2025 was a Tough Year to Be an Active Manager in Emerging Markets.

During this period, the quality factor underperformed across equities, hitting emerging markets the hardest. At NEPC, we recommend investors stay the course as we maintain that diversification across countries, sectors and factors is crucial to avoid large deviations from benchmark performance. We believe that despite the recent underperformance, quality companies remain fundamentally strong and are supported by robust earnings and sound management.

Furthermore, we have seen short-term underperformance in emerging markets equities is often due to index construction and country/sector weights, and not a breakdown in the quality factor itself. Historically, we have seen quality as a factor has delivered superior returns in all major equity indexes, including emerging markets, and we expect this trend to continue as market conditions normalize.

In general, a quality company is one that usually has robust financials backed by a sustainable competitive advantage. Typically, metrics used to describe the quality factor are a high return on equity, stable and healthy cash flows, and a strong balance sheet. For instance, for MSCI, the companies that make it into the global index provider’s quality index have to meet three primary conditions: high return on equity, stable year-over-year earnings growth, and low financial leverage1. Given that these tend to be successful businesses, we believe they make sound investments as long as they are purchased at an attractive entry point.

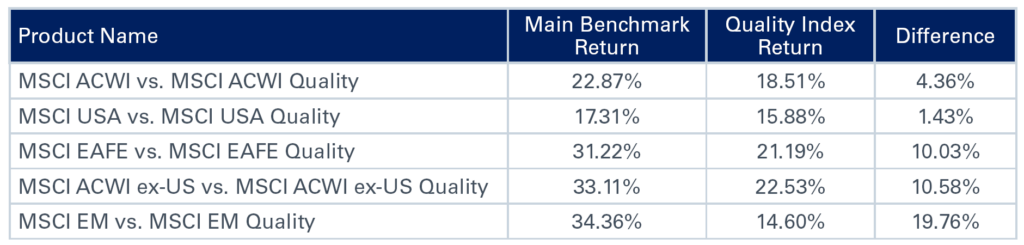

In 2025, the underperformance of quality has been stark across the global equity indexes, but most prominent in international markets. In particular, their underperformance within emerging markets has stuck out like a sore thumb with the MSCI EM Index outperforming the MSCI EM Quality Index by about 20% in 2025. This has had an outsized impact on many fundamental active managers that tend to have a bias towards quality companies.

1 MSCI, as of January 6, 2025 (https://www.msci.com/indexes/group/quality-indexes)

The underperformance of quality in emerging markets in 2025 can be attributed to two main trends:

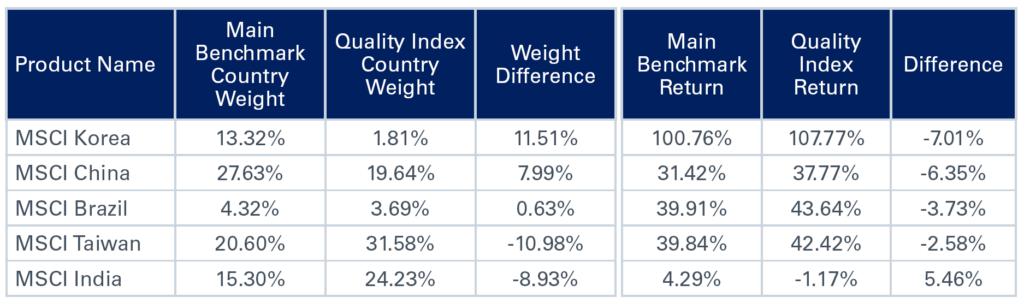

1. Country weight differences between the quality and main indexes: the large difference in returns between the MSCI EM and MSCI EM Quality indexes is mostly due to differences in country weights in the benchmarks.

Interestingly, it was not that quality stocks within countries underperformed, but that the Quality Index is constructed such that it is overweight Indian companies and underweight Korean and Chinese ones. In fact, for the MSCI Korea, MSCI China, MSCI Brazil, and MSCI Taiwan indexes, quality actually outperformed (see table below). Given that the EM Quality Index has larger weights to India and lower weights to China and Korea, and China and Korea outperformed and India underperformed in 2025, the MSCI EM Quality Index considerably lagged the MSCI EM Index’s 34.4% return compared with the MSCI India Index’s 4.3% gain.

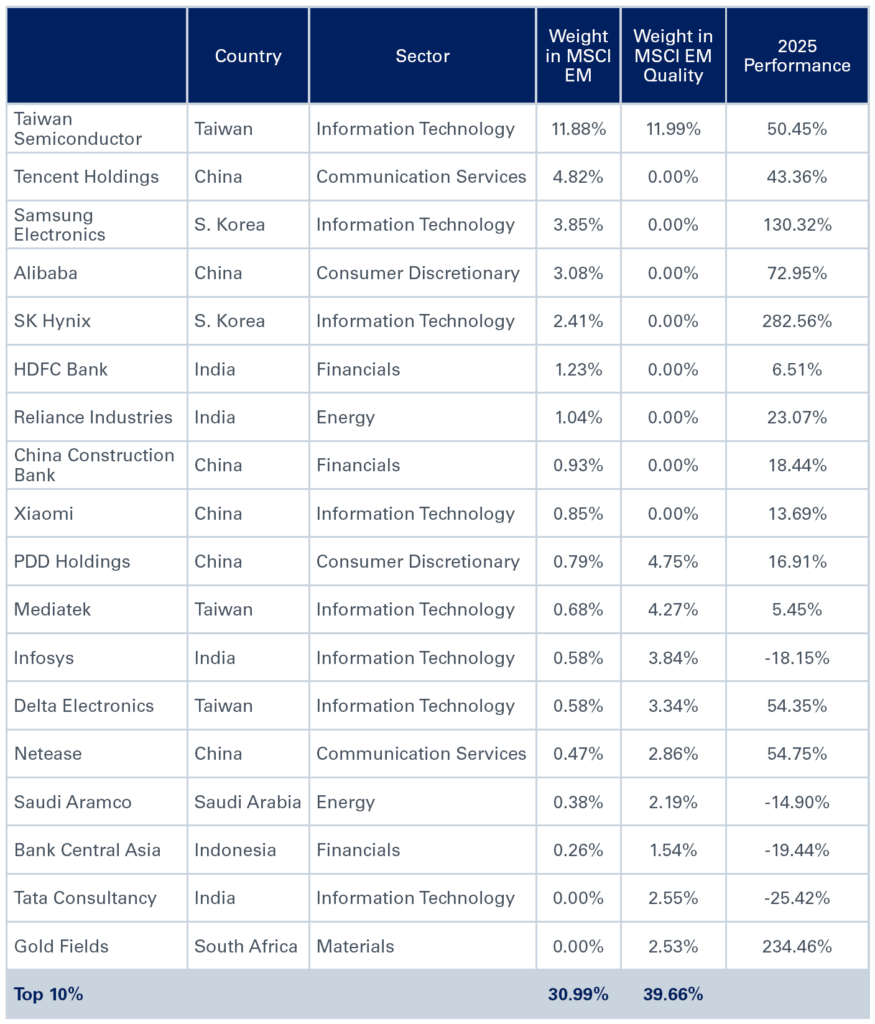

2. The underlying top names are different between the MSCI EM Quality and MSCI EM indexes with the largest names in the EM Index that turned in a strong performance in 2025 excluded from the EM Quality Index.

When looking at the table below, it is easy to see why the MSCI EM Quality Index has underperformed as many of its top 10 names had lackluster returns in 2025.

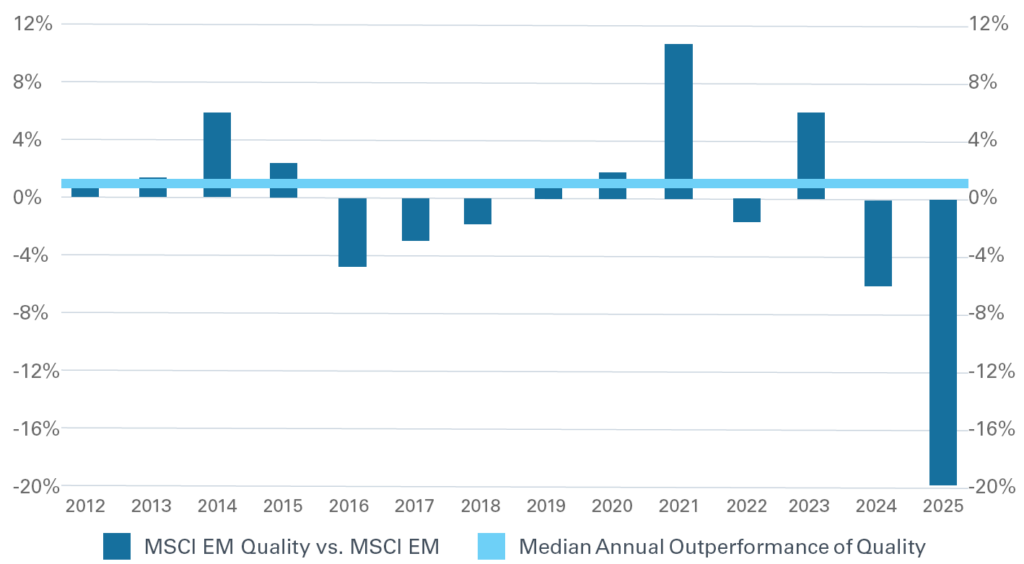

Last year witnessed the largest divergence in 25 years between quality and its peers. While the underperformance has been pronounced, it has especially hurt the relative performance of active managers that have a bias to quality companies in India.

To be sure, these quality companies may have been somewhat overpriced, but earnings will ultimately determine the success of a company. Quality companies are supported by strong earnings and should continue to do well in the future, and we believe active managers with a quality bias will succeed in the long run. Within emerging markets, we have generally seen quality outperform in most calendar years.

MSCI EM Quality vs. MSCI EM

At NEPC, we are optimistic of the quality factor outperforming in the future. Periods of underperformance tend to be brief, and we expect quality to rebound as fundamentals reassert themselves. We believe active management is still integral to investing in companies in emerging markets to successfully take advantage of the inequalities and inefficiencies in these regions.

Our role is to find the appropriate active manager and strategy in these spaces, and help our clients build diversified portfolios that can withstand multiple and varied economic cycles. To learn more, please reach out to your NEPC consultant.