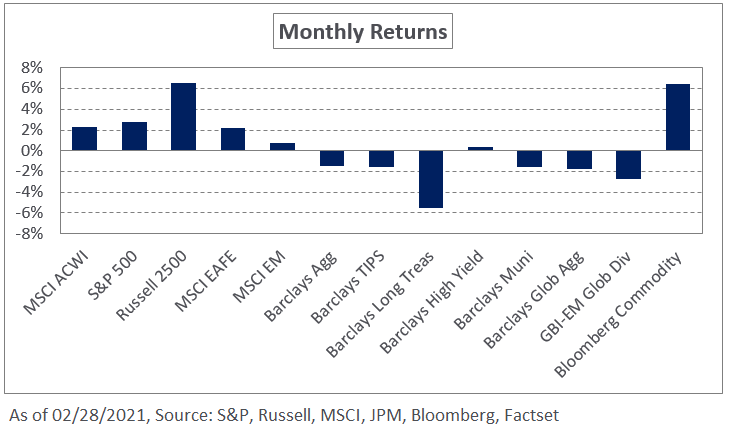

Following the volatile month of January, U.S. equities got off to a strong start in February, bolstered by optimism around ongoing inoculations, improving COVID-19 trends, and the proposed stimulus plan. However, as the weeks progressed, continued upward pressure on interest rates negatively impacted stocks amid concerns around the potential implication for valuations. Despite the increase in yields, the S&P 500 Index rose 2.8% during the month; during this period, small-cap US equities outperformed, increasing 6.2%, as measured by the Russell 2000 Index. Outside the United States, the MSCI EAFE and MSCI Emerging Markets indexes posted gains of 2.2% and 0.8%, respectively, in February.

In fixed income, global yields moved higher as the market began pricing in higher growth and inflation expectations. In the U.S., the front-end of the curve remained relatively flat, while the belly and long-end of the yield curve moved notably higher. The curve steepening resulted in the widest spread between the 10- and 2-year yields since 2015. The 10- and 30-year yields increased 37 and 34 basis points, respectively, during the month. As such, rate-based indexes posted losses with the Barclays U.S. Treasury Index down 1.8% and the longer-dated Barclays Long Treasury Index falling 5.6% in February. In addition, spreads moved modestly lower in investment-grade credit. More significant spread tightening occurred in lower-quality securities with the option-adjusted spread on the Barclays U.S. Corporate High Yield Index tightening 36 basis points to 3.26%.

Within real assets, spot WTI crude oil extended its rally, increasing 17.9% in February; the rally reflects improving growth prospects and the impact of extreme weather in many areas of the U.S. Meanwhile, the broad Bloomberg Commodity Index was up 6.5%.

The improving macroeconomic backdrop has resulted in higher growth and inflation expectations in the near term. While the corresponding increase in interest rates is notable, we still recommend investors maintain a dedicated allocation to Treasuries to support liquidity levels and cash flow needs in the event of a market dislocation. Further, the ongoing support from monetary and fiscal interventions continues to provide a supportive environment for equities. To that end, we encourage investors to maintain strategic equity targets even in the face of modestly higher interest rates.