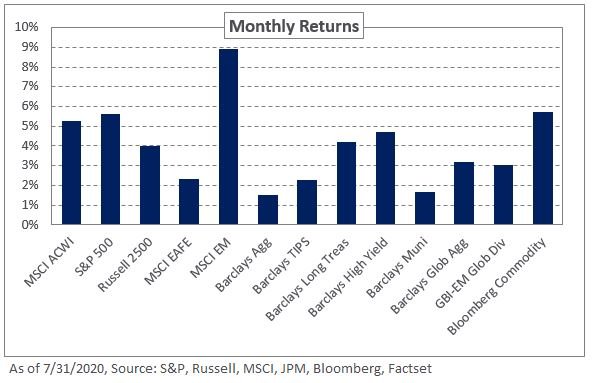

Risk assets enjoyed another strong month as optimism around a COVID-19 vaccine, hopes of additional stimulus, and better-than-expected quarterly corporate earnings in the US bolstered investor sentiment. The S&P 500 Index was up for the fourth straight month, increasing 5.6% in July; the gains pushed the index into positive territory with a year-to-date returns of 2.4%. This confidence comes despite a record spike in infection rates in many parts of the country, and macroeconomic data underscoring the economic fallout from the pandemic.

Non-US equities also benefitted from the risk-on sentiment and the continued weakness in the dollar in July. During this period, emerging markets led performance with gains of 8.9%, driven by a significant rally in Taiwanese stocks following an announcement that chip maker Intel Corp. may outsource production to Taiwan Semiconductor Manufacturing Company. Developed market stocks, excluding the US, rose 2.3%, according to the MSCI EAFE Index; the euro appreciated 5.3% relative to the dollar in July. The DXY Index, which represents a trade-weighted index for the US dollar, fell over 4% — its worst monthly performance since 2010.

In fixed income, global rates moved lower, reflecting the bond market’s concerns over the economy. In the US, yields on 10- and 30-year Treasury bonds fell 11 and 21 basis points, respectively. The larger move on the long end of the yield curve incited a rally in longer-dated Treasuries, with the Barclays Long Treasury Index increasing 4.2% in July. In addition, US real rates moved further into negative territory, causing the US 10-year breakeven rate to tick up 21 basis points. In credit, spreads continued to tighten amid central bank intervention in the fixed-income market. The largest movement occurred in lower-quality credit with the option-adjusted spread on the Barclays US Corporate High Yield Index down 138 basis points, fueling returns of 4.7% for the index in July.

In real assets, broad commodity indexes rallied amid higher spot gold prices. Gold increased 11% during the month, pushing year-to-date returns to 30.3%; the recent rally reflects weakness in the US dollar and the asset’s negative correlation to real rates, which have moved lower.

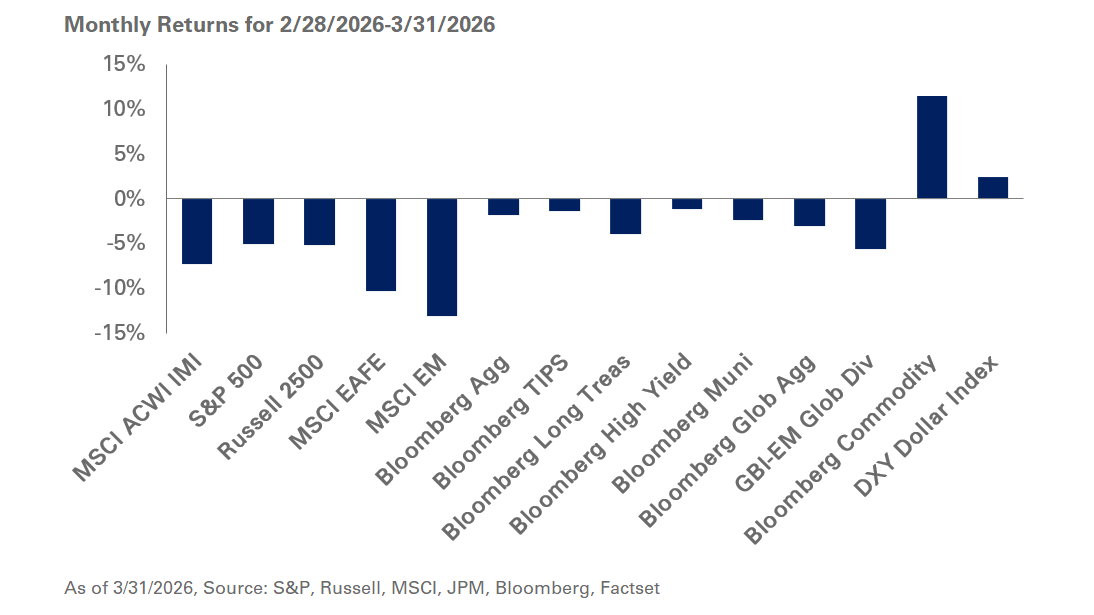

While the recent performance of risk assets has been encouraging, we remind investors of the significant uncertainties still surrounding the global economy. As such, we expect heightened volatility to continue across capital markets given the wide range of potential economic outcomes. We recommend investors maintain discipline and remain mindful of market liquidity. To that end, we suggest a dedicated allocation to Treasuries to support liquidity levels and cash-flow needs as potential market dislocations can introduce bouts of illiquidity across publicly-traded markets.