All asset classes were in the black in March as markets saw no signs of an economic slowdown in the U.S. in the first quarter, while the Federal Reserve continues its efforts to steer the economy to a safe landing. Markets have priced in a safe landing—a stable path back to inflation of 2% with no recession along the way. So far, the labor market has been resilient with inflation moderating. That said, the path to the Fed’s inflation target of 2% remains unclear.

Commentary from the central bank and the FOMC interest-rate dot plot data from March indicates a willingness to allow inflation to run above 2% for a while to pave the path for a safe economic landing. This last mile in the battle against inflation, that is, getting inflation from 3%-4% to the Fed’s target of 2%, will likely prove to be the most difficult as the central bank weighs possible job losses, market volatility, and a slowing of the U.S. economy against trying to get inflation 100-to-200 basis points lower.

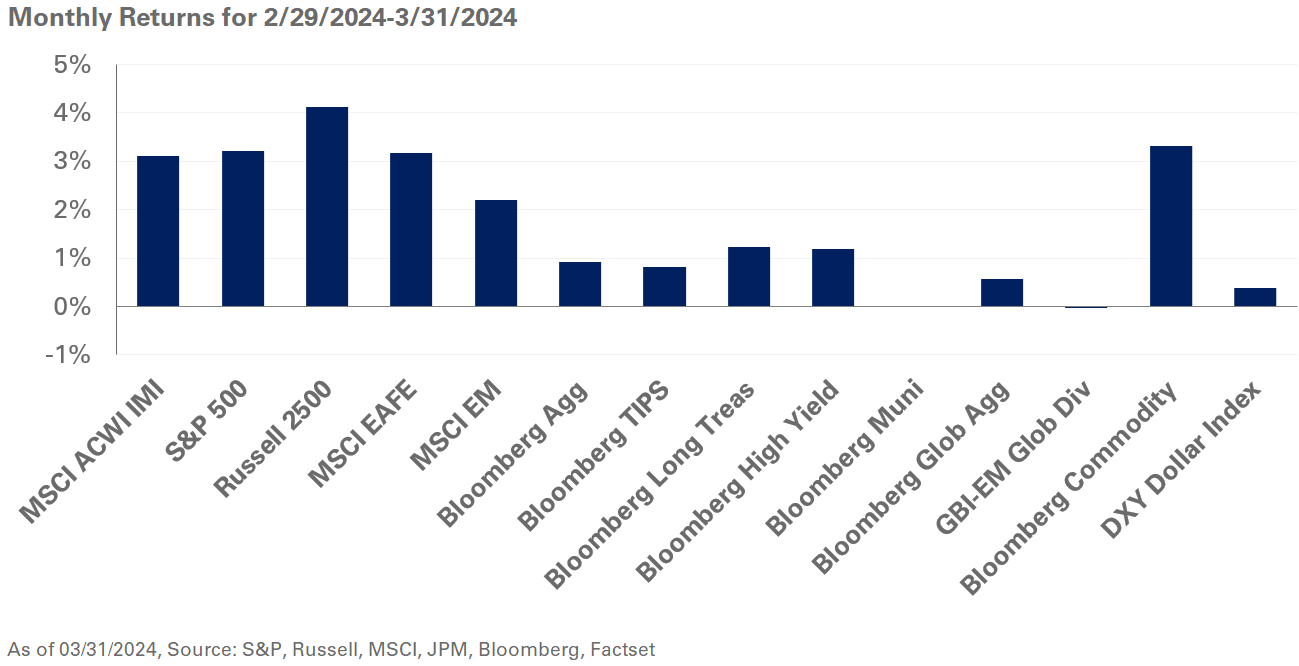

The continuing economic momentum bolstered stocks last month with U.S. large-cap equities up 3.2%, according to the S&P 500 Index; U.S. small-cap stocks rose 3.6%, as measured by the Russell 2000 Index. Global equities gained 3.1%, according to the MSCI ACWI Index, helped by the MSCI EAFE Index posting returns of 3.3%; emerging market equities lagged with the MSCI Emerging Markets Index up 2.5%.

Despite the dovish Fed commentary and increase in interest rate expectations for 2026 by FOMC members, interest rates held steady in March. The two-year U.S. Treasury yield—a proxy for short-term market expectations for Fed interest rate policy—was unchanged at 4.6%, and consistent with Fed guidance on three expected cuts in 2024. Long-bond yields were also flat in March with the 10-year yield at 4.2% and 30-year at 4.4%.

Within credit, spread levels moved lower with investment-grade spreads appearing moderately tight at 90 basis points. However, high-yields spreads are aggressively tight at just under 300 basis points. The carry on high-yield debt continues to be attractive, but we express caution around the entry point at these spread levels.

Elsewhere, energy markets ended the month higher with WTI Crude Oil spot prices up 5% in March and 15.7% in 2024. Overall, the Bloomberg Commodity Index decreased 3.3% last month but remains in the black so far this year with gains of 2.2%.

Given the rally in U.S. equities, we suggest investors reduce S&P 500 exposure, while maintaining U.S. large-cap value positions. Real interest rates have risen to attractive levels and we recommend taking advantage of the available real yield of 2%-3% and adding exposure to TIPS amid the continued uncertainty around inflation. Lastly, we suggest holding greater levels of cash within safe-haven fixed-income exposures and encourage investors to maintain greater levels of portfolio liquidity.