Volatility roiled markets in the first quarter as investors grappled with the potential economic fallout of the COVID-19 pandemic. Economies across the world screeched to an abrupt halt in the face of travel restrictions and containment efforts, sending the CBOE Volatility Index, a barometer of market sentiment, to over 80 during the quarter before settling at 53.5 on March 31.

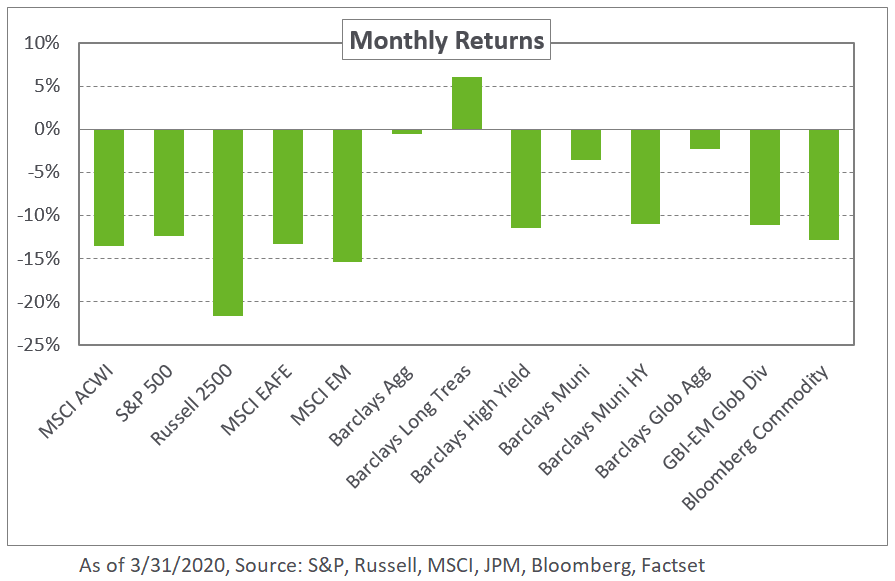

Most major equity indexes entered into bear territory in March, falling as much as 20% from recent highs. While the subsequent announcements of significant fiscal and monetary responses across the world spurred a rally in stocks, most benchmarks remained in the red. The S&P 500 Index ended the month down 12.4%, and posted its worst quarterly performance since 2008 with a decline of 19.6%. Outside the US, a strengthening dollar added to the trials and tribulations of the MSCI EAFE and MSCI Emerging Markets indexes, which fell 13.3% and 15.4%, respectively, in March.

Within fixed income, US rates moved materially lower after the Federal Reserve cut rates in two emergency sessions by 150 basis points to a range of 0.00%-0.25%. The 10- and 30-year Treasury yields fell 46 and 35 basis points, respectively. In addition, the Fed announced an unlimited expansion of its balance sheet and credit support in efforts to bolster the US economy and provide market liquidity. In credit, spreads widened during the month, reflecting risk-off sentiment and the heightened probability of defaults during times of economic stress. The most significant spread widening occurred in lower-quality issues, causing the Barclays US Corporate High Yield option-adjusted spread to increase 380 basis points to 8.8% with a corresponding decline of 11.5% for the month.

In real assets, commodities fell further into the red amid abundant supply, triggered by a price war between Russia and Saudi Arabia, and a steep drop in demand as measures to contain the pandemic include stringent restrictions on travel and movement. As a result, energy sold off with spot WTI crude oil plummeting 55.2% for the month – pushing year-to-date losses to 67.1%.

As we start the second quarter, we expect market volatility to remain heightened as COVID-19 continues to wreak havoc on the global economy. As always, we advocate a disciplined investment process and rebalancing towards targets to maintain a diversified strategic asset allocation. In addition, we recommend investors be mindful of market liquidity and look to build cash to cover one quarter of spending needs.