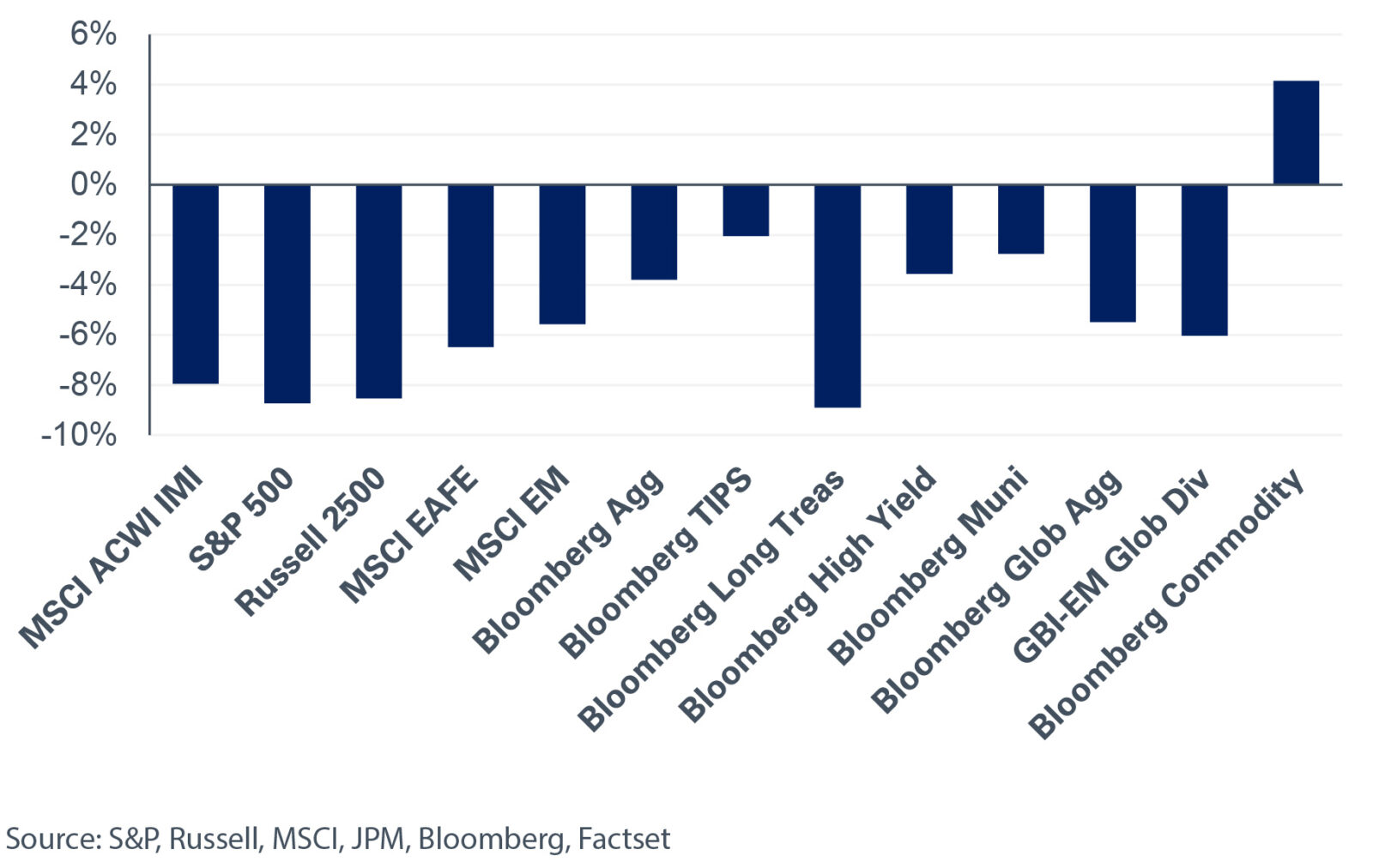

Tighter monetary policy, geopolitical tensions and lockdowns in China dragged down equities in April. The backup in global bond yields remained a headwind for stocks, with growth equities generally underperforming value. In the U.S., the S&P 500 plummeted 8.7%—its largest monthly decline since March 2020. Outside the U.S., markets outperformed on a relative basis despite the dollar strengthening by 4.9% during the month, as measured by the DXY Index; the MSCI EAFE and MSCI Emerging Markets indexes were down 6.5% and 5.6%, respectively.

Global yields moved higher last month – weighing on broad fixed-income returns. In the U.S, the 10- and 30-year Treasury yields increased 56 and 49 basis points, respectively. The move followed the release of the March FOMC minutes, which highlighted a more hawkish policy stance, and another elevated inflation print: U.S. CPI-U increased 1.2% in March, or an 8.5% annualized rate. As a result, longer-duration fixed-income indexes suffered the largest losses, with the Bloomberg Long Treasury and Long Credit indexes falling 8.9% and 9.6%, respectively. In credit, option-adjusted spreads widened in April, with the biggest moves occurring in the lower-quality credit space. The spread on the Bloomberg U.S. Corporate High Yield Index rose 54 basis points, resulting in a monthly index loss of 3.6%.

In real assets, the Bloomberg Commodity Index was up 4.1% during the month as geopolitical tensions continued to impact supply dynamics.

NEPC’s stance towards risk assets is more subdued given the greater uncertainty around growth and inflation. As such, we recommend reallocating overweight risk-asset positions to build exposures to short-term investment-grade credit as higher yields increase expected returns. We continue to recommend investors maintain a dedicated allocation to assets that support liquidity needs in periods of stress.