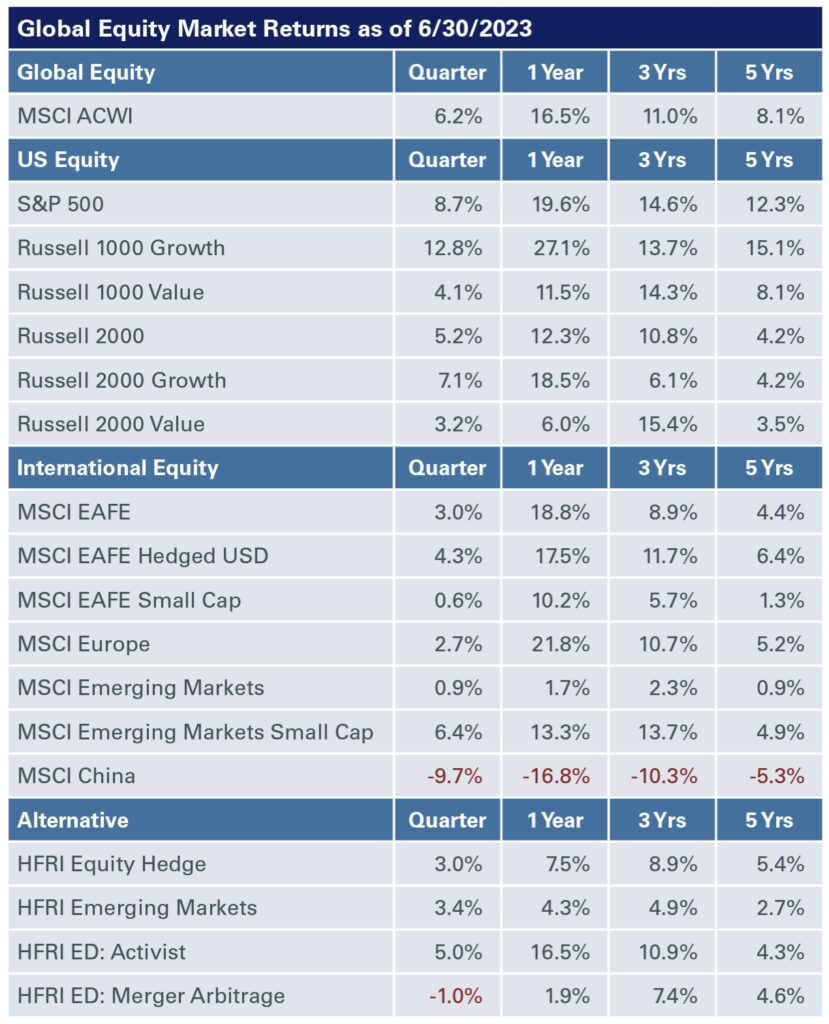

Global Equities

Building off the strong start to the year, U.S. stocks extended their winning streak into the second quarter. During this period, the S&P 500 advanced nearly 9%, the Nasdaq was up 13% and the Russell 2000 increased just over 5%. These gains were primarily fueled by technology companies, heightening concerns around narrowing market breadth and the undue influence of the so-called magnificent seven or super seven—Meta, Amazon, Apple, Nvidia, Microsoft, Google and Tesla—on domestic equities.

Meanwhile, international stocks were also in the black but lagged U.S. stocks on a year-to-date basis. The MSCI EAFE Index gained 3%, while the MSCI Emerging Markets Index was up almost 1% in the second quarter.

Elsewhere, in U.S. private equity, fundraising activity totaled $83.3 billion for the three months ended June 30, up from $66.8 billion the prior quarter, according to data from Preqin. During the same period, fundraising in the U.S. venture market increased to $21.6 billion from $11.7 billion in the first quarter, but activity has decelerated significantly from its peak in 2022 and lags recent vintages.

New deal activity, at $191 billion, according to data from PitchBook, was down 16% from the prior quarter. On the venture side, deal activity totaled $39.8 billion of estimated value in the second quarter, a 13% drop from the first quarter and down 48% from a year ago, as venture capitalists slowed their pace of deployment and portfolio companies streamlined their organizations to increase cash runway. Exit activity rebounded in the three months ended June 30, totaling $87 billion, a 15% jump from the first quarter; exit value for venture was a modest $5.5 billion, a 69% drop from a year earlier.

Global Fixed Income

Fixed-income markets continue to be caught in a tug-of-war between interest rates and credit spreads. Rates rose moderately in the second quarter but were offset by declining spreads.

Fixed-income markets continue to be caught in a tug-of-war between interest rates and credit spreads. Rates rose moderately in the second quarter but were offset by declining spreads.

While the Federal Reserve raised rates by 25 basis points in May—its tenth consecutive hike—it hit pause in June amid a backdrop of declining inflation and a resilient labor market. Still, Fed chair Jerome Powell reiterated that the central bank’s job will not be done until inflation comes down to its stated target of 2%, underscoring the likelihood of more rate hikes in the future.

For the three months ended June 30, spreads tightened across sectors, with investment-grade and high-yield corporate bonds declining 15 basis points and 65 basis points, respectively. Yields rose, with the 10-year Treasury increasing 33 basis points to 3.81%. Alternatives also benefitted, with the HFRI Credit Index producing a 1.45% total return.

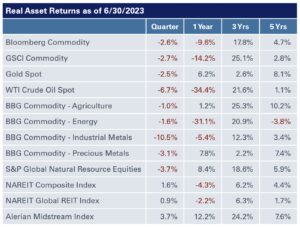

Real Assets

Returns were a mixed bag for real assets in the second quarter with the Bloomberg Commodity Index down 2.6%, bringing year-to-date losses to 7.8%. During the same period, crude oil experienced declines of 6.7%, leading to losses of 11.9% so far this year. The midstream market was a bright spot among natural resources, with the Alerian Midstream Index up 3.7% for the quarter. Gold posted a 2.5% loss in the second quarter, giving up a part of its gains from the prior quarter.

Returns were a mixed bag for real assets in the second quarter with the Bloomberg Commodity Index down 2.6%, bringing year-to-date losses to 7.8%. During the same period, crude oil experienced declines of 6.7%, leading to losses of 11.9% so far this year. The midstream market was a bright spot among natural resources, with the Alerian Midstream Index up 3.7% for the quarter. Gold posted a 2.5% loss in the second quarter, giving up a part of its gains from the prior quarter.

Meanwhile, global natural resources were down 3.7% in the second quarter and the S&P Global Infrastructure Index was flat for the quarter, down 0.1%. NEPC is also constructive on infrastructure equities as a potential hedge against high inflation; we continue to favor private markets when it comes to implementing infrastructure in a portfolio.

Elsewhere, in public real estate, the NARIET Global REIT Composite Index was up a modest 0.9%. Private real estate declined for the third straight quarter, with the NCREIF ODCE posting a 2.7% preliminary gross loss for the quarter as rising interest rates continue to pressure asset values following historically high returns prior to 2022. Private real estate valuations have been slow to adjust relative to the sharp correction in REITs. That said, fundamentals remain healthy for most sectors, though uncertainty around the future demand for traditional office space continues to weigh on markets.