In this second installment of a three-part series on VEBAs, we review key factors plan sponsors ought to consider when evaluating investment options.

A Voluntary Employees’ Beneficiary Association (VEBA) comes with a wide variety of options. As a result, there’s no singular framework that can be applied when developing an investment strategy for the assets. At NEPC, we believe it is critical to understand how each of the unique factors should be incorporated when considering an appropriate investment solution.

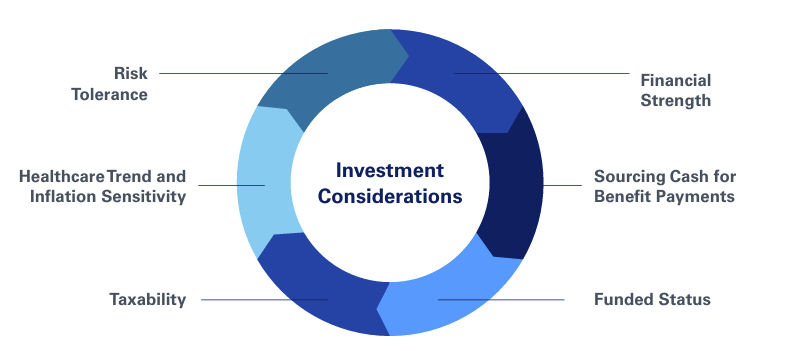

INVESTMENT CONSIDERATIONS

I. RISK TOLERANCE

The plan sponsor’s risk appetite can be used to guide the asset allocation framework. Usually, VEBAs pursue a total-return approach, i.e., a strategy focused on an allocation framework intended to maximize risk-adjusted returns; the risk posture with this approach can vary, running the gamut from conservative, to moderate and aggressive. The conservative total-return approach typically emphasizes public fixed-income exposure in the allocation, whereas a heavy public equity allocation usually indicates an aggressive posture based on our experience. Input from the plan sponsor sets the foundation for the

appropriate risk/return profile.

II. PLAN SPONSOR’S FINANCIAL STRENGTH

Since there are generally no mandatory minimum required contributions associated with VEBAs, plan sponsors may have considerable discretion regarding the timing of contributions and how benefits are paid (i.e., using trust assets or passing cash through the trust from external operating accounts). Given this flexibility in contribution and benefit payment policies, the plan sponsor may incorporate the organization’s financial strength and the tax status when deciding the timing of contributions and whether to redeem assets to fund benefit payments or use a pay-as-you-go approach, barring any collective bargaining agreements.

Based on our experience, discretionary contributions usually exceed required benefit payments during economic environments in which the plan sponsor’s industry is generally performing well. All else being equal, this results in the subsequent need to reinvest the proceeds and an overall increase in the plan’s funded status. On the other hand, discretionary contributions may be suspended when the industry is contracting, and the plan sponsor is facing business challenges. Trust assets may be utilized to satisfy required benefit payments, emphasizing a heightened need for liquidity when developing the plan’s investment strategy.

A change in management and organizational priorities may result in adjustments to both contribution and benefit payment policies. As such, in our opinion, the investment strategy should be nimble enough to accommodate the broad flexibility inherent in how VEBAs are managed.

III. HEALTHCARE BENEFITS AND SENSITIVITY TO INFLATION

Healthcare benefits funded through VEBAs typically include a component in the actuarial valuation of benefits that reflects medical inflation to keep pace with rising healthcare costs (though many plans do cap this assumption in the valuation), according to the plans we have analyzed.

While not all provisions apply to all plans, the actuarial liabilities for plans funded through VEBAs may include an expense load that is tied to inflation, such as CPI or medical inflation. All else being equal, the inflation expense load may increase asset return requirements and suggests exposure to inflation-sensitive assets, such as Treasury Inflation-Protected Securities (TIPS), to mitigate this expense load, based on our asset allocation approach.

We recommend that plan sponsors understand the impact of inflation on liabilities and determine if exposure to inflation-sensitive assets is required in the investment portfolio. There are limited, if any, investment options available that can precisely offset the inflation associated with most plans funded through VEBAs.

IV. FUNDED STATUS

We believe it is crucial to have visibility into the plan’s funded status, as this could be a factor when determining investment strategy. Considering the absence of mandatory minimum contributions, the ability to maintain funds outside the trust, the potential for benefits to be forfeited, and the flexibility in benefit distribution policies, VEBAs can be persistently underfunded or have a material surplus.

Significantly underfunded plans may pursue an investment strategy focused on long-term asset growth, while the overfunded plans may look to preserve funded status. In some cases, plan sponsors may maintain more than one VEBA, each with different funded status, contribution schedules, and benefit payment practices.

For overfunded plans, the excess asset accumulations may trigger unrelated business taxable income (UBTI), under Section 419A of the Internal Revenue Code. As a result, materially growing the plan’s funded status may have limited benefits unless there is a desire to explore the transfer of some assets to another VEBA, which can be a complex process.

In addition, transferring plans funded through VEBAs to an insurance company—either through a group annuity buy-out or buy-in contract—is less common from our perspective; therefore, VEBAs typically do not have an endgame like pension risk transfers. We believe it is feasible for plan sponsors to incorporate a glide path as the cornerstone of an investment strategy when managing VEBAs under certain scenarios.

V. SOURCING CASH FOR BENEFIT PAYMENTS

As discussed in the first part of this blog series, there is no mandatory requirement to fund VEBAs; as such, funds earmarked for benefit payments can be held outside of the trust or held as part of the trust’s investment portfolio.

If the funds are held as investments in the trust, the plan sponsor can redeem these investments to raise the cash required to meet the benefit obligation. On the other hand, if the funds are held outside the trust, the plan sponsor can contribute and pass through enough cash to the trust to match the outgoing benefit payments. This pay-as-you-go approach means the plan sponsor covers benefit payments as they come due, rather than investing funds in advance and redeeming them later.

Raising cash for benefits directly from the trust’s investments imposes a requirement for greater liquidity. Therefore, we suggest being mindful of exposures to illiquid assets. We encourage plan sponsors to have a disciplined strategy to raise cash, so they are not caught off guard in periods of extreme market volatility.

In other common scenarios, where the trust can be persistently underfunded and cash is passed through to meet benefit payments, there may be flexibility in incorporating modest exposure to private markets, particularly strategies such as private credit with a short fund life. The limited allocation to private markets may help to maximize the trust’s expectations for investment returns. The plan sponsor can also adjust how benefits are paid, so it is essential to consider this when developing an appropriate investment strategy.

VI. TAXABILITY

It is important to understand the tax implications of the trust, as some trusts may have a tax-exempt structure if they meet the requirements under the Internal Revenue Code and ERISA. If the trust is set up to be tax-exempt, VEBAs are often similar to traditional defined benefit plans that tend to be tax-agnostic when making investment decisions based on our view.

Other VEBAs may be subject to taxes as a whole or in some parts, and a closer understanding of each trust’s nuances may reveal significant variability in the tax implications. For example, understanding the impact of capital gains (short term versus long term), investment income (ordinary income versus qualified dividend income), unrelated business income, deductible versus non-deductible contributions, and the trust type, i.e., welfare versus healthcare benefit funds, must be factored in when considering an investment strategy.

Plan sponsors for taxable VEBAs should evaluate their investment strategy through a tax-sensitive lens, as this will help assess the impact on asset allocation, trading and selection of an investment vehicle, among other factors, which can erode after-tax investment returns.

At NEPC, we do not provide tax advice and encourage plan sponsors to consult with their tax advisors and attorneys. We provide high-level insight into implementable techniques that can increase tax sensitivity throughout the investment portfolio, and recommend clients engage with their tax advisors for a more comprehensive tax strategy.

CONCLUSION

We believe the above factors are essential to understand while determining an investment strategy for VEBAs. Each factor is important to consider independently, as it may influence two seemingly identical trusts differently and result in differentiated investment solutions between the trusts.

Plan sponsors may need to incorporate a dynamic strategy that evolves as their circumstances change without sacrificing the fiduciary responsibilities associated with the governance of institutional portfolios earmarked to fulfill benefit obligations to participants and their beneficiaries.

Stay tuned for the third and final installment of this series, where we explore a liability-driven investing approach as a tool for efficient governance and management of VEBAs. Meanwhile, if your company is evaluating a VEBA or if you want to better understand its potential impact on your firm, we are available to discuss the process and implications.