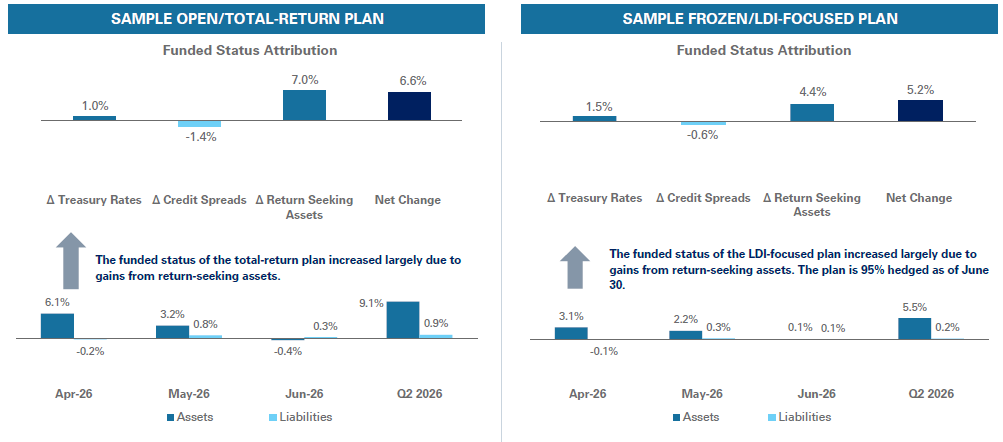

International and domestic equities posted notable gains in the second quarter of 2026 driven by strong earnings in the technology sector. The funded ratio for plan sponsors also increased as discount rates were largely unchanged during the quarter.

For the three months ending on June 30, the 30-year Treasury yield increased three basis points to 4.91%. During this period, credit spreads tightened three basis points. The discount rate for the open total-return plan decreased six basis points to 5.76%, and the discount rate for the frozen LDI-focused plan decreased two basis points to 5.54%. The funded status of our total-return and LDI-focused plans saw fairly significant increases, rising 6.6% and 5.2%, respectively.

Total-return plans may want to consider the impact of rate changes on plan liabilities and the role of LDI in light of the current rate environment. For certain plan sponsors, lower rates may increase liabilities and reduce funded status, which could lead to higher required contributions and PBGC variable-rate premiums. NEPC consultants are available to discuss the impact and cost of various pension finance and derisking strategies in light of rate movements and volatility in the market.

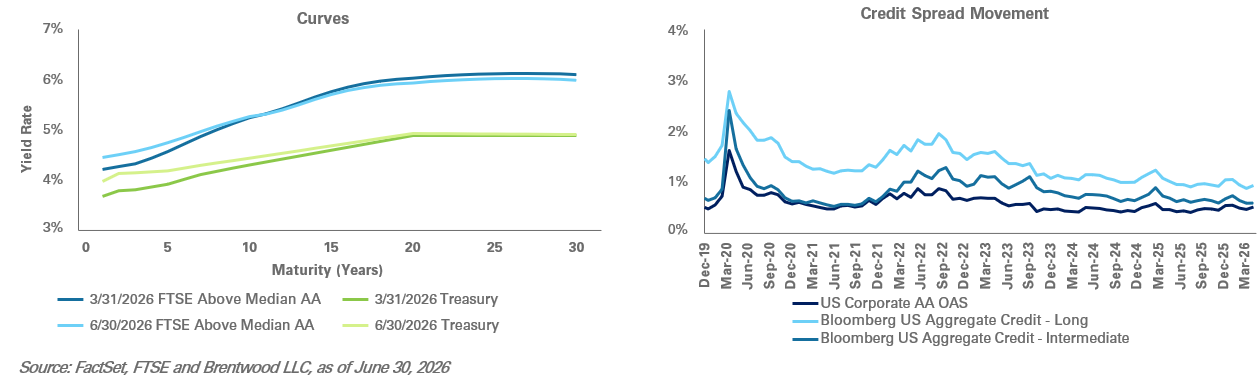

Sources: FactSet, FTSE and Brentwood LLC, as of June 30, 2026

Rate Movement

Retiree Buyout Index

Retiree Buyout Index

The Buyout Index for retirees is estimated to be approximately 107% of PBO, as of June 30, 2026.

Recent Insights from NEPC

The Art of Terminating a Corporate Pension Plan, Part 3

Insights From the NEPC Conference: The State of AI in Institutional Investing

Recent Corporate Pension Headlines

The PBGC clarified treatment of annuity buyouts for active participant reduction reporting

• In its first opinion letter in 24 years, the PBGC noted that an annuity buyout does not create an active participant reduction

reportable event simply because active participant counts decline. Participants transferred to an insurer are no longer covered by PBGC insurance and should not be included in the reporting.

• The opinion is notable in the ongoing pension risk transfer (PRT) litigation environment as it states that pension risk transfers are not evidence of financial weakness; at the same time, it reaffirms the loss of PBGC protection for participants once transferred to an insurer.

Sources:

PBGC. (June 15, 2026). Reportable Event Opinion Letter https://www.pbgc.gov/documents/opinion-letter-26-001