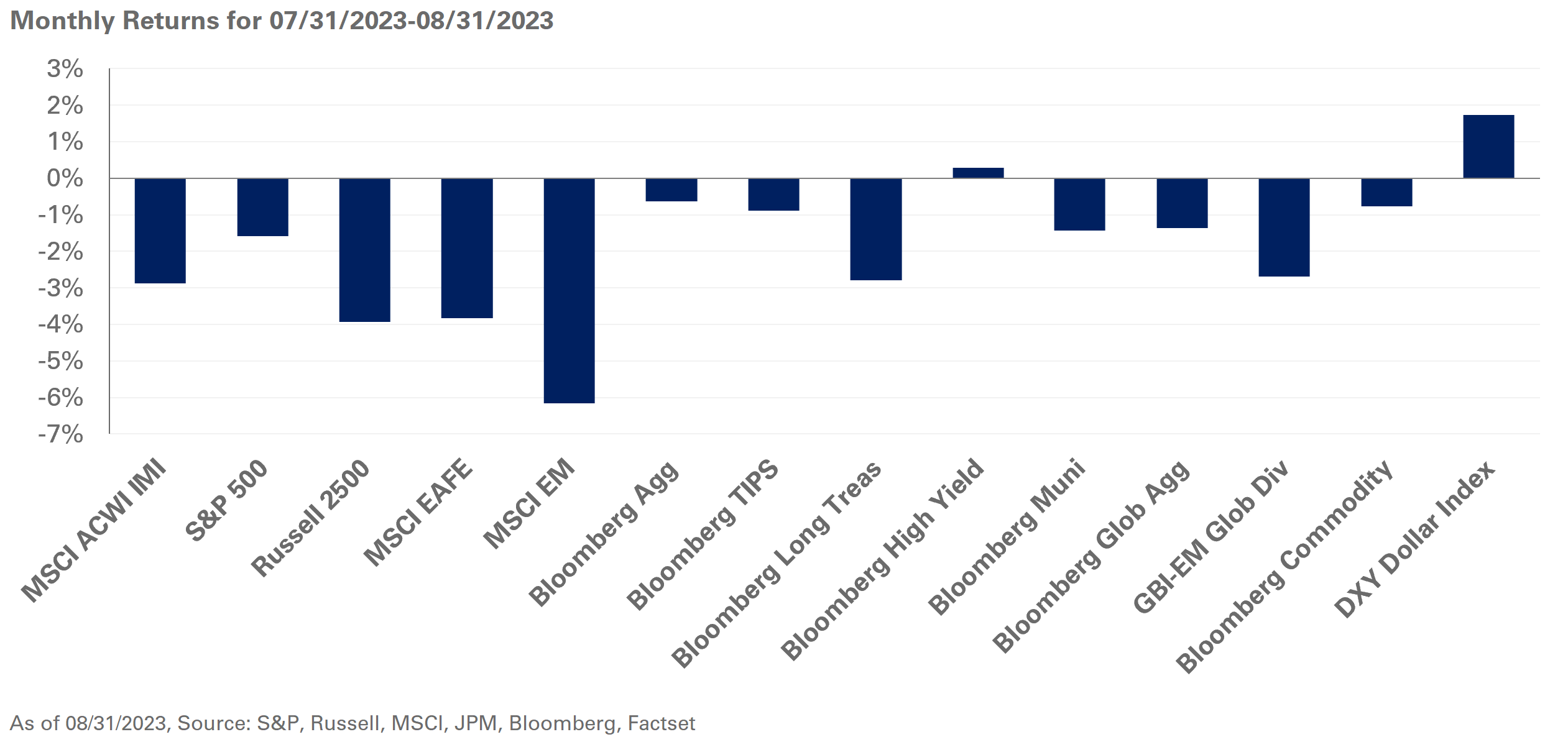

Global equities and bonds ended August in the red as concerns around economic growth in China and upward pressure on interest rates weighed on returns. The month started off on uncertain footing as Fitch Ratings downgraded the sovereign credit rating of the U.S. to AA+ from AAA, and the Bank of Japan unexpectedly adjusted its policy on how it manages the yield curve. Negative investor sentiment from these developments was counterbalanced with better-than-expected data in the U.S., underscoring a still-resilient labor market and moderating inflation pressures.

However, markets were unable to look past a string of weaker-than-anticipated economic data in China, pulling global benchmarks lower for the month. The S&P 500 Index fell 1.6% in August; during the same period, non-U.S. markets were further challenged by a stronger U.S. dollar with the MSCI EAFE Index and MSCI Emerging Markets Index losing 3.8% and 6.2%, respectively.

Higher interest rates also dampened investor sentiment, with U.S. rates trending higher last month: the 10- and 30-year Treasury yields added 14 and 19 basis points, respectively, weighing down longer-duration indexes. These moves came on the back of comments by Federal Reserve Chair Jerome Powell after the Jackson Hole Economic Symposium, in which the central bank said it is prepared to further raise rates if needed and will maintain a restrictive policy stance until it is confident that inflation is moving toward the stated 2% inflation target. Federal Funds Futures continue to reflect one additional rate hike for 2023 and four rate cuts in 2024.

Meanwhile, in real assets, energy markets rallied with spot WTI Crude Oil adding 2.2% as markets weighed OPEC+ production cuts and uncertainty around demand from China.

Despite the recent performance of equities, we continue to suggest investors reduce exposure to the S&P 500, while maintaining U.S. large-cap value positions. We also recommend investors increase exposure to U.S. high-yield bonds and broadly evaluate the risk-return benefit of fixed income. Lastly, we suggest holding higher levels of cash within safe-haven fixed-income exposures and encourage investors to maintain greater levels of portfolio liquidity.