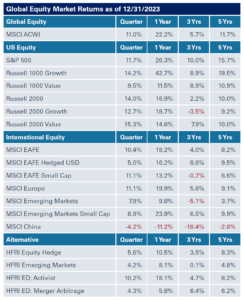

Global Equities

Equities posted impressive gains in the fourth quarter, ending a strong year on a high note. For the three months ended December 31, U.S. stocks got a shot in the arm from a lower inflation print and robust economic data; during this period, the S&P 500 returned nearly 12%, finishing 2023 up over 26%.

Equities posted impressive gains in the fourth quarter, ending a strong year on a high note. For the three months ended December 31, U.S. stocks got a shot in the arm from a lower inflation print and robust economic data; during this period, the S&P 500 returned nearly 12%, finishing 2023 up over 26%.

Mega-cap growth stocks continued to lead the charge with the Nasdaq Composite up around 14% for the quarter and over 44% for the year. After lagging the first nine months of the year, small-cap equities outpaced large-cap stocks in the fourth quarter with gains of 14%, ending the year up around 17%.

International developed and emerging market equities were also in the black with the MSCI EAFE Index returning 10% in the fourth quarter and 18% for the year, while the MSCI EM Index gained around 8% for the three months ended December 31 and 10% for 2023.

Meanwhile, fundraising activity in U.S. private equity totaled $375 billion last year, modestly down from $379 billion in 2022, according to data from Preqin. The total number of funds raised dropped by around 51%, underscoring a flight to larger and more established funds; the drop was particularly pronounced in emerging and first-time funds. Fundraising in the U.S. venture market plummeted in 2023 to $66.9 billion—a record low since 2017—from a high of $173 billion a year earlier.

New deal activity in U.S. private equity declined to $645 billion last year compared to $915 billion in 2022, according to data from PitchBook. Exit activity also fell, totaling $234 billion in 2023 – a new low since 2011. Venture deal activity stood at $171 billion in 2023, its lowest level since 2019, as venture capitalists slowed their pace of deployment and portfolio companies streamlined their organizations to increase cash runway.

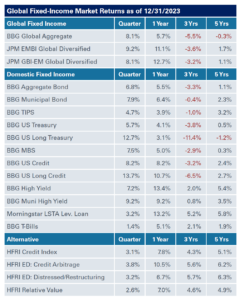

Global Fixed Income

Treasuries reversed course in the fourth quarter as the Federal Reserve assumed a more dovish stance after reinforcing the message of higher-for-longer rates in the prior quarter. Treasuries rallied with the two- and three-year maturities experiencing the greatest moves during the quarter. Credit spreads tightened across fixed-income markets and ended the year below long-term median levels, resulting in substantially positive returns in the fourth quarter with longer maturities and lower-quality debt led the way.

Treasuries reversed course in the fourth quarter as the Federal Reserve assumed a more dovish stance after reinforcing the message of higher-for-longer rates in the prior quarter. Treasuries rallied with the two- and three-year maturities experiencing the greatest moves during the quarter. Credit spreads tightened across fixed-income markets and ended the year below long-term median levels, resulting in substantially positive returns in the fourth quarter with longer maturities and lower-quality debt led the way.

For the three months ended December 31, the spread on investment-grade corporate bonds tightened 22 basis points, while high-yield corporate bonds were tighter by 71 basis points. The yield on the 30-year Treasury fell 67 basis points to end the quarter at 4.03%, while the two-year Treasury note yield fell 80 basis points to end the quarter at 4.23%. The Bloomberg U.S. Aggregate Index returned 5.5% in 2023, while the Bloomberg U.S. High Yield Corporate Index was up 13.4% during the same period.

Real Assets

The fourth quarter was a mixed bag of returns for real assets, in line with the rest of 2023. The Bloomberg Commodity Index was down 4.6%, closing out the year with losses of 7.9%. Crude oil gave back most of its third-quarter gains, down 21.1%, bringing the losses for 2023 to 10.6%. The midstream market avoided a similar fate, posting a gain of 6.4% for the three months ended December 31; gold was even stronger during this period, returning 11.5%.

Meanwhile, global natural resources gained 3.6% in the fourth quarter, ending the year in the black at 4.1%. The S&P Global Infrastructure Index recovered in the fourth quarter and was up 10.9%. NEPC is constructive on infrastructure, and we continue to favor private markets as a means to implement infrastructure in a portfolio.

Elsewhere, in public real estate, the NAREIT Global REIT Composite Index rebounded from a rocky year with gains of 15.6% in the fourth quarter to end 2023 in the black. Meanwhile, private real estate returns did not emerge unscathed, posting their fifth straight negative quarter, with the NCREIF ODCE posting a 4.83% preliminary gross loss for the three months ended December 31. The negative total return is inclusive of asset depreciation of 5.77%, as the effects of rising interest rates continue to pressure valuations following historically high returns prior to 2022.