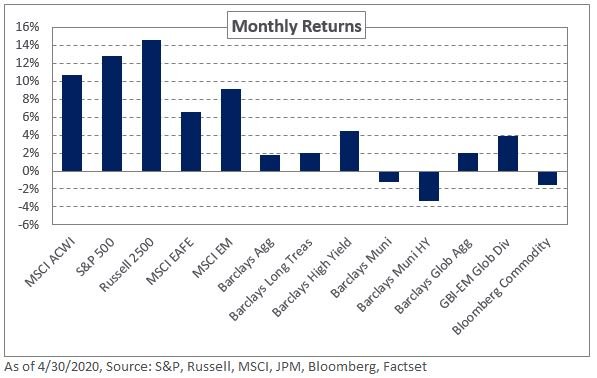

Following a disappointing first quarter, risk assets moved higher in April as central banks and governments stepped in with monetary and fiscal stimuli to stem the fallout from the COVID-19 pandemic. While the virus continued to spread, new data indicated a slowing pace in infections and hospitalization rates in some regions. To that end, the focus is shifting toward reopening economies, providing a tailwind for global risk assets. In the US, the S&P 500 increased 12.8% last month, though the index is down 9.3% for the year. International and emerging market equities were also in the black in April though weak economic data dampened sentiment; the MSCI EAFE Index posted returns of 6.5% and the MSCI Emerging Markets increased 9.2%.

The Federal Reserve, in its meeting last month, expanded its programs announced in March that are aimed at supporting consumers and small businesses. In addition, rates held steady at a range of 0.00% to 0.25%, nearly unchanged month-over-month. Within credit, spreads moved significantly lower following the widening in March. The option-adjusted spread on the Barclays Investment Grade Credit Index declined 70 basis points to 2.02%, with the index returning 4.6% for the month. Lower-quality credit experienced a larger movement with the spread on the Barclays US Corporate High Yield Index declining 136 basis points to 7.44%, though spreads are 408 basis points higher so far this year; the index increased 4.5% during the month. Meanwhile, emerging market debt posted gains in April with local-currency debt outperforming hard currency; the JPM GBI-EM Global Diversified Index was up 3.9% bolstered by a modestly weaker dollar.

Real assets continued to be volatile last month as the tumult in energy impacted market pricing and sentiment. Spot WTI Crude Oil declined 8.1% last month, reflecting concerns around oversupply, storage capacity and demand. Mid-month, the May WTI crude oil contract fell to -$36.98, marking the first time in history a contract traded in negative territory. While commodities still face headwinds, most listed real assets rallied significantly off March lows. The midstream space experienced the biggest bounce with the Alerian Midstream Energy Index up 29.5% for the month, though it is still down 31.3% year-to-date.

While April offered some respite to risk assets, economic uncertainty remains. Recent economic data have provided a preview of the dramatic impact of COVID-19 on the economy, labor market and consumer confidence. We anticipate additional weakness in the second quarter, with a larger impact to corporate earnings as foreshadowed by recent revisions and suspended guidance. We expect volatility to continue across capital markets and remind investors to be disciplined and mindful of market liquidity.