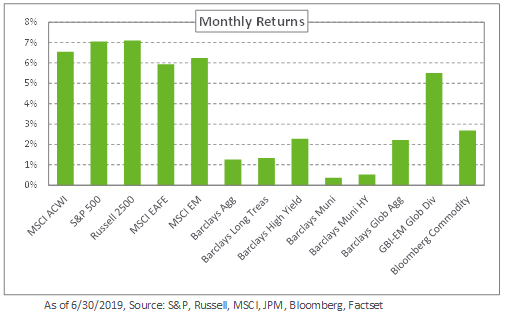

Reversing their sharp declines from a month earlier, equities posted strong gains in June on the back of a more accommodative pivot from global central banks responding to muted inflation, ongoing trade concerns and weakening economic data. The S&P 500 Index hit a record high, up 7.0% for the month and 4.3% for the quarter. Outside the US, the MSCI EAFE and MSCI Emerging Market indexes increased 5.9% and 6.2%, respectively, while also benefitting from a weaker dollar.

The rally also extended to fixed income with most global bond indexes in the black last month. Global rates continued to decline with the 10-year and 30-year US yields falling 14 basis points and six basis points, respectively. In Germany and Japan, 10-year yields fell further to -0.44% and -0.16%, respectively, underscoring a resurgence in negative-yielding debt in many parts of the developed world. In credit, spreads fell across the board with the largest decline in lower-rated debt. The Barclays US High Yield Index spread declined 56 basis points to 3.77%, resulting in gains of 2.3% for the month. In emerging markets, local currency debt rallied, with the JPM GBI-EM Global Diversified Index up 5.5% in June, as currencies broadly strengthened against the dollar.

Within real assets, spot WTI Crude Oil increased 9.2% to $58, bringing year-to-date gains to 29.4%.

While renewed support from the central bank may lengthen the economic expansion in the United States, we believe it remains firmly placed in the late-stage of the market cycle. To this end, we remind investors of the importance of diversification given the more pronounced risks and volatility historically associated with this stage of the cycle. Considering the robust performance of equities, we encourage rebalancing stocks with a preference towards emerging market equities and reducing exposure to lower-quality credit.