In this blog, the second in a series of three, we highlight the importance of using a specialist to achieve the desired outcome in a pension risk transfer, and the advantage of having an investment consultant to help with the process. In the first installment of the series we highlighted the importance of monitoring the funded status of a defined benefit plan.

A corporate employer on the path to terminating its defined benefit plan faces numerous complexities.

This journey can bring to the forefront key issues such as asset allocation, liquidity, funded status, and hedging requirements. Risks for corporate pension plans can change suddenly and quickly, taking employers by surprise. As a result, it is important to partner with specialists whose focus lies in executing retiree annuity buyouts. Enter: NEPC’s deep knowledge on pension risk transfers and its network of relationships with experts that can help our clients achieve their goals. We can play a decisive role in helping a client de-risk the defined benefit plan’s portfolio to lock in its fully funded position and prepare for a retiree annuity buyout transaction.

The Challenge

An NEPC client considered alternatives to its actuary for risk transfer. The client’s goal: engage with a firm with a proven record of successful risk transfer transactions that could provide stellar service at a competitive price.

A specialist, hired as either an independent expert or independent fiduciary, can provide these services at an attractive cost for a similar or better outcome through potentially competitive bids from insurers. However, using a specialist firm may also entail greater administrative effort relative to utilizing the incumbent actuarial firm.

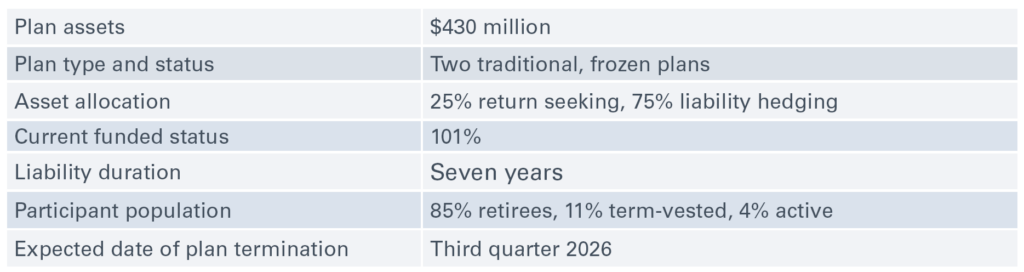

Sample Client Profile

Enter: NEPC

NEPC maintains professional relationships with firms specializing in managing defined benefit plans, including actuarial, administrative, and pension risk management strategies. We introduced our client to three annuity placement firms to evaluate alongside their incumbent actuary.

We provided each finalist with background information on the client and participated in the client’s discussions with each firm. The client chose to engage one of the three annuity placement firms as a pension risk transfer specialist to facilitate the annuity buy-out in place of the incumbent actuary due to its track record of lower costs and success in executing risk transfers over the last several years.

An independent specialist and independent fiduciary assist plan sponsors in fulfilling the Department of Labor’s 95-1 requirements when purchasing annuities for a pension plan. However, under an independent specialist mandate, the decision to select the insurer remains with the plan sponsor, while in the case of engaging an independent fiduciary, 3.38, the specialist firm has the discretion to select the insurer on behalf of the plan sponsor.

NEPC facilitated discussions between the client and the annuity placement firm, which resulted in a pension risk transfer feasibility study. The feasibility study evaluated several annuity buyout scenarios with different populations and monthly benefit thresholds. In addition, the study also assessed potential implications, such as settlement accounting of the scenarios under consideration.

The Outcome

The plan released $263 million in assets to settle $283 million in liabilities, or roughly 93% of projected benefit obligation (PBO). This was a compelling result as the liabilities were settled at a discount relative to the PBO, which led to a net benefit in funded status of the residual plan of $17 million.

On the completion of a successful risk transfer, the focus shifted to minimizing volatility around asset allocation and maintaining the funded surplus until plan termination. The client considered the pension risk transfer specialist (“PRT”) for the plan termination project, which included a lump sum offering and annuitization.

While this was a favorable outcome for this client, it is important to note that each pension risk transfer is unique, and pricing varies based on factors such as interest rates, the participant population being annuitized, the type of liability structure, and market dynamics.

By working with a PRT specialist, our client strengthened their funded position and gained additional options to explore how to use the surplus after the termination process. This example underscores NEPC’s knowledge of the de risking and termination processes, and our network of specialists that can add value for our clients.

Next Up

Stay tuned for the third and final installment of this series, where we help our client implement a tailored liability-driven investing strategy to improve efficiencies, reduce risk and save on fees. Please contact your NEPC consultant if you have any questions or would like to discuss your individual plan.