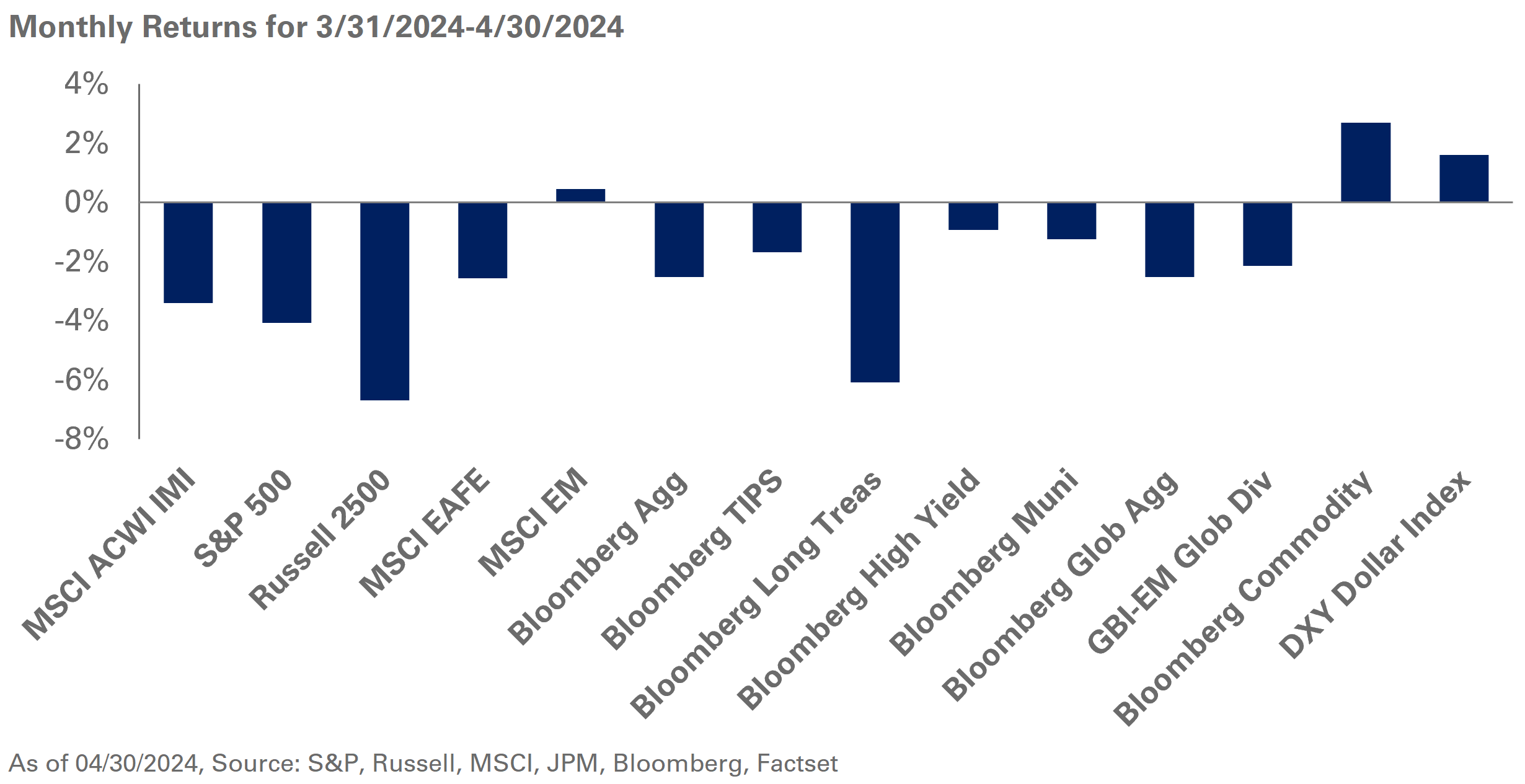

The S&P sold off 4.1% in April with equity markets reacting to rising interest rates and elevated inflation prints. Large-cap stocks outperformed, while small-cap stocks continue to be sensitive to long-term interest rates with the Russell 2000 selling off 7% for the month.

Outside the U.S., the MSCI Emerging Markets Index added 0.4% in April. Led by strong results in China, the MSCI China Index returned 6.6% last month, buoyed by supportive industrial economic data and corporate earnings growth. Meanwhile, the MSCI EAFE Index lagged, dropping 2.6% as a strong dollar was a headwind for markets. Currency weakness was most notable in Japan with the yen weakening 10% in April.

Economic strength and a steady stream of sticky inflation reports shifted expectations of interest rate cuts from the Federal Reserve. The market began the year expecting nearly six cuts in 2024; now, expectations have pushed potential Fed action to later this year with less than two cuts priced in by the market. As a result, 10- and 30-year Treasury yields increased 48 and 44 basis points, respectively, last month. Broad based fixed-income indexes turned negative in April, with the Bloomberg U.S. Treasury Index down 2.3% and the Bloomberg Aggregate off 2.5%. Within credit markets, spreads were largely unchanged for the month with levered loans the only positive outlier.

Meanwhile, in real assets, the Bloomberg Commodity Index gained 2.7%, despite spot WTI crude oil falling 2.5% in April. During this period, gold prices gained 2.4%, while REITs fell 6.3% due to pressure from rising interest rates in the U.S.

We continue to recommend investors hold a blend of S&P 500 and value exposure within U.S. large-cap stocks. Additionally, while markets have undergone a hawkish repricing of interest rate expectations, we still believe investors remain overly biased to falling interest rates. We suggest investors broadly evaluate the risk-return benefit of fixed income and look to add strategic exposure to U.S. TIPS, given the current level of real interest rates, along with the potential for further inflation upside relative to market breakeven inflation rates.