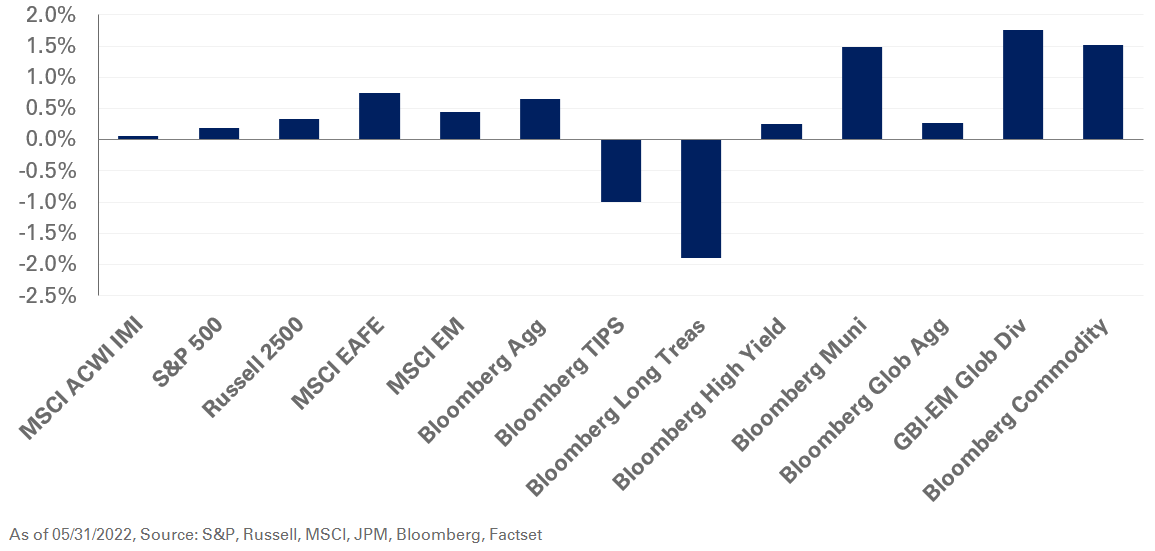

Despite a difficult start to the year, global equities modestly rebounded in May. The S&P 500 Index eked out a gain of 0.2% for the month, even as mega-cap technology names faltered with rising interest rates and earnings pressure. Growth equity underperformed value with the Russell 1000 Value Index gaining 1.9%, while the Russell 1000 Growth Index lost 2.3% last month. Outside the U.S., the dollar weakened in May, supporting returns for non-U.S. assets; the MSCI ACWI ex-U.S. Index gained 0.7%.

As anticipated, the Federal Reserve raised the benchmark interest rate by 50 basis points to a range of 0.75%-1.00% and announced that the balance sheet runoff would begin in June. The market is still pricing in two sequential 50-basis-point rate hikes in June and July, but expectations through the remainder of 2022 moderated given potential growth concerns and elevated, though declining, headline inflation figures. U.S. yields were volatile in May with the 10-year yield ending the month five basis points lower, while the 30-year yield increased 11 basis points.

In real assets, supply constraints continued to apply upward pressure in commodity markets. Spot WTI Crude Oil gained 9.6% for the month – pushing year-to-date gains to 52.2% – given disruptions fueled by the war between Russia and Ukraine.

At NEPC, our stance towards risk assets is unfavorable given the uncertain dynamics around growth and inflation. As a result, we recommend building exposure to short-term investment-grade credit as higher yields offer an attractive defensive position. In addition, we still encourage investors to maintain a dedicated allocation to assets that support liquidity needs in periods of stress.