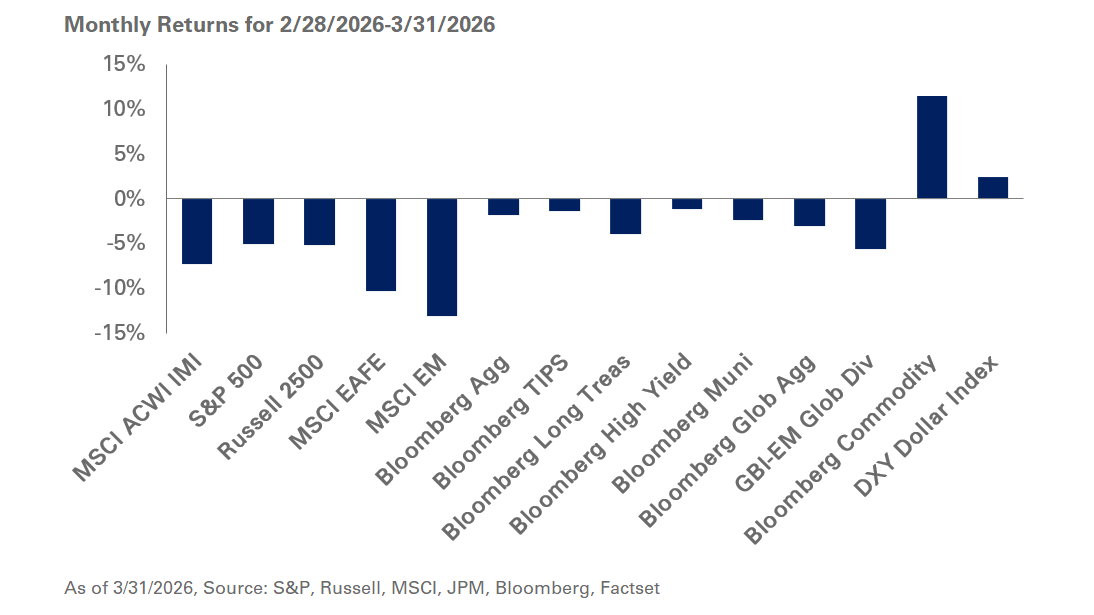

Global equities snapped their winning streak amid a spike in volatility, resulting in a moderate correction early February. Investors’ concerns around rising wage inflation potentially leading to more aggressive rate hikes by the Fed and a larger projected government deficit interrupted the S&P 500’s golden run of 15 straight months of gains as the index tumbled 3.7%. International equities were in the red as well with the MSCI EAFE and MSCI EM indexes declining 4.5% and 4.6%, respectively.

The specter of higher inflation also weakened government bond prices with the 10-year Treasury up 16 basis points at 2.86% and the 30-year Treasury increasing 19 basis points to 3.12%. Liquid real assets declined sharply with the Alerian MLP Index falling 9.7% last month, as higher Treasury yields took some of the shine off risky investments. Treasury-based indexes continued their decline with the Barclays Long Treasury Index down 3%. Despite beliefs that recent elections in Italy and political wrangling in Germany would weigh on international yields, 10-year German and Japanese sovereign bonds ended the month little changed.

At NEPC, our views remain broadly unchanged despite volatility rearing its head. We still prefer international and emerging markets equities relative to domestic stocks. At the same time, we acknowledge the likelihood of additional uncertainty given potential trade disruptions and recent electoral developments in Europe. For fixed income, we maintain our recommendation for investors to reduce credit exposure with spread compression, and favor the addition of TIPS given the potential for higher inflation. Finally, we remind investors to be vigilant in the face of elevated volatility and to adhere to disciplined rebalancing if and when deeper selloffs occur.