIPS Index. Credit markets were also weighed down by the shift in market sentiment, with the U.S. High Yield and U.S. Credit indexes posting losses of 0.5% for the quarter. Credit spreads for investment-grade and high-yield bonds saw an uptick, rising 11 basis points and 50 basis points, respectively.

Meanwhile, public real assets led performance with the price of WTI Oil up more than 75% for the three months ended March 31; during this period, the Bloomberg Commodity Index posted gains of 24%. Gold remained positive for the quarter, earning 8% despite the double-digit drawdown in March. With the outsized performance of real assets, we encourage investors with a dedicated allocation to public real assets to rebalance exposures back to strategic targets as market conditions are likely to remain fragile in the space.

We also recommend investors remain disciplined and stick to long-term strategic asset allocation targets. We advocate maintaining exposure to equities and seeking opportunities to rebalance across market segments should stocks materially under- or out-perform. Within equity portfolios, we suggest balancing exposure of the earnings power from the largest S&P 500 names with value and quality companies across the globe. However, we advise being mindful of portfolio equity positions and monitoring outsized tracking error levels associated with the top 10 index names of ACWI IMI. Furthermore, we prefer investors hold high-quality, liquid assets, and are underweight non-investment-grade public debt, and maintain appropriate safe-haven fixed-income exposure for liquidity and downside protection.