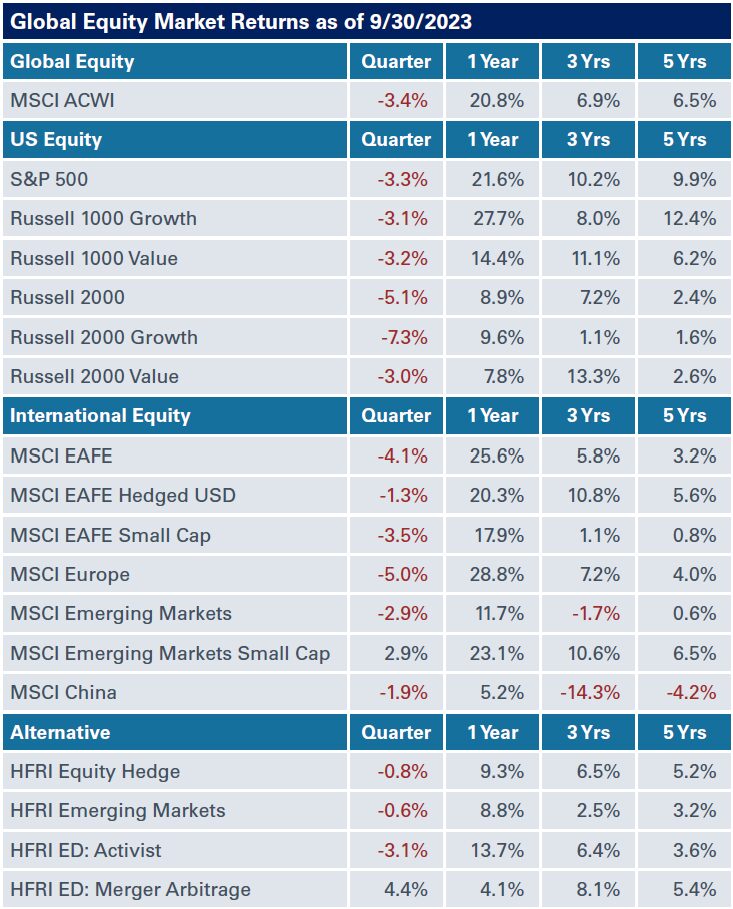

Global Equities

Equities cooled off in the third quarter with most major indexes experiencing a quarterly loss. With the current interest-rate headwind, investors looked to fixed-income investments as an alternative to stocks. For the three months ended September 30, the S&P 500 Index fell 3.3%, faring modestly better than the tech-heavy Nasdaq which closed 3.9% lower. So far this year, U.S. equity performance remains fairly strong, with the S&P 500 up 13% and the Nasdaq gaining 27% through the third quarter.

Small-cap stocks experienced larger drawdowns in the quarter versus large-cap equities, fueled by investors favoring the perceived safety of large- and mega-cap companies. the Russell 2000 was down 5.1% for the quarter.

Meanwhile, in international markets, the MSCI EAFE fell 4.1% in the third quarter, while the MSCI EM slid lower by only 2.9%, modestly outperforming international developed and domestic equities, despite a strong U.S. dollar and volatility in China.

Fundraising activity in the US PE market was healthy in the first nine months of 2023, albeit muted relative to the highs of past years. Total fundraising levels increased from the prior quarter to $242 billion. Fundraising in the US venture market increased from $33 billion in the second quarter to $43 billion, but activity has decelerated significantly from its peak in 2022.

Exits in PE-backed companies declined during the quarter, reaching a three-year low. US venture deal activity remained flat in Q3 but has declined to 2019 levels as venture capitalists slowed their pace of deployment and portfolio companies streamlined their organizations to increase cash runway.

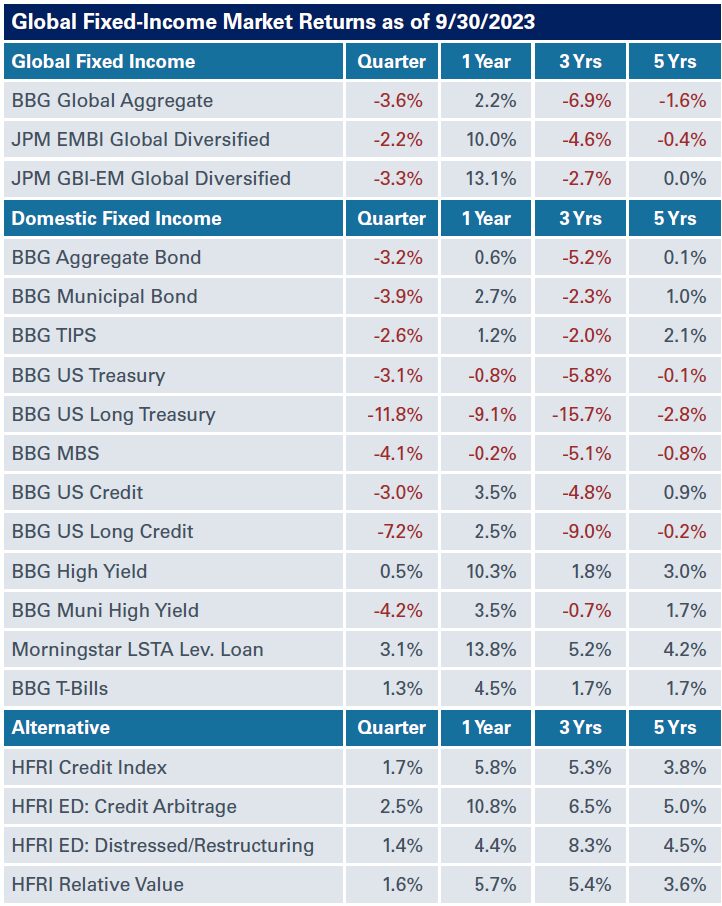

Global Fixed Income

Fixed-income markets succumbed to the Federal Reserve’s continued messaging of higher-for-longer interest rates. The FOMC raised rates by 25 basis points in July and held steady in September. Treasuries sold off during the quarter, led by the long end of the yield curve in a bear steepening move. The yield on the 30-year Treasury climbed by 84 basis points to end the quarter at 4.7%, while the five-year Treasury note yield climbed 45 basis points to end the quarter at a 4.6% yield. This led total returns to be negative for most fixed-income indexes in the investment-grade universe. Overall, credit spreads in fixed income were relatively unchanged. The return-seeking segments of the fixed-income market, such as high-yield and levered loans posted positive returns for the quarter.

Fixed-income markets succumbed to the Federal Reserve’s continued messaging of higher-for-longer interest rates. The FOMC raised rates by 25 basis points in July and held steady in September. Treasuries sold off during the quarter, led by the long end of the yield curve in a bear steepening move. The yield on the 30-year Treasury climbed by 84 basis points to end the quarter at 4.7%, while the five-year Treasury note yield climbed 45 basis points to end the quarter at a 4.6% yield. This led total returns to be negative for most fixed-income indexes in the investment-grade universe. Overall, credit spreads in fixed income were relatively unchanged. The return-seeking segments of the fixed-income market, such as high-yield and levered loans posted positive returns for the quarter.

Real Assets

Real asset returns continued to produce mixed returns in the third quarter, with even more variance than in the previous quarters. The Bloomberg Commodity Index was up 4.7%. Crude oil was the star of the quarter, with a 29.8% gain; it led all other real asset segments, bringing its return for the year up to 14.4%. In public real estate, the NARIET Global REIT Composite Index was challenged for the quarter, posting a 6.5% loss. While, gold has now given back nearly all its 2023 gains, posting a 3.7% loss for the three months ended September 30.

During this period, global natural resource stocks gained 3.7%, mirroring the 3.7% loss the asset class faced in the prior quarter. NEPC maintains a favorable view of natural resource equities due to the potential for inflation to remain elevated.

The midstream energy market was positive as well, with the Alerian Midstream Index up 2.5% for the quarter. The S&P Global Infrastructure Index took a dip in the third quarter and was down 7.3%. Similar to global natural resources, NEPC is constructive on infrastructure equities as a potential hedge against high inflation, though we continue to favor private markets when it comes to implementing infrastructure in a portfolio.

Private real estate returns declined for the fourth straight quarter, with the NCREIF ODCE posting a -1.99% preliminary gross return for the quarter. The negative total return is inclusive of a -2.9% asset appreciation, as the effects of rising interest rates continue to put pressure on asset values.

While private real estate equity has suffered from higher rates and the market correction, real estate debt is offering attractive opportunities for investors. Higher interest rates, impending loan maturities, and a pullback from traditional lenders has led to higher return expectations that rival what can be expected from value-add real estate equity.

Private infrastructure strategies continue to garner increased interest among investors, and NEPC investment advisory solutions team is particularly constructive on the tailwinds driving communications infrastructure, renewable energy, and energy transition strategies.