After a disappointing era of returns for high-yield investment strategies, where both actively managed and passive approaches had their shortcomings, it’s time to take a fresh look at the asset class and revisit the merits of both implementation options.

Even though the past decade has yielded lackluster results, a fundamentally different market backdrop and advancements in the bond trading ecosystem within high yield offer investors better options. While several factors—risk profile, client objectives and manager selection—remain critical, clients looking to allocate to high yield may recognize benefits when considering both approaches in their implementation.

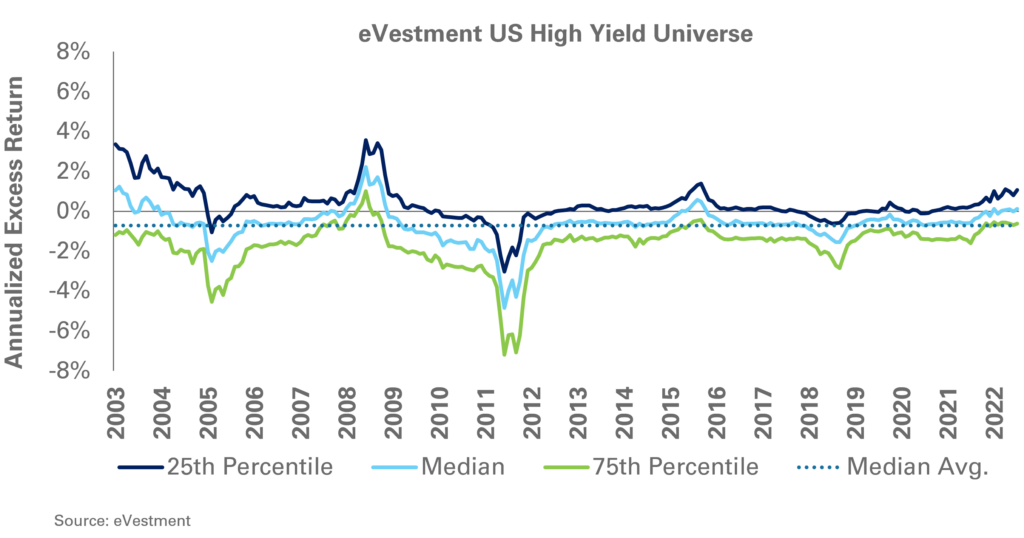

High-yield investment has been traditionally dominated by fundamental investors with a background in credit lending, where the guiding principle is to avoid credit losses. This approach was challenged in the aftermath of the global financial crisis, when demand for yield was high, low rates equaled lower costs of capital for leveraged companies, and borrowers with poor credit fundamentals were able to kick the can down the road and survive. Managers were reluctant to embrace these riskier companies, which led to a defensive/lower-beta posture compared to the indexes. This resulted in consistent underperformance for active managers, as more often than not you were paid to take on greater credit risk than most managers were willing to underwrite.

At NEPC, we believe it’s too soon to write off active management within high yield. We believe fundamental credit underwriting and careful manager selection can offer compelling alpha, especially in the post-quantitative easing world that we have entered. Many strategies lean defensive/lower beta, while some are more concentrated with higher levels of idiosyncratic risk. In order to appropriately set expectations, understanding these characteristics is a critical step before allocating.

At NEPC, we believe it’s too soon to write off active management within high yield. We believe fundamental credit underwriting and careful manager selection can offer compelling alpha, especially in the post-quantitative easing world that we have entered. Many strategies lean defensive/lower beta, while some are more concentrated with higher levels of idiosyncratic risk. In order to appropriately set expectations, understanding these characteristics is a critical step before allocating.

At the same time, we recognize that past results in active management have been mostly underwhelming, dragged down further by relatively hefty fees—in the 40-to-70 basis points range—for institutional investors. It isn’t surprising then that the conversation turned towards passive strategies. However, even that approach has proven frustrating for investors.

The premise for passive management is that you can buy the market cheaply and mimic it at low cost. However, historically, within high yield, steep trading costs, opaque market pricing and lack of availability of many bonds held by the indexes led to an inability to effectively mimic the broad high-yield indexes. Exchange-traded funds (ETFs) and other index products turned to custom indexes aimed at the largest issues and issuers in an attempt to create an investable universe and index unit of measurement they could replicate. That said, investor experience trailed even these tailored indexes, especially after fees.

When compared to indexing in large-cap equities or investment-grade fixed income, high-yield indexing still has ways to go in terms of cost and tracking error. However, enhanced indexing and quantitatively driven strategies are showing more promise, in large part, due to the evolution of the market trading structure. As the trading mechanisms used in the bond market have evolved and become more efficient, the ability to implement large trades has led to significantly reduced transaction costs for investors, improving outcomes for these systematic, index-based approaches.

Although imperfect, we feel increasingly comfortable with ETFs as a tool for both clients and active managers to gain relatively efficient exposure to high-yield beta. A key benefit that ETFs bring to portfolio management is the instant issuer diversification. Being able to have a highly diversified portfolio in short order should help to reduce idiosyncratic credit risk.

For questions or to learn more, please contact your NEPC consultant.