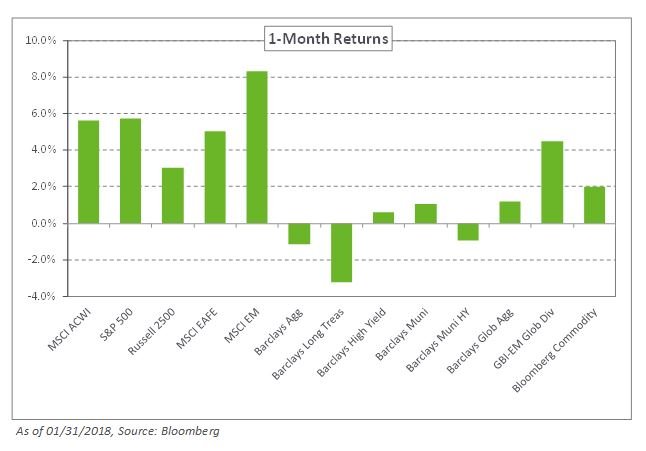

Global equities continued their winning streak in the new year. Emerging market stocks maintained their lead—gaining 8.3% in January, according to the MSCI EM Index—bolstered by a weaker US dollar, stronger commodity prices, and sustained economic growth. The S&P 500 and MSCI EAFE indexes posted returns of 5.7% and 5.0%, respectively. As the month ended, so did the run up in stocks; volatility rose across equity markets, fueling a moderate correction in early February.

Despite barely discernable changes in the communications from the major central banks in January, there appears to be a growing belief that stronger global economic growth will push inflation higher in the short term. As a result, government bond prices weakened on the month with the two-year Treasury increasing 26 basis points to 2.14%, for the first time since 2008. As such, Treasury-based indexes declined with the Barclays US Treasury Index and Barclays Long Treasury Index down 1.4% and 3.2%, respectively. The sell-off also extended to other developed markets, as yields rose 0.27% on the 10-year German Bund and 0.04% on Japan’s 10-year sovereign bonds. In contrast, emerging market local-government bonds rose 4.5%, according to the JPM GBI-EM Index, amid a weaker US dollar.

As we turn the page on a new year, our views are broadly unchanged. Despite the recent flare up in volatility, we still favor international developed and emerging market stocks over domestic equities as economic growth and earnings, combined with a lower starting point for valuations, provide a relatively attractive opportunity. For fixed income, we continue to advocate for reducing credit risks as future return expectations have declined with spreads well below median levels. Finally, we remind investors to remain committed to a risk-balanced approach and to evaluate market opportunities should a more significant short-term dislocation occur.