In this blog, the final installment in a series of three, we discuss a client’s use of a custom liability driven investment (LDI) strategy to manage plan assets until plan termination. In the first part we highlighted the importance of monitoring the funded status of a defined benefit plan; in the second, we examined the benefits of using a specialist to achieve the desired outcome in a pension risk transfer, and the advantage of having an investment consultant to help with the process.

A corporate employer on the path to terminating its defined benefit plan faces numerous complexities.

This journey can bring to the forefront key issues such as asset allocation, liquidity, funded status, and hedging requirements. Risks for corporate pension plans can change suddenly and quickly, taking employers by surprise. As a result, we maintain it is important to partner with specialists whose experience lies in executing retiree annuity buyouts. Enter: NEPC’s deep knowledge on pension risk transfers and its network of relationships with professionals that can help our clients achieve their goals. We can play a decisive role in helping a client de-risk the defined benefit plan’s portfolio to lock in its fully funded position and prepare for a retiree annuity buyout transaction.

The Challenge

A NEPC client wanted to minimize funded status risk prior to plan termination. The client’s goal was to reduce funded status volatility by maintaining a 100% interest rate hedge while addressing credit and yield curve risk.

Recognizing the termination process would involve lump sum distributions and annuity purchases, the client sought a strategy that would allow for dynamic adjustments to minimize risk throughout the process.

ILLUSTRATIVE CLIENT PROFILE – UPDATED

| Plan assets | $158 million |

| Plan type and status | Two traditional, frozen plans |

| Asset allocation | 100% liability hedging |

| Current funded status | 112% |

| Liability duration | Seven years |

| Participant population | 56% retirees, 32% term-vested, 12% active |

| Expected date of plan termination | Second quarter 2026 |

Source: NEPC. The above is an illustrative example of a client’s experience with NEPC. Past performance is not indicative of future results. The above example is intended for discussion purposes. Please see additional disclosures throughout these materials.

Enter NEPC1

NEPC canvased our broader focused placement list (FPL) of LDI managers across the intermediate-, long-, and extended-duration spectrum. We developed criteria to narrow the field to the appropriate candidates for a custom LDI strategy based on the client’s goals and preferences. This included the availability of pooled fund vehicles, a dedicated LDI solutions team, experience with risk transfers, and current or former manager relationships.

To identify the manager, NEPC coordinated a rigorous search and requested that the managers provide a customized proposal, in a case study format, for how they would implement their portfolio to achieve the client’s goals. The selected firm would initially manage two portfolios for each of the client’s two plans and then create a single custom portfolio once the plans were merged.

A key consideration for this client’s search included the manager’s ability to use pooled fund vehicles for efficient implementation. Given the asset size, it was determined that pooled funds would be more efficient and cost-effective than a separate account; a separate account may be more appropriate for larger account balances, with the ability to consider transferring assets in-kind as part of the termination process.

The client also considered the manager’s dedicated LDI solutions team, LDI thought leadership, and experience managing portfolios for risk transfers with a focus on credit research capabilities to mitigate downgrade and default risks, since that adversely impacts asset values. Our review also considered typical criteria such as historical composite performance results, experience, stability of the investment team, the potential for repeatable alpha generation, and research capabilities.

A major challenge in evaluating custom proposals from LDI managers is that they are not directly comparable to benchmark-managed strategies. In this case, the manager who was hired not only demonstrated strong experience in fixed income, but also a thorough understanding of the pension de-risking process.

The ongoing management of the custom LDI relationship prior to plan termination requires close coordination with all parties, including the client, manager, consultant and actuary. On an ongoing basis, the actuary should provide updated information on cash flows to the manager so they can determine the optimal allocation that reduces risk for the client. The manager will need to know the timing of the lump sum offering, estimated take-up rates, and projected amounts to ensure available liquidity and determine when to unwind the lump sum liability hedge. They will also need to review the updated cash flows post lump sums and adjust their hedge for the annuity to minimize funded status volatility.

We believe a custom LDI strategy should be evaluated based on its ability to minimize funded status volatility and how its performance compares to a custom market benchmark.

ILLUSTRATIVE OUTCOME

| Before | After | |

| Hedge Ratio | ~90% | 100% |

| Yield Curve Match | Overweight long-end, underweight short | Duration matched across key rates |

| Funded Status Volatility | 3.6% | <2% |

| Number of managers | 3 | 1 |

| Fees | $513,000 | $289,000 |

Source: NEPC. The above is intended for educational purposes only and has been provided as a sample to illustrate a point. Past performance is not indicative of future results. Please see additional disclosures at the end of these materials.

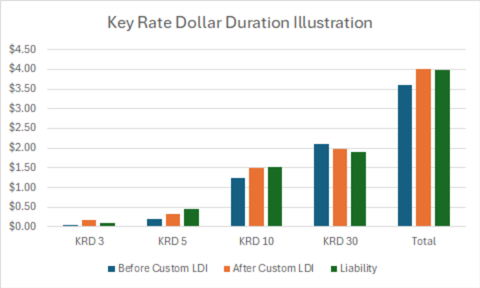

The chart below is an illustration of key rate duration (KRD) matching. Improving the matching across key rates helps reduce funded status volatility by minimizing risks due to changes in the shape of the curve.

Source: NEPC. The above is intended for educational purposes only and has been provided as a sample to illustrate a point. Past performance is not indicative of future results. Please see additional disclosures at the end of these materials.

NEPC believes custom LDI strategies can play a key role in helping clients prepare portfolios for de-risking and plan termination. Implementation of a custom LDI strategy may depend on many factors, including the size and complexity of the portfolio and de-risking activity under consideration.

Through a carefully planned and customized process, we helped our client select a manager aligned with their criteria. The manager brought to the table dedicated experience in LDI solutions, pooled fund vehicles, and a strong understanding of the de-risking process. Implementation of the custom LDI strategy reduced the number of managers and fees. The manager also helped achieve the 100% hedge ratio target and reduce yield curve risk and overall funded status volatility.

1The above is an illustrative example of a client’s experience with NEPC. Past performance is not indicative of future results. The above example is intended for discussion purposes. Please see additional disclosures throughout these materials.

Please contact your NEPC consultant if you have any questions or would like to discuss your individual plan.