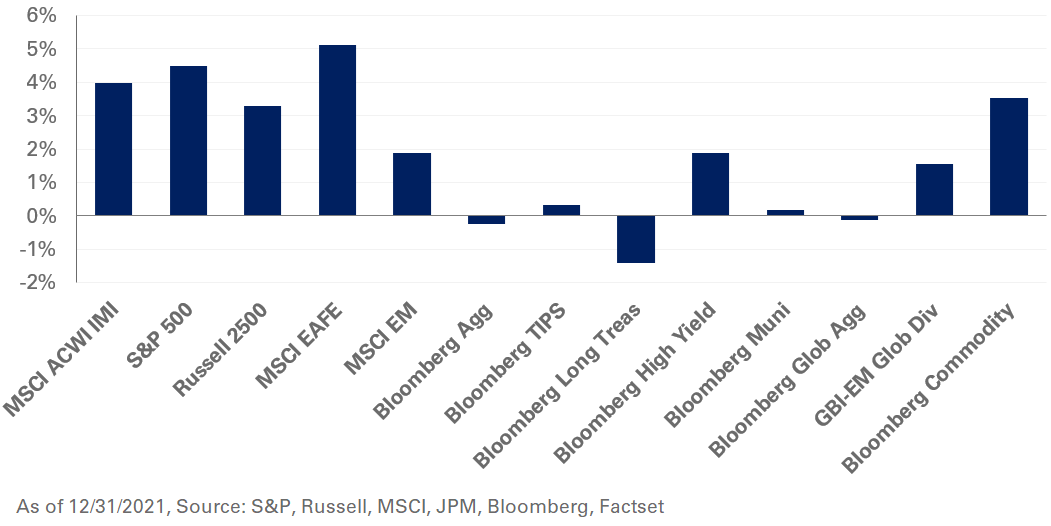

Global equities ended 2021 with a bang as strong earnings growth and positive risk asset sentiment bolstered returns in December. In the U.S., the S&P 500 Index gained 4.5%, pushing year-to-date returns to a whopping 28.7%. Non-U.S. equities were also in the black with the MSCI EAFE and MSCI Emerging Markets indexes up 5.1% and 1.9%, respectively. Chinese equities were an outlier, falling 3.2% last month as mega-cap technology names remain under pressure.

In fixed income, 10- and 30-year Treasury yields increased eight and 12 basis points, respectively, against a backdrop of inflationary tensions and less accommodative central bank policy. Public debt markets echoed the positive risk asset sentiment with spreads—particularly in lower-quality credit—grinding lower. The option-adjusted spread on the Bloomberg U.S. Corporate High Yield Index fell 54 basis points to 2.83%, resulting in a 1.9% monthly return.

In real assets, commodities gained despite ongoing concerns over the Omicron COVID variant, with the Bloomberg Commodity Index adding 3.5% in December. Spot WTI Crude Oil ended the year at $75 a barrel, posting returns of 55.6% for the year – the largest annual increase since 2009.

Despite recent volatility, the market environment remains supportive for equities as below-median credit spreads in the public-debt space imply muted forward-looking returns. We recommend investors maintain a dedicated allocation to safe-haven fixed income to provide downside protection and support portfolio liquidity needs. At the same time, we caution investors to brace for potentially higher inflation relative to market expectations and suggest adding large-cap value exposure to U.S. stocks to help mitigate the impact of rising interest rates on portfolios.