Note: This analysis comes from work NEPC has done over the last six months on investing in a negative-rate environment. This specific topic and the analysis around it got left on the cutting room floor. If you have interest in learning more about our thoughts on negative rates, click here.

Rock-bottom interest rates in the United States, sub-zero rates in parts of Europe and Japan, and the economic havoc wreaked by the coronavirus pandemic are causing some to revisit a longstanding investment tenet: the use of Treasury bonds as an effective diversification tool against equities.

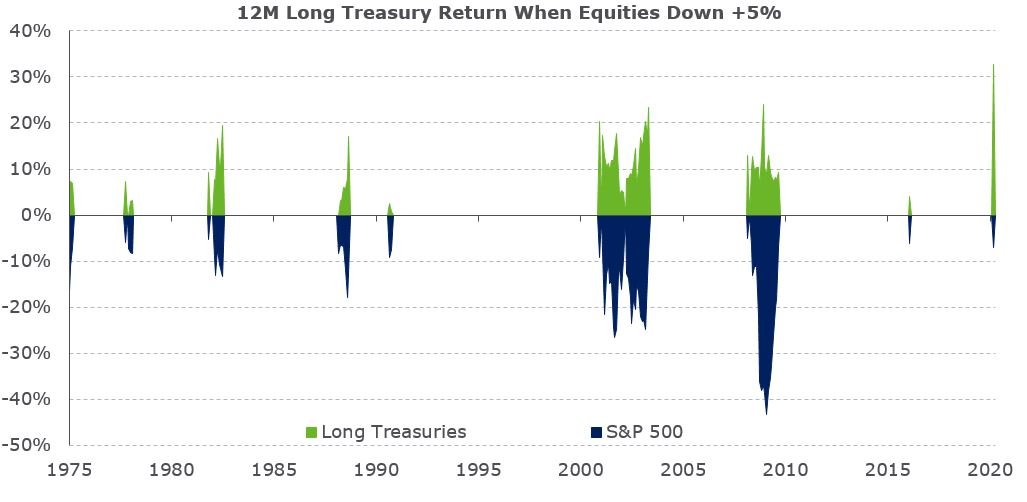

Bonds, particularly safe-haven liquid Treasuries, play a critical role in investment portfolios. They not only provide reliable returns, or yield, over the long term, but also offer negatively-correlated gains when growth-sensitive assets, such as equities, struggle. Historically, when equities have fallen by 5% or more on a rolling one-year basis, Treasuries have almost always offset the losses in some way (Exhibit 1). That said, the 10-year Treasury note is currently offering only 73 basis points of yield, while the 30-year Treasury bond provides a paltry 1.43% annually. These unprecedented lows are compelling investors to question whether falling yields during this period of market turmoil will provide the same cushion they traditionally have and be as effective in balancing equity risk in portfolios.

At NEPC, we believe that while the compensation, that is, the yield for holding these assets has diminished, US bonds—at least for now—still play an important role in portfolio diversification. This may not hold true for when rates fall below zero but, until then, we suggest investors hold onto bonds and reap the benefits of the returns and diversification they offer.

Exhibit 1

Source: FactSet, NEPC

In fact, recent market performance has only reinforced the fact that Treasuries rally when equities sag. Even as equity markets have recovered from March lows, the S&P 500 Index was still down almost 10% for 2020 performance through the end of April. At the same time, long-Treasuries came through for investors willing to hold duration in their portfolio, with year-to-date returns of over 23%.

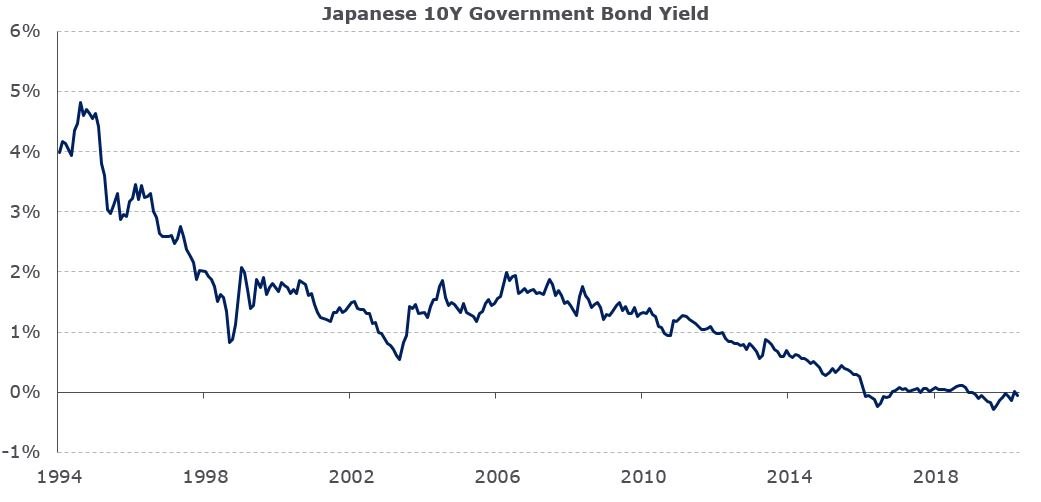

To be sure, Treasury prices are based on their yields, and that robust 23% return is only possible because of the positive duration impact of falling yields. Fortunately for US investors, we have instances of low yields in other countries to provide a potential roadmap of the future. For example, in Japan, yields have stayed low for a very long time: yields on its 10-year sovereign bonds have been below 2% since 1999, lower than 1% since 2012, and at or even below 0% since 2016 (Exhibit 2).

Exhibit 2

Source: FactSet, NEPC

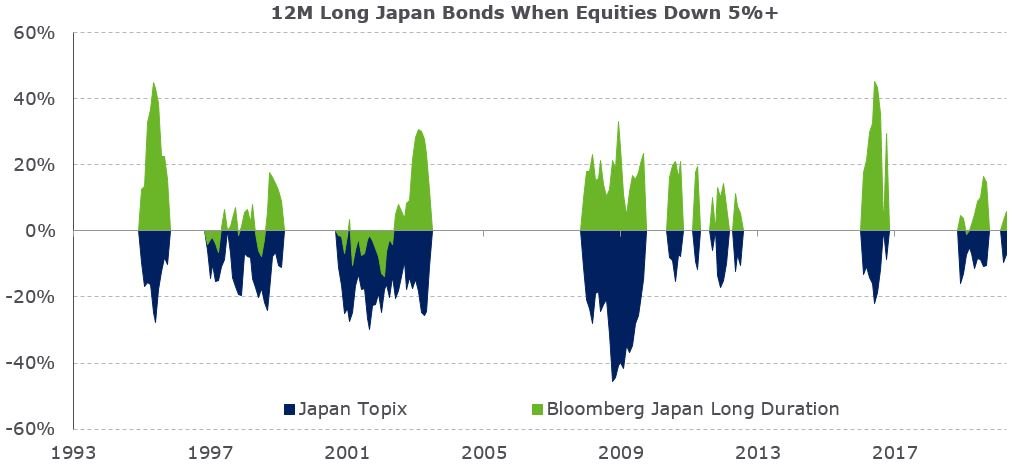

At these low yields, when equities have been negative, Japanese bonds have delivered the type of protection investors have historically enjoyed from Treasuries. That said, low-yielding Japanese bonds have not been as reliable as US long bonds which were in the black around nine out of 10 times that US equities slipped into the red. Still, over 75% of the time, Japanese bonds have delivered positive returns when Japanese equities were negative.

Exhibit 3

Source: FactSet, NEPC

Similarly, when we ran the same exercise for German bunds dating back to 2012—when 10-year Treasury yields were 2% or lower—we find a convincing hit rate of 90%. And if you believe that yields cannot go any lower, imagine investing in 10-year German bunds at the start of 2017, with a mere 0.4% yield: despite the paltry yield, that investment would have delivered a 10% total return at its peak in the fall of 2019 as rates fell over 100 basis points to -0.7% (Exhibit 4).

Exhibit 4

Source: FactSet, NEPC

What should investors expect going forward? Investors should anticipate US Treasuries, even at historically low, but still positive, yields are likely to fall when growth and inflation expectations adjust downward, offering gains to offset likely losses in equities, credit and other growth-sensitive assets across the rest of the portfolio. At least for now, even with very low yields in the US, investors are being paid for taking on the inherent risks in domestic bonds, while also being able to offset risks within their portfolio. There are trade-offs in holding bonds and these should be acknowledged and factored into sizing decisions in an overall diversified allocation:

- Return expectations are historically low with yields starting below 1% implying expected returns below 1%, barring a further fall in rates. Investors must consider the opportunity cost of holding Treasuries, while understanding that it can help to at least hold some.

- While we have witnessed several regions like Japan, and now Europe, experiencing secular low-rate environments, there is no guarantee that rates stay permanently low, providing portfolio protection during the crisis but rising otherwise. With the amount of stimulus now flooding economies across the world, the risk of inflation, deteriorating sovereign credit quality, and/or the dollar giving up its reserve currency status have all increased, weighing on sizing decisions.

Bonds have long played a critical role in diversified investment portfolios. Investment in bonds, particularly safe, liquid Treasuries, has not only offered return compensation through the duration risk premium, but also, just as importantly, provided a helpful negatively-correlated positive return when growth-sensitive assets struggle. While yields have diminished, we remain convinced that at least for now, US bonds still play a crucial role in diversifying portfolios. This may no longer be the case if rates fall below zero, but until then we generally recommend investors hold onto them.