Risk-off sentiment washed over markets in February as the Ukraine-Russia conflict fueled concerns around the potential impact on the global economy, the geopolitical landscape, and capital markets. While our expertise is focused on investment portfolios, we are mindful of the suffering and our thoughts and compassion are with those impacted.

Though the conflict was the main focus for markets, expectations of tighter monetary policy around the world continued to accelerate amid ongoing inflation pressures. As such, interest rates trended higher and global equities fell during the month – offering little respite for investors.

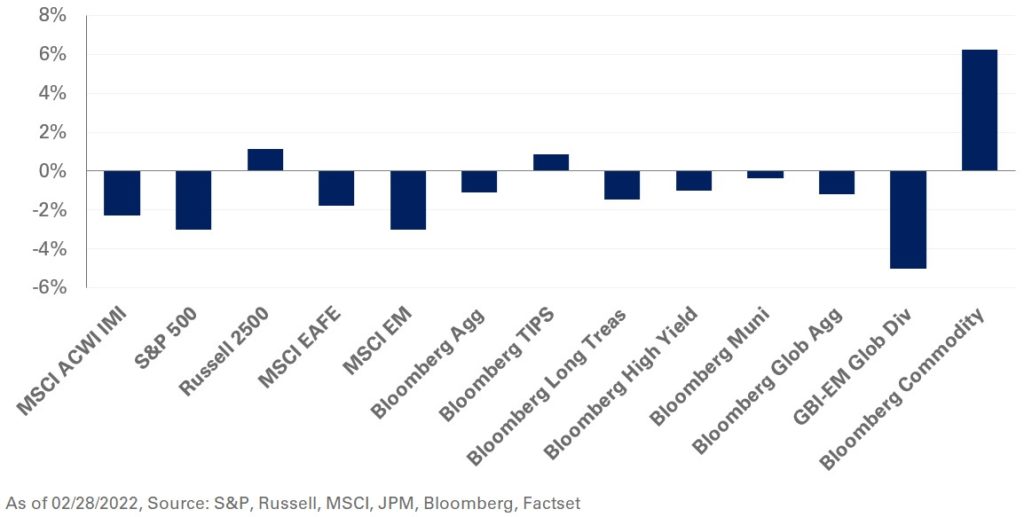

The S&P 500 Index fell 3% in February—the largest monthly pullback since the start of the pandemic in March 2020—pushing year-to-date losses to 8%. Value stocks continued to outperform growth given the upward pressures on interest rates and inflation. Outside the U.S., the MSCI EAFE and MSCI Emerging Markets indexes fell 1.8% and 3%, respectively.

In fixed income, global yields trended higher. The 10- and 30-year Treasury yields increased five and eight basis points, respectively; fixed-income benchmark returns were broadly negative for the month. Inflation expectations also increased as the 10-year breakeven inflation rate jumped 19 basis points; the Bloomberg U.S. TIPS Index gained 0.9% last month.

Emerging market debt came under pressure, underscoring the impact of the Ukraine-Russia conflict. The spread on the JPM EMBI Global Diversified Index increased 67 basis points to 411, resulting in a decline of 6.5% for the month. During the same period, local currency debt also declined, with the JPM GBI-EM Global Diversified Index losing 5%.

Meanwhile, in real assets, commodities continued their run, with the Bloomberg Commodity Index gaining 6.2% in February; the Ukraine-Russia conflict will likely have spillover effects for global commodity supplies.

While the ongoing conflict may increase near-term market volatility, we remain constructive on public equities and encourage adding to U.S. large-cap value exposure to help mitigate the impact of rising interest rates on portfolios. Despite the recent hawkish shift from the Federal Reserve, we recommend investors maintain a dedicated allocation to safe-haven fixed income to support portfolio liquidity needs and provide downside protection in periods of stress.