SUMMARY

- Quantifying the “value” of a managed account provider can be challenging.

- The advantages of managed accounts from a net-of-fee performance perspective can be debated, but some participants may receive enough personalization to truly benefit.

- Managed account providers look at personalization factors differently, and a vastly different risk level may be set by providers for the same participant.

- In addition to ensuring participants receive value, plan sponsors should evaluate whether the selected managed account provider’s philosophy and methodology for personalizing risk level are aligned.

INTRODUCTION

Managed account providers often tout personalization as a key benefit. But the reality is that most participants enrolled in managed accounts tend to receive an experience similar to that of a target date fund (TDF) while paying higher fees. While some highly engaged participants could benefit from a managed account investing approach, the question of who may benefit isn’t straightforward, as different providers can arrive at distinctly different answers for the same participant.

WHAT DOES PERSONALIZATION MEAN?

If personalization is a key benefit, then how do we define personalization? A variety of definitions exist, including methods of communication, forecasting future outcomes, and asset allocation. Given the fact that managed account provider’s fees are explicitly for an ERISA 3(38) discretionary asset allocation, it makes sense to focus on the personalization received from an asset allocation (or risk level) perspective.

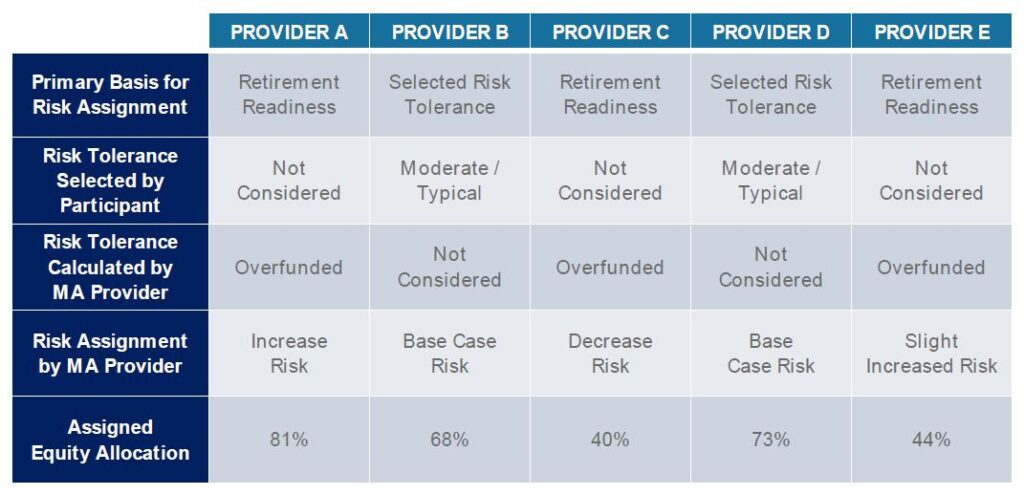

To show the differences in risk level personalization, consider Jethro, a 55-year-old planning for retirement. He self identifies as having a moderate/typical risk tolerance, and expects to retire on time, as he is currently well-funded for retirement. He enrolls in a managed account within his 401(k) plan and provides all information asked about his financial situation (which is uncommon). However, he doesn’t enter the composition of his outside accounts (very few participants do).

Based on this input, the risk levels set by five different providers are shown in the table below.

Notice that all five providers have the same information but use different methodologies to arrive at different portfolios. Providers A and C use retirement readiness as the primary basis for assigning risk level and yet arrive at vastly different equity allocations. Providers B, D and E use selected risk tolerance (in this instance, moderate/typical) to set risk level and arrive at distinctly different equity allocations. How are we to determine which provider is “correct” in this scenario?

ALIGNING INVESTMENT PHILOSOPHY WITH MANAGED ACCOUNT PROVIDERS

Even if plan sponsors believe their plan could benefit from managed accounts, we maintain that an in-depth due diligence process is required to ensure sponsors are aligned philosophically with the way a managed account provider sets risk level. This is especially necessary since asset allocation philosophies vary between managed account providers and may be quite different than the in-plan TDF. To complicate matters further, sponsors may only have access to one or two managed account providers, depending on the recordkeeping platform.

Clearly, the decision to offer managed accounts is more nuanced and less straightforward than one might think. It is crucial for plan fiduciaries to critically evaluate each managed account provider to ensure investment philosophies align.

The first step on your journey will be to ensure there is alignment of governance evaluating the managed accounts providers. We have seen administrative committees assume the responsibility of selecting a managed account provider, which makes sense as managed accounts were originally introduced as an add-on feature to recordkeeping services. However, since managed account providers are assuming the role of a 3(38) discretionary investment manager, we believe this evaluation process should be conducted by the same investment committee that selects any other investment options offered in the plan; doing so can improve the industry by promoting competition and more robust solutions, rather than simply concluding that managed accounts and personalized portfolios are inherently correct.

At NEPC, we can help plan sponsors with these analyses and can work to include different providers on new recordkeeping platforms to better align with sponsors’ beliefs. Contact us to learn more about our services and how we can help plan participants save for the future.