This is the second of a four-piece series under the heading, “Investing in Private Markets: Best Practices for Family Offices.” In the series, we focus on the unique challenges of investing in private markets and how family offices can most effectively address them.

Private markets are fundamentally different from public portfolios, and in our experience, not all principals are prepared for the differences in risk, return, and liquidity. The most common challenge is that principals must commit capital before it can be invested, so that the portfolio does not reach its target allocation on day one. Capital is drawn down over several years as the manager identifies and closes investments.

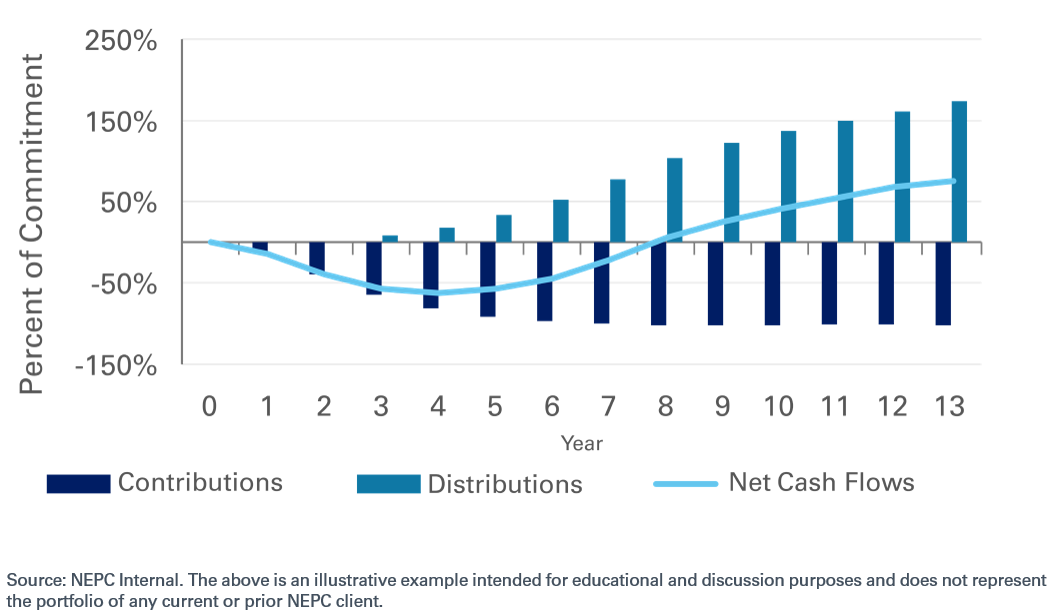

This dynamic produces the well-known “J-curve”. In the early years, most funds show a loss on paper. Only later, when the capital committed is higher and underlying companies grow and are sold, does the fund begin to appreciate, potentially substantially. It is this phase of private market ownership that people think of first, but it can take a decade or more of commitments to get there.

It has been our experience that the J-curve profile can have a dramatic impact on long-term portfolio strategy, investment timing, and liquidity planning. In this piece, we will discuss allocations, position sizing, and diversification in the context of a private markets program – as well as the best practices NEPC has encountered when addressing portfolio construction.

Determining The Right Private Markets Allocation

Because family circumstances vary widely, it can be difficult to identify rules of thumb when determining a private markets allocation. However, these best practices typically benefit family portfolios.

Best Practice #1: Communicate with the Family

In our view, family offices have more success when they put in place a foundation of communication and understanding with the family. That foundation has a few common components.

- Make sure the principals have clearly articulated their goals and objectives in the investment policy statement. This will provide the family office with a functional and consistent set of priorities.

- Model the impact a combined public/private portfolio will have on beta This will help families anticipate the performance profile they will experience.

- Map out potential impacts on risk as well as Private markets funds are long-term in nature and cannot be easily unwound, so risk preparedness is necessary.

Family offices must also be able to gauge how much of the portfolio can be invested in illiquid assets before liquidity risk becomes unacceptable. The liquidity dimension is critical so we will address it in greater depth in piece #3 of this series Retaining Portfolio Liquidity When Investing in Private Markets.

Best Practice #2: Tailor Sub-Asset Class Allocations to Family Needs

Within private markets, most family offices lean heavily into private equity, which may include buyout, growth equity, and venture capital funds.

But other private markets asset classes have advantages that might be a better fit for family needs. For example, some family offices supplement private equity with private debt including strategies such as direct lending, opportunistic credit, and asset-backed lending. Although private debt typically has a lower return target and less favorable tax treatment, it can play a useful role for families looking for higher income or a quicker return of capital.

Real estate and real assets round out the toolkit. Family offices often hold direct real estate outside of any managed program, which can limit the advantages of holding real asset funds. Nonetheless, in the right situation, a modest allocation to these types of funds can offer diversification, inflation protection, or income.

Portfolio Construction Guidelines

Best Practice #3: Develop a Pacing Plan

Because building a private markets allocation takes time, we believe a pacing plan is essential. A pacing plan tool models how much capital to commit each year, and across which strategies, to reach and maintain target allocations over time.

The pacing plan is a guide, not a rigid mandate. It should be revisited at least annually to reflect changes in portfolio values, market conditions, manager pipelines, and the client’s own circumstances.

Best Practice #4: Overcommit

A common best practice is to overcommit to a given allocation to keep actual investments close to the planned allocation1. That is, the family office must commit more total capital to private markets than their target allocation, because not all capital will be drawn down simultaneously, and older funds will be returning capital even as new ones are calling it. Overcommitting keeps the portfolio’s actual private markets deployment closer to the planned allocation, while allowing uncommitted capital to be invested.

Family offices who are inexperienced with overcommitment might benefit from having a dedicated investment staff or consultant support, since getting overcommitment right often requires sophisticated modeling.

Best Practice #5: Build Agreement on Position Sizing

Family offices tend to make better private markets decisions when there is broad agreement with principals about position sizes. There are several aspects to sizing that need to be discussed.

- Fund-level limits prevent any single fund from dominating the portfolio.

- Manager and strategy concentration limits ensure that a single strategy or sector does not inadvertently become a major economic bet.

- Co-investments and direct deals – which are typically undiversified holdings in a single company – should be sized with particular care, since they carry significant concentration risk and can meaningfully skew overall portfolio exposures

Best Practice #6 – Diversify

Diversification is as valuable in private markets as in public, but there are additional dimensions of diversification that need to be considered. Like in public markets, a private markets allocation should be diversified across sub-asset classes (equity, debt, real estate/real assets), sectors, themes, and geographies to control risk.

Best Practice #7 – Vintage Year Diversification

One of the most underappreciated risks in a private markets program is vintage year concentration, or the risk that too much capital is committed in a single year or narrow time window. Because private equity funds typically have 10-year+ lifespans, investors are essentially betting on the economic environment that will prevail over that decade. If the fund deploys capital into a frothy market, or if a recession hits in the early years, returns can be materially impaired.2

The best practice here is to spread commitments consistently across economic cycles — committing meaningful capital each year regardless of market sentiment. This approach smooths capital calls and distributions over time, reduces the impact of any single bad vintage, and creates a more predictable cash flow profile for the overall program. Vintage year diversification is also a valuable practice for managing liquidity challenges.

Best Practice #8 – Prioritize Good Managers

Ensuring a proper allocation and a broad range of diversification approaches can build success in a private markets program. But our experience working with family offices suggests that getting access to the best managers often has a larger impact on client success. A great manager opportunity is usually worth pursuing, even if it is outside a “planned” commitment year or changes your allocation planning.

Conclusion

In this piece, we have focused on central portfolio construction issues – the structural backbone of a sound private markets program. Other pieces in this series address further best practices, including manager selection, due diligence, and liquidity management.

A well-designed private markets program is a powerful tool for family offices, but that power comes with complexity, and complexity rewards thoughtful design and consistent execution. The families who benefit most from private markets are those who approach it with patience, discipline, and a trusted partner like NEPC who can provide both the framework and the ongoing guidance to navigate it well.

1Building a Private Capital Commonfund.org, April 2026 https://www.commonfund.org/cf-private-equity/committing-to-private-capital

2Lessons for Private Equity from the Last Downturn. McKinsey and Company, April 2020 https://www.mckinsey.com/industries/private-capital/our-insights/lessons-for-private-equity-from-the-last-downturn