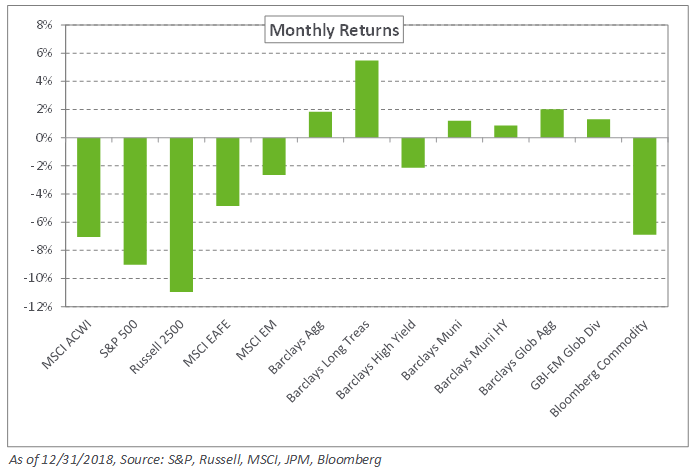

Global equities went out with a whimper in a year marked by volatility as ongoing trade tensions, a rising rate environment, and weaker economic data weighed on all major global equity indices. The S&P 500 Index fell 9.0% in December – logging its heftiest monthly decline since February 2001. While international and emerging markets were in the red as well, they were more insulated from the broad sell-off, with the MSCI EAFE and MSCI Emerging Markets indices down 4.9% and 2.7%, respectively.

In a widely anticipated move, the Federal Reserve raised rates last month for the fourth time in 2018. As a result, short-term rates moved modestly higher, while intermediate- and long-term rates declined, underscoring a wave of risk aversion. International yields also declined with 10-year German and 10-year Japanese bond yields falling to 0.24% and 0.00%, respectively. Within credit, spreads continued to widen, weighing on total returns. The Barclays US High Yield Index declined 2.1% as spreads increased 108 basis points to 526 basis points in December.

In real assets, spot WTI crude oil lost 10.8%, ending the month at $45.41 per barrel, amid concerns around oversupply and potentially weakening demand fueled by a less favorable global economic outlook. Additionally, the midstream energy space continued to decline as rising rates and distribution cuts weighed on sentiment. In response, the Alerian MLP Index fell 9.4% in December.

With markets whipsawing as we enter 2019, we anticipate the drivers of recent volatility to continue in the near term. To this end, we remind investors to remain vigilant and to maintain a diversified, risk-balanced portfolio to weather potential market sell-offs. While we still advocate adding safe-haven fixed-income assets, we believe the magnitude of the recent sell-off offers an opportunity to rebalance equity exposure back to targets.