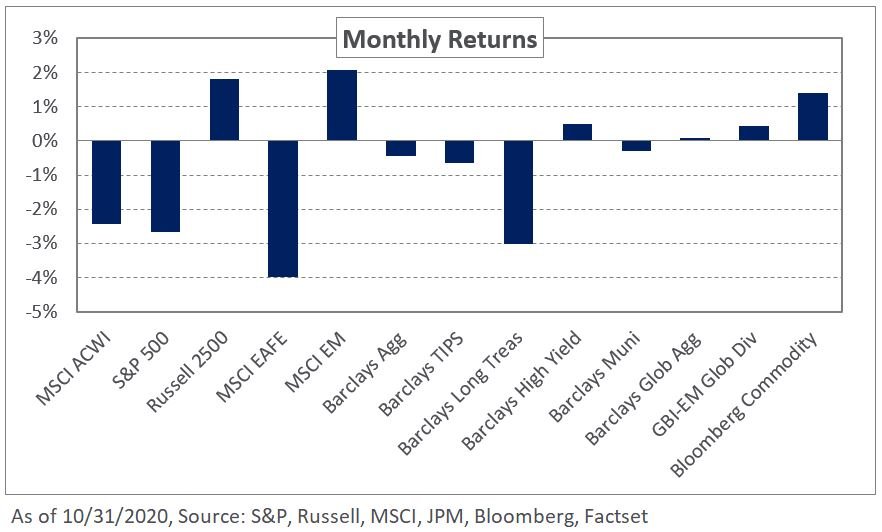

Developed market equities faltered in October amid a wave of risk aversion fueled by an uptick in new cases and hospitalization rates for COVID-19 in the U.S. and Europe. Domestic equities posted their second straight month of declines as volatility in the final trading days of October, incited by diminishing hopes of a pre-election fiscal stimulus package, triggered losses of 2.7% in the S&P 500 Index. In contrast, emerging market equities gained 2.1% last month, according to the MSCI Emerging Markets Index, amid improving economic data, particularly in emerging Asia, and weakness in the U.S. dollar.

In fixed income, U.S. rates rose with the 10- and 30-year Treasury yields increasing 17 and 19 basis points, respectively. The movement in the long-end of the yield curve and relative steepening detracted from long duration. The Barclays Long Treasury Index lost 3% in October. In Europe, yields broadly declined, reflecting renewed concerns around the coronavirus. As a result, the 10-year German Bund yield fell nine basis points to -0.62%.

Within real assets, spot WTI crude oil declined 10.9% last month, bringing year-to-date losses to 41.6%; the drop reflects ongoing concerns around lower demand because of the pandemic and also increasing supply from Libya.

The recent weakness in equities and associated volatility serve as a reminder of the fragility of the broader market rally. Despite the impressive performance of risk assets over the past few months, significant economic uncertainty remains with the weak macroeconomic backdrop. In addition, with the outcome of the U.S. presidential election likely to be finalized soon, the trajectory of COVID-19 and monetary and fiscal stimulus are of greater importance for financial markets. In the face of such uncertainty, we expect heightened volatility and encourage investors to be disciplined and mindful of market liquidity. To this end, we recommend investors maintain a dedicated allocation to Treasuries to support liquidity levels and cash-flow needs as potential market dislocations can introduce bouts of illiquidity across publicly-traded markets.