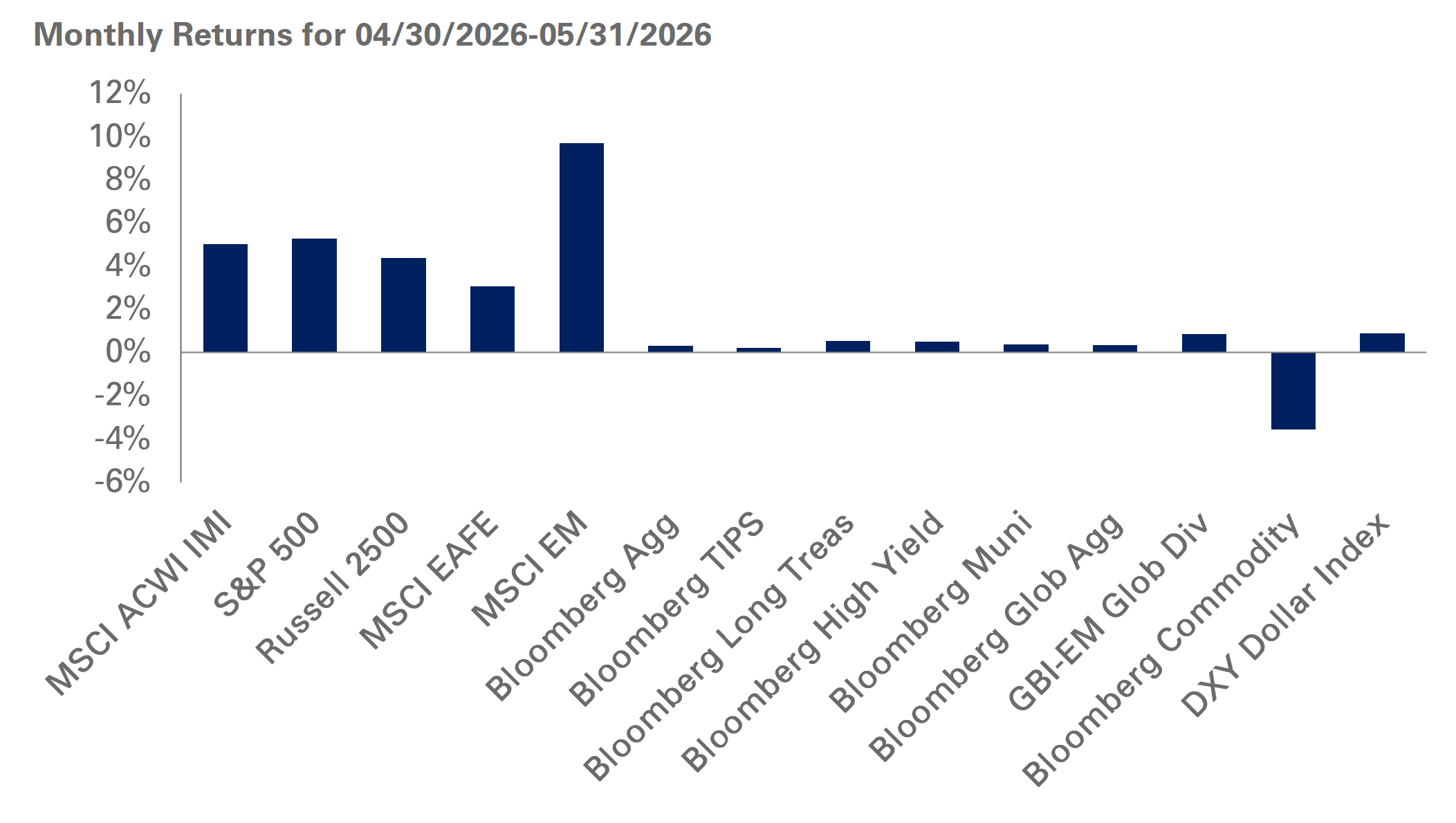

Global equities further cemented gains in May on the heels of robust corporate earnings and optimism towards the back end of the month around a potential U.S.-Iran peace deal. While geopolitical headlines fueled intra-month volatility across markets, a backdrop of resilient economic and corporate earnings data continued to support returns. Companies in the S&P 500 Index posted a blended earnings growth rate of nearly 29% with the technology sector leading the way. In response, the S&P 500 Index hit a record high in May, adding gains of 5.3%. With continued momentum around AI, growth markets strongly outperformed value: the Russell 1000 Growth Index added 7.2% in May—pushing quarter-to-date returns above 20%—while the Russell 1000 Value Index lagged with returns of 2.9%.

The momentum in AI and strong earnings also buoyed markets outside the U.S., particularly in Asia. The MSCI Emerging Markets (EM) Index added 9.7% in May, led by a 35% gain in Korean equities. While China still represents over 20% of the MSCI EM Index, the country ranked among the worst performing in May, falling 3% given a string of lackluster economic data reflecting a weak domestic economy.

Meanwhile, Treasury yields were especially volatile last month as markets reacted to headlines around Iran and a fresh batch of inflation data showed continuing price stressors across the U.S. economy. In response, markets priced in tighter policy expectations, with the probability of a 2026 rate hike by the Federal Reserve hovering near 45% at month-end. Despite these headwinds, signs of a de-escalation in geopolitical tensions in the final days of the month helped temper pressure on bond yields. Notably, the 30-year Treasury yield ended at 4.98%, down just one basis point in May, after briefly touching 5.22% mid-month. Credit spreads also tightened modestly during this period, fueling 0.7% and 0.5% monthly gains in the Bloomberg U.S. Corporate and U.S. High Yield indexes, respectively.

Finally, public real assets continued their volatile streak. Spot WTI crude oil ended around $87 per barrel – down nearly 20% for the month – reflecting easing supply concerns related to the Strait of Hormuz. The weakness in the energy sector cascaded across the commodity complex, causing the Bloomberg Commodity Index to post a 3.6% loss for the month.

While the geopolitical backdrop remains a source of volatility for markets, robust corporate earnings and resilient economic data continue to provide a supportive environment for growth. We advise investors look past day-to-day headlines, and suggest fully utilizing the portfolio risk budget, while staying close to strategic target levels. Within equities, we recommend investors are mindful of portfolio underweights and outsized tracking error levels relative to the top names in the MSCI ACWI IMI and the S&P 500 indexes. We encourage investors to hold high-quality, liquid assets such as safe-haven fixed-income securities at strategic target levels to support portfolio liquidity.

As of 5/31/2026, Source: S&P, Russell, MSCI, JPM, Bloomberg, Factset