A growing wave of mega-IPOs is forcing index providers—and investors—to rethink their views on inclusion timing, liquidity and concentration risk.

Index rules are becoming a major market force as companies stay private longer and potentially list at increasingly large valuations. These trends are upending traditional index inclusion frameworks built around seasoning periods, float thresholds and periodic rebalancing. This shift is about flows, and not fundamentals. With nearly $30 trillion1 benchmarked to major indexes globally—including approximately $27.7 trillion tied to S&P Dow Jones indexes alone—we believe inclusion timing can generate large, mechanical demand shocks. A single mega-IPO can quickly become a top index weight, exacerbating risks around index concentration, and reinforcing factor and sector tilts. At NEPC, we urge investors to be mindful of the impact of these mega-IPOs on portfolios.

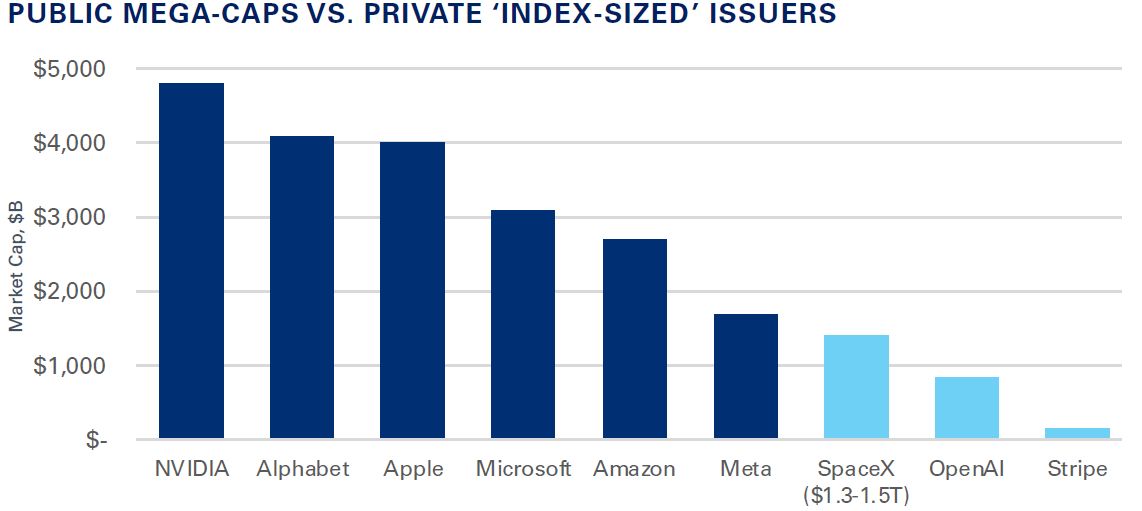

The Pipeline: Large, Private and Index-Sized

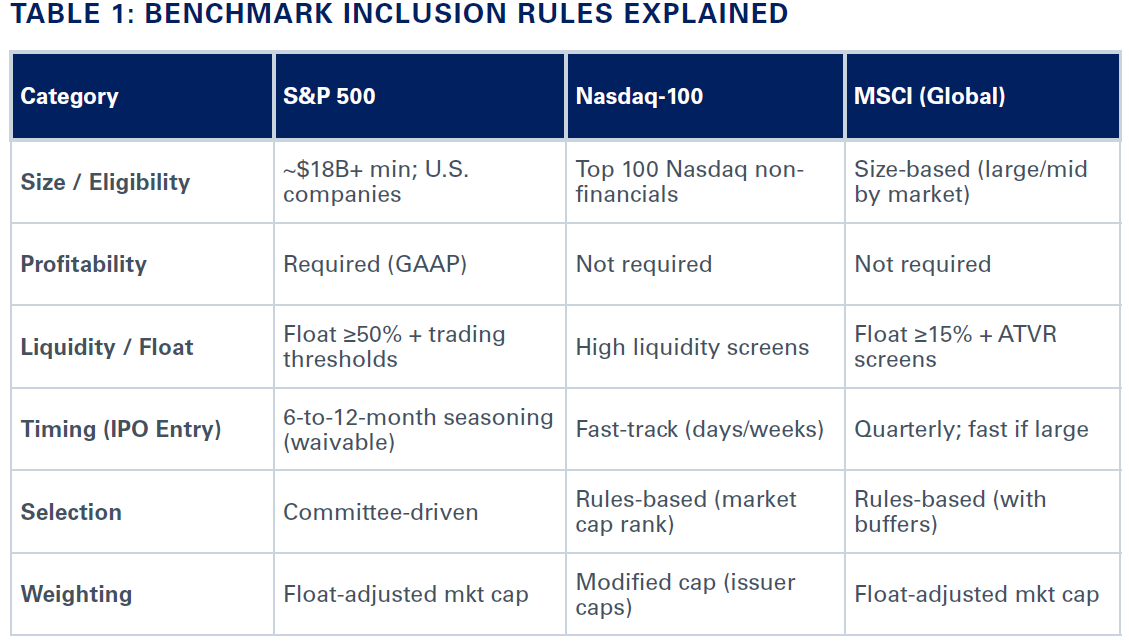

Historically, index providers balanced representation with implementation by requiring seasoning periods and minimum float thresholds to support reliable price discovery and appropriate liquidity (Table 1). That balance is shifting with accelerated inclusion proposals that not only reduce seasoning periods—potentially to as little as ~15 trading days—but also lead to the recalibration of the treatment of float and market capitalization in determining eligibility and weighting. At NEPC, we anticipate IPO activity will be stronger at the larger end of the market given a backlog of IPO-ready companies2 that suggests issuance could accelerate in 2026, particularly if macro conditions remain supportive. If this dynamic plays out, it will be important to pay attention to whether large deals crowd out smaller offerings or delay broader IPO activity, potentially introducing capacity constraints at the market level—not just within indexes. Many prospective issuers already exhibit free-float-adjusted market capitalizations and scale characteristics consistent with large-cap index constituents3 while still private. For example, SpaceX is currently valued in the ~$1.3 trillion-to-$1.5 trillion range based on indications from the secondary market, placing it within the upper echelon of global large-cap equities on a pro forma basis. Anthropic, by contrast, is valued in the ~$20 billion-to-$40 billion range, consistent with a mid-to-upper tier large-cap index entrant on initial inclusion. Alongside peers such as OpenAI, Databricks and Stripe, these firms could enter public markets with index-relevant notional market capitalizations but constrained free float, creating a potential divergence between headline index weight and investable capacity under MSCI- and S&P-style float-adjusted methodologies.

Sources: S&P Dow Jones Indices, Nasdaq Indices, FactSet, Pitchbook as of March 31, 2026

In response, index providers, including Nasdaq and S&P Dow Jones Indexes, are revisiting eligibility frameworks and inclusion timelines. Nasdaq has implemented a ‘fast entry’ rule enabling large, highly liquid IPOs to join the Nasdaq-100 within ~15 trading days4, while S&P is actively evaluating potential adjustments to its more stringent, discretionary inclusion process5.

Sources: S&P Dow Jones Indices methodology, Nasdaq index rules, MSCI Global Investable Market Index framework, and public index documentation.

What’s Changing: From Delayed Inclusion to Engineered Acceleration

In practice, we have observed index methodologies evolving to accommodate low-float mega-IPOs rather than constrain them. In some cases, eligibility may increasingly reflect total economic size, including insider and unlisted shares, while still requiring execution in a smaller tradable float. This underscores a growing disconnect between index weights and investable supply.

These changes are not purely technical; they also reflect competitive dynamics among index providers, including S&P Dow Jones indexes and FTSE Russell, as benchmarks compete to remain relevant and capture flows associated with high-profile listings.

Accelerated inclusion places liquidity and float dynamics at the center of index construction. We see the core tension as straightforward: index weights are determined by total market capitalization, while execution must occur within the constraints of available float for that specific stock. Active managers retain flexibility to stage entry and manage liquidity, while passive vehicles, by design, must execute on the index provider’s timetable. When passive funds are required to buy a large percentage of a limited float within a compressed timeline, buying pressure is concentrated on a small share base and upward price moves can be amplified—particularly if dealer balance sheets are constrained and price discovery is still developing.

One could imagine a scenario in which significant upward price moves triggered by market enthusiasm around these mega-IPOs could result in an increase in the price of the stock. In such a scenario, the weight of the stock in the index could force even more buying by index providers, thereby creating the reflexive loop that supports index concentration. For passive and tracking-sensitive mandates, this has the potential to raise implementation risk. Shorter timelines can increase turnover, widen spreads, and elevate market impact. At the same time, predictable inclusion rules create opportunities for anticipatory positioning by both systematic and discretionary investors, concentrating risk around event windows.

Index Concentration Amplified

Concentration is already a defining risk of indexes today, and the inclusion of mega-IPOs could further magnify these risks moving forward. Large entrants can reach top index weights quickly, as seen in the rapid weight accretion following Tesla’s inclusion6, and benchmark exposures can shift mechanically rather than through active allocation decisions. A wave of mega IPOs could increase sector weights through index rules alone, reinforcing existing factor tilts and crowding dynamics. More specifically, we would expect broad market indexes to become further tilted towards software, aerospace and defense, likely at the expense of financials, industrials and energy.

The issue is not whether mega-IPOs belong in an index, but what happens when benchmarks seek to remain representative while incorporating companies with massive valuations and constrained free float. Accelerated inclusion effectively pulls passive demand forward, forcing execution against limited liquidity and compressing price discovery. The result is a potential transfer of liquidity risk, trading cost, and early-life volatility onto index holders which need to be fully understood. Index rules are no longer just back-end mechanics.

In a market dominated by benchmarked capital, they function as an active lever—capable of moving prices, reshaping concentration, and altering portfolio risk at a much faster pace than many investors anticipate. Given these evolving dynamics, NEPC Research urges investors to be mindful of the major impacts from these mega-IPOs:

- Market concentration, and its follow-up impacts, may continue. Investors need to be wary of navigating a narrow U.S. market and stay cognizant of taking the right type of active risk

- Concentrated benchmarks present a dilemma for investors on whether they should invest passively and accept stock concentration, or invest actively and accept tracking error

- Index funds come with their own risks, and it is important for index holders to understand how these passive investments may tilt the portfolio towards a certain sector or factor bias. NEPC’s Portfolio Construction specialists help our clients understand total portfolio exposures and tilts, so our clients can be sure they understand their investment program holistically

- The convergence of public and private markets is a continuing theme and the impact of these mega-IPOs on public markets is an example of that. Stay tuned for a piece from NEPC’s Private Markets group that tackles the current state of the private markets and our IPO outlook for 2026 and beyond.

If you have questions on the potential impact of mega-IPOs and fast-track index inclusion on your investment portfolio, please reach out to your NEPC consultant

If you have questions on the potential impact of mega-IPOs and fast-track index inclusion on your investment portfolio, please reach out to your NEPC consultant.

Sources

1 S&P Dow Jones Indices, Annual Survey of Indexed Assets (2024), reporting approximately $27.7 trillion benchmarked to its indices globally.

2 “IPO-ready companies” refers to late-stage private firms with the scale, audited financials, governance, and investor backing required for public listing, including established revenue models and readiness for SEC reporting and public market scrutiny.

3 “Index-sized” refers to companies whose pro forma free-float-adjusted market capitalization would place them within the large-cap universe of major equity indices such as the S&P 500 or MSCI USA Index, and whose scale is sufficient to materially affect index weights upon inclusion, subject to float adjustment, liquidity screens, and other investability criteria defined by index providers (e.g., S&P Dow Jones Indices and MSCI methodology frameworks).

4 Nasdaq has introduced a “fast entry” rule allowing certain large, highly liquid IPOs to be considered for inclusion in the Nasdaq-100 Index within approximately 15 trading days of listing; see Reuters, “Nasdaq rules to speed entry of new listings into benchmark index” (2026).

5 S&P Dow Jones Indices maintains more stringent eligibility requirements for the S&P 500, including seasoning and profitability criteria, and has indicated it is evaluating potential adjustments to its inclusion framework; see S&P Dow Jones Indices methodology documents and Morningstar, “How Indexes Will Adapt to Mega-IPOs” (2026).

6 Research Affiliates, Tesla, the Largest-Cap Stock Ever to Enter S&P 500: A Buy Signal or a Bubble? (2020).