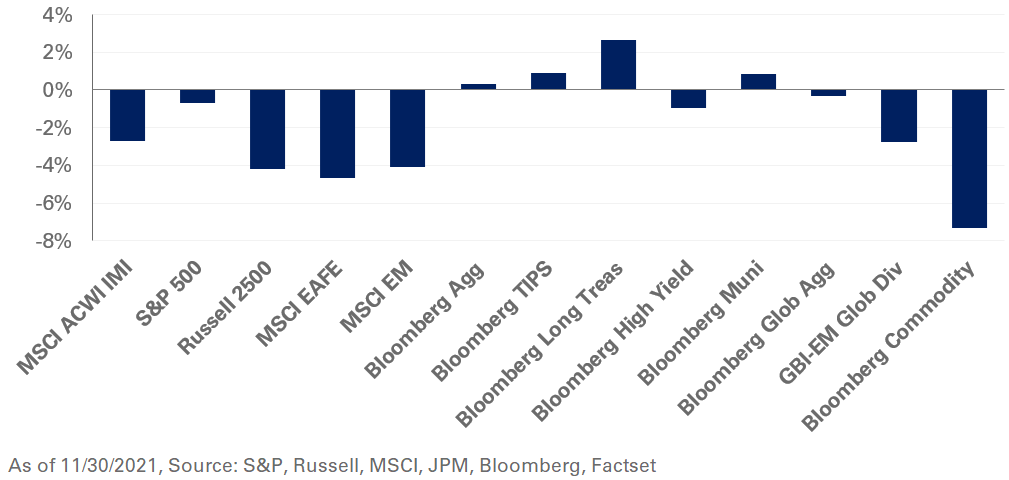

Risk assets sold off in November as investor sentiment weakened amid concerns around ongoing inflation and the pandemic. In the U.S., October Consumer Price Index data revealed higher-than-expected prices with headline CPI increasing 6.2% year-over-year. In an unexpected shift, the Federal Reserve Chair Jerome Powell assumed a more hawkish tone and signaled that tapering of asset purchases could end a few months sooner. As a result, the S&P 500 Index ended the month down 0.7%.

International equities lagged with the MSCI EAFE and the MSCI Emerging Market indexes posting losses of 4.7% and 4.1%, respectively. In Europe, a fresh wave of COVID-19 and increasing rates of hospitalization have forced tighter restrictions and lockdowns, dampening the prospects for economic growth.

Consistent with risk-off sentiment, global yields broadly shifted lower. The U.S. yield curve flattened with the 10- and 30-year Treasury yields falling 12 and 16 basis points, respectively. As a result, longer-duration assets outperformed, with the Bloomberg Long Treasury Index up 2.7%.

In real assets, the Bloomberg Commodity Index fell 7.3%, weighed down by energy prices. WTI crude oil spot prices plunged 20.7%—the largest monthly decline since March 2020—amid concerns over weaker growth due to the omicron variant and news that major economies, including the U.S., would release oil from their strategic reserve to rein in rising energy prices.

Despite recent volatility, the market environment remains supportive for equities as below-median credit spreads in the public-debt space imply muted forward-looking returns. We recommend investors maintain a dedicated allocation to safe-haven fixed income to provide downside protection and support portfolio liquidity needs. At the same time, we caution investors to brace for potentially higher inflation relative to market expectations and suggest adding large-cap value exposure to U.S. stocks to help mitigate the impact of rising interest rates on portfolios.