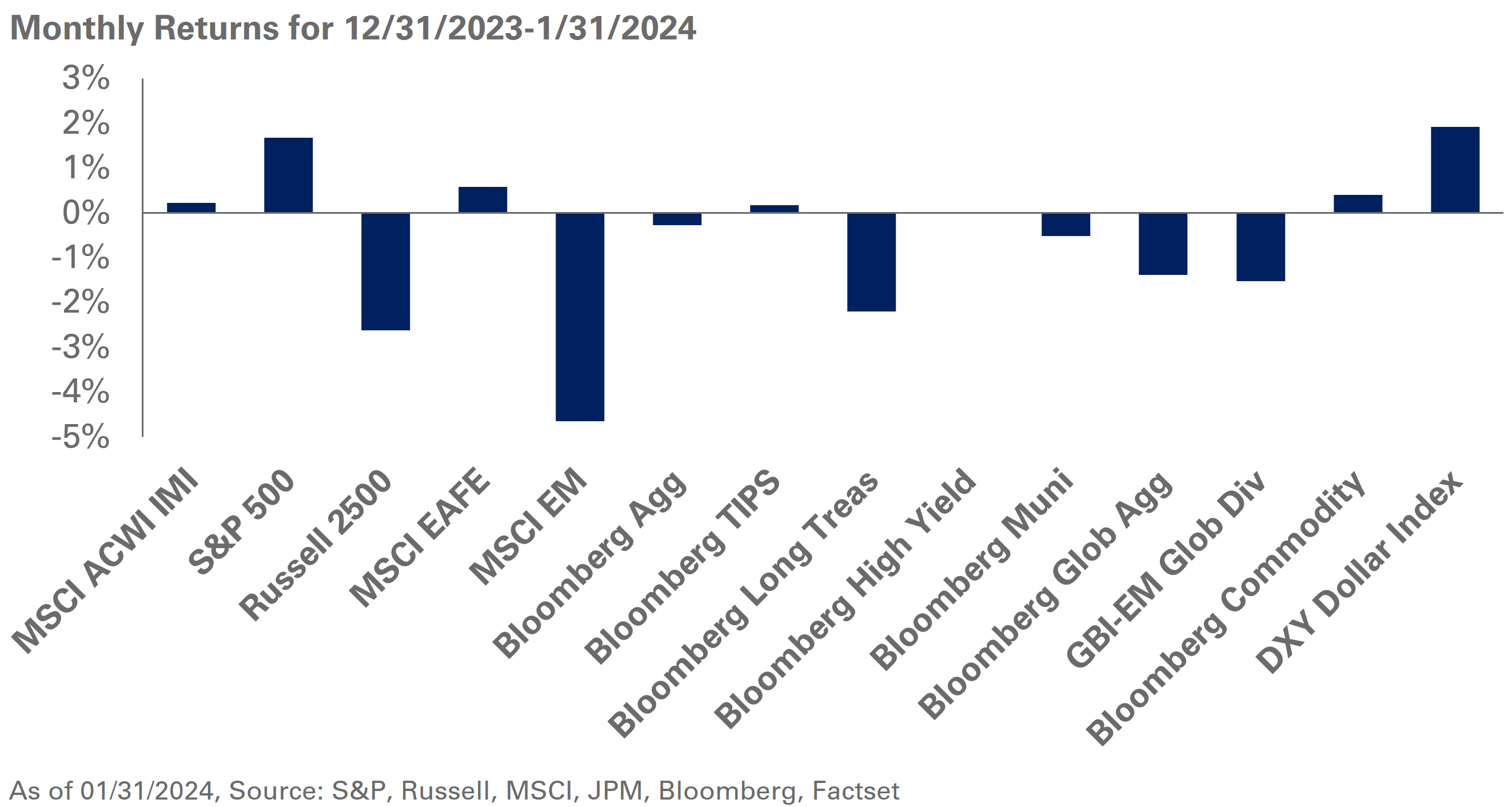

Asset returns were mixed in January as better-than-expected economic returns and a hawkish Federal Reserve weighed on markets. The U.S. economy expanded at an annualized rate of 3.3% in the fourth quarter fueled by strong consumer spending. Spending data released last month still point to a resilient consumer with personal consumption expenditures beating expectations and rising 0.7% over December. In addition, JOLTS data beat expectations, rising to nine million job-openings in December. In a widely expected move, the Fed held rates steady at a range of 5.25%-5.50%, with Fed Chair Jerome Powell signaling that a rate cut at the next meeting in March is unlikely. As a result, longer-tenor interest rates rose with the 10-and 30-year Treasury yields rising seven and 16 basis points, respectively.

In equities, the S&P 500 Index gained 1.7%, with the so-called Magnificent 7 companies contributing 0.7% of the broader index returns. Notably, small-cap equities underperformed with the Russell 2000 falling 3.9% as uncertainty surrounding interest rates weighed on sentiment.

Meanwhile, outside the U.S., a stronger dollar weighed on equity returns with the MSCI EAFE Index rising 0.6% and 2.6% in dollar and local terms, respectively. Chinese equites continued to sell off despite new stimulus efforts by the People’s Bank of China; as a result, the MSCI China and Emerging Market Index fell 10.6% and 4.6%, respectively.

Elsewhere, within real assets, WTI Crude oil spot prices rose 5.5% in January as ongoing attacks on freight shipping through the Suez Canal and disruptions to Russian energy infrastructure raised supply concerns.

Following the recent strength in U.S. equities, we continue recommending investors reduce S&P 500 and U.S. mega-cap exposure in favor of U.S. value positions and high-yield credit. Additionally, while expectations around rate cuts have waned, we believe the market is aggressive projecting falling interest rates in the near term. To that end, we are comfortable with clients holding higher levels of cash to bolster liquidity in portfolios. We also recommend investors broadly evaluate the risk-return benefit of fixed income and look to add U.S. TIPS to capitalize on the current real-rate environment.