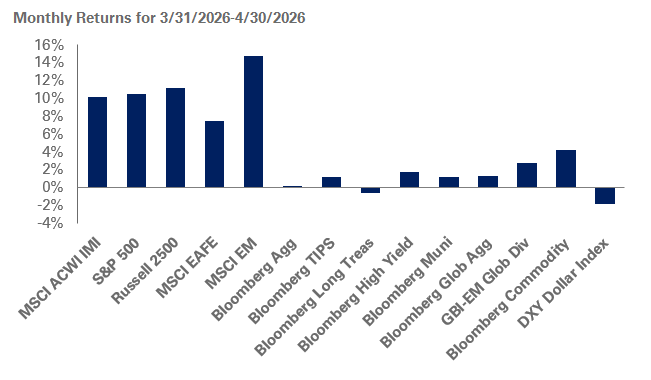

Stocks rallied in April following a sharp sell-off in March. Hopes for a conclusion to the Iran war and the re-opening of the Strait of Hormuz buoyed investor sentiment, propelling the S&P 500 to its best month since November 2020. U.S. small-cap equities led performance with the Russell 2000 Index posting returns of 12.2% last month. Outside the U.S., emerging market stocks gained 14.7%, bolstered by artificial intelligence-related names in South Korea and Taiwan. The MSCI EAFE Index trailed in April, delivering returns of 7.5%, as concerns of potentially tighter monetary policy and disruptions in energy supplies from Iran remain headwinds for the market.

In other news, macroeconomic data released in April reinforced the resilience of the U.S. economy despite rising energy costs. The U.S. economy grew at an annualized rate of 2% in the first quarter, helped by robust consumer spending and private investment. The job market also appears to be on solid footing with weekly unemployment claims coming in at a 50-year low in April. However, inflation and price pressures remain an ongoing concern. The release of March U.S. CPI showed inflation increasing 0.9% last month due to higher energy prices, even as core prices (excluding energy and food) rose a modest 0.2%. central banks were in the spotlight in April, with Japan and Europe signaling potential tighter monetary policies. The Federal Open Market Committee (FOMC) also met and held its policy rate steady at a range of 3.5%–3.75% for the third straight meeting. This meeting was likely the last for Jerome Powell as FOMC Chair with Kevin Warsh expected to take over following his Senate confirmation. However, Powell indicated he will remain in his role as a member of the Board of Governors of the Federal Reserve System, with his term expiring in January 2028.

Meanwhile, fixed-income markets were subdued relative to equities with 10- and 30-year Treasury yields rising modestly in April. During this period, the Bloomberg Aggregate Bond Index rose 0.1%, while long-term Treasury indexes were in the red due to higher yields. Credit markets did respond to the improved sentiment with spreads tightening on investment grade and non-investment grade corporate debt, fueling gains for high-yield credit and bank loans.

Within real assets, volatility was exceptionally high as the price of oil gyrated throughout the month, but WTI ended April modestly higher, settling at $105 a barrel. Broad commodity markets, as represented by the Bloomberg Commodity Index, posted a 4.2% return in April, up nearly 30% for the year. During this period, REITs were also in the black, rallying 9%; gold lagged, down 0.8% in April. While the geopolitical backdrop remains a source of volatility for markets, robust corporate earnings and resilient economic data continue to point toward a supportive environment for growth. We encourage investors to look past day-to-day headlines and suggest fully utilizing the portfolio risk budget, while staying close to strategic target levels.

Within equities, we encourage investors to be mindful of portfolio underweights and outsized tracking error levels relative to the top names in the MSCI ACWI IMI and the S&P 500 indexes. We still recommend investors hold high-quality, liquid assets and suggest holding safe-haven fixed-income securities at strategic target levels to support portfolio liquidity. We also advise shying away from liquid segments of lower-quality credit given tight spread levels and market sentiment.

As of 4/30/2026, Source: S&P, Russell, MSCI, JPM, Bloomberg, FactSet