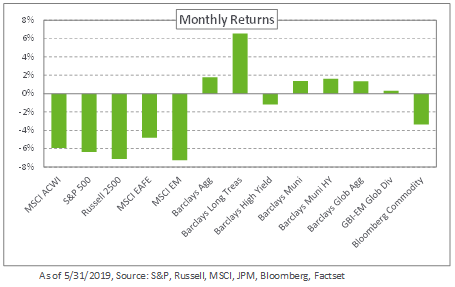

It appears markets were ready to take off for the summer as the “sell in May and go away” adage took effect. Equities declined across the board amid renewed concerns around US trade policy. The S&P 500 Index came off its record high, losing 6.4% in May; emerging market equities lost even more, falling 7.3%, according to the MSCI Emerging Markets Index, as a stronger US dollar also took a bite out of returns.

The flight-to-quality led to a decline in global yields and a subsequent rally in safe-haven assets. In the US, 10- and 30-year Treasuries declined 36 and 35 basis points, respectively. The movement in longer-dated yields caused parts of the yield curve to invert – specifically at the 10-year, 3-month and 10-year, 1-year points. As a result, the Barclays US Treasury Index and Barclays Long Treasury Index increased 2.4% and 6.5%, respectively, during the month. In credit, spreads widened with the Barclays US High Yield Index experiencing the largest change, increasing 75 basis points to 4.33%, leading to a monthly decline of 1.2%.

Within real assets, spot WTI Crude Oil reversed recent gains, falling 16.2% to $54 amid concerns on the potential impact of tariffs on the demand for oil. Despite its losses in May, WTI Crude Oil is up 18.5% for the year.

We believe volatility is likely here to stay as the US administration revisits the issue of tariffs and the economy advances to the late stage of the market cycle. To this end, we remind clients to stay committed to a risk-balanced approach and to evaluate market opportunities should larger short-term dislocations occur.