The Federal Reserve stepped in last month, infusing liquidity into the banking sector, in a bid to quell the rising turmoil precipitated by higher interest rates and the collapse of a handful of banks.

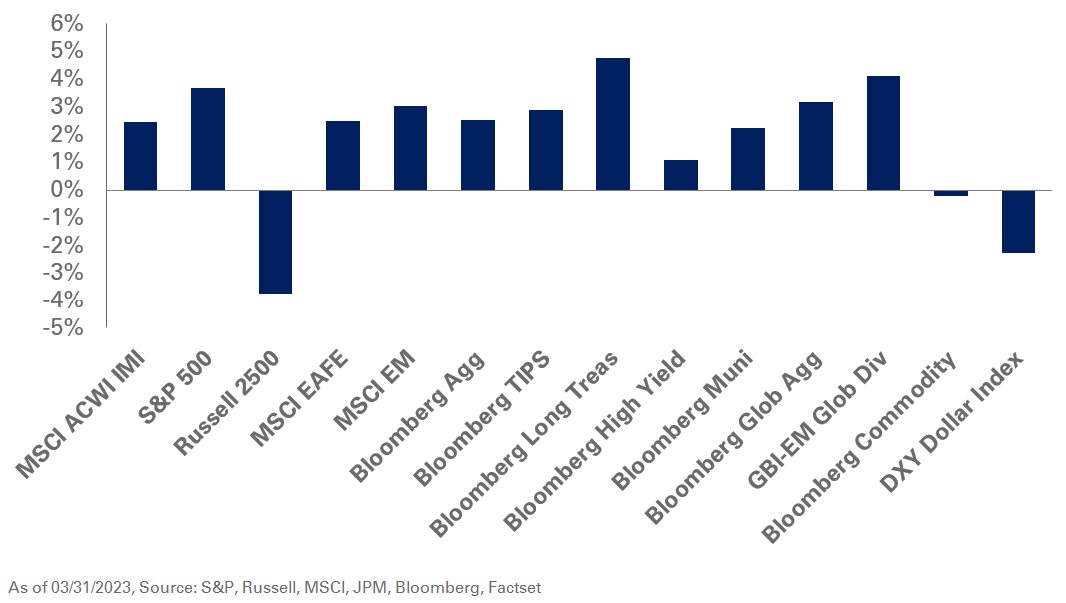

Equities got a boost as the central bank’s actions eased the concerns of investors with markets pricing in lower interest rates in the future in anticipation of slowing consumer demand and moderating inflation. The S&P 500 Index gained 3.7% and the MSCI EAFE Index was up 2.5% in March. During the same period, emerging markets returned 3%, according to the MSCI EM Index. Growth equities outperformed value stocks last month with the Russell 1000 Growth Index gaining 14.4% while the Russell 1000 Value Index was up 1%.

On the heels of the failure of Silicon Valley Bank (SVB), the Fed created a Bank Term Lending Program in an effort to provide a backstop to the banking sector. This would enable banks to borrow against their bond holdings at face value for up to a year, allowing them to meet an influx of deposit withdrawals without selling their bond holdings at a loss. Many banks are holding unrealized losses with respect to their bond holdings purchased prior to the Fed raising interest rates by over 400 basis points over the course of the last 12 months. We believe SVB is an outlier in terms of the relative size of unrealized losses it was carrying. To that end, it appears to be an isolated case rather than a widespread systematic issue.

In fixed income, returns were bolstered by the downward pressure on interest rates. Treasury yields moved lower with 10- and 30-year yields decreasing 42 and 24 basis points, respectively.

Elsewhere, energy markets were in the red in March. Meanwhile, precious metals ended the month higher likely due to a flight to safety amid concerns around the banking sector. During this period, the Bloomberg Commodity Index remained mostly flat, down 0.2%.

Against a backdrop of encouraging economic data and dissipating concerns around the banking sector, we suggest investors hold equity allocations near strategic targets. Given our upward bias in terminal rate projections relative to the market’s pricing amid softening—though still elevated—inflation levels, we also recommend exposure to U.S. large-cap value stocks.