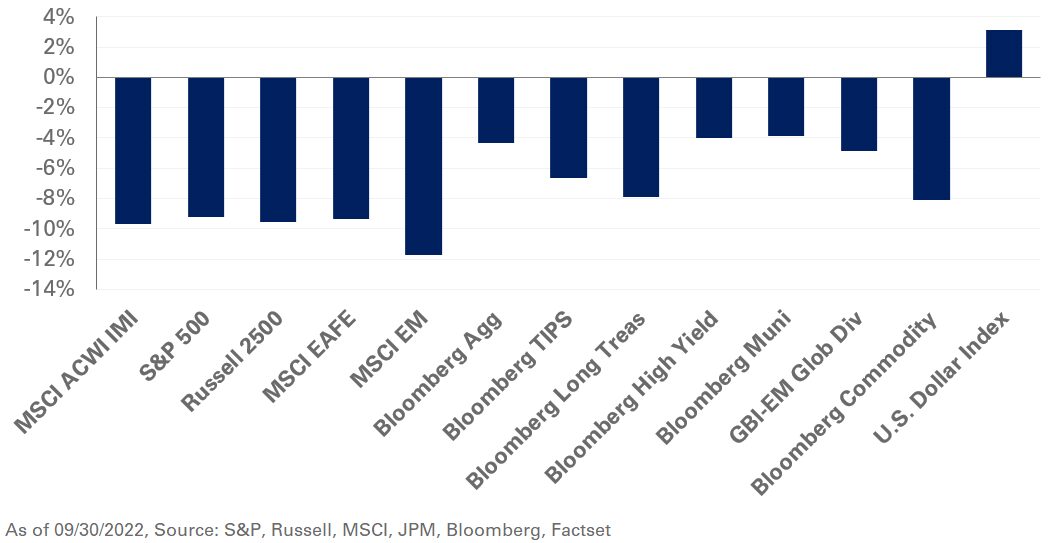

Equities continued their downward slide in September as central banks around the globe reiterated their commitment to tighter monetary policies amid persisting inflationary pressures despite softening economic growth. In the U.S., the S&P 500 Index plummeted 9.2%, fueling year-to-date losses of 23.9%. Value stocks outperformed growth equities with the Russell 1000 Value Index falling 8.8%, while the Russell 1000 Growth Index declined 9.7%. Emerging market equities, down 11.7%, underperformed all other regions.

Within fixed income, the yield curve flattened with 10- and 30-year Treasury yields rising 67 and 52 basis points, respectively. The 10-year German Bund yield also increased 59 basis points to 2.13% amid inflationary pressures in the Eurozone.

In real assets, commodities experienced another volatile month amid concerns around weakening global demand and supply constraints. Notably, spot WTI Crude Oil fell 11.8% in September to $79 per barrel.

NEPC’s stance towards risk assets remains unfavorable given the uncertain dynamics around growth and inflation. We recommend building exposure to short-term investment-grade credit as higher yields offer an attractive defensive position. We also suggest adding exposure to value stocks in U.S. large-cap equity to mitigate the portfolio impact of rising interest rates and inflation normalizing above market expectations. In addition, we still encourage a dedicated allocation to assets that support liquidity needs in periods of stress.