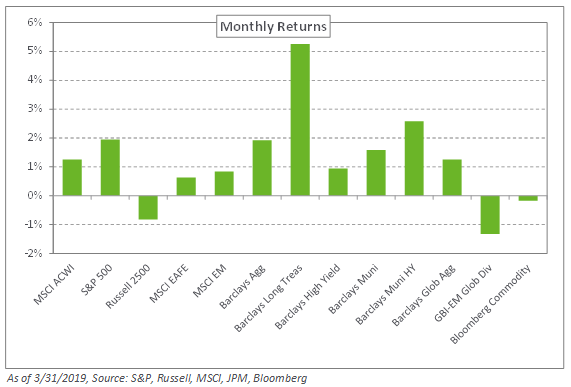

Following the market rout at the end of 2018, equities made a strong comeback in the first quarter. Risk assets pushed higher as the Fed signaled no additional rate hikes in 2019. The US led the way, with the S&P 500 Index increasing 1.9% in March; international and emerging market equities were also in the black, with the MSCI EAFE and MSCI Emerging Markets Indexes up 0.6% and 0.8%, respectively.

The dovish pivot by the Fed also bolstered fixed-income returns, broadly causing yields to decline. In the US, a segment of the yield curve—measured by the spread between the 10-year Treasury note and 3-month Treasury bill—inverted. By the end of the month, the inversion had reversed, even as the 10-year US Treasury yield declined 30 basis points to 2.42%. Meanwhile, 10-year German and Japanese bond yields fell 0.26% and 0.07%, respectively – both ending in negative territory. Within credit, spreads continued to tighten with the Barclays US High Yield spread declining 1.35% to 3.91%, which corresponded to an index return of 0.9%. In emerging markets, local debt, as measured by the JPM GBI-EM Global Diversified Index, fell 1.3% with modest currency depreciation relative to the dollar.

In real assets, spot WTI Crude Oil maintained its rally, increasing 5.2% during the month and up 33.3% for the quarter. Additionally, midstream energy benefitted from higher oil prices, which fueled a 3.4% increase in the Alerian MLP Index in March.

With the US advancing into the late stage of its expansionary economic cycle, we remind investors of the importance of diversification given the more pronounced risks and volatility historically associated with this stage. As such, after a strong first quarter for risk assets, we encourage investors to consider rebalancing recent equity gains and increasing safe-haven fixed-income exposure.