Risk assets pushed higher this month as economies around the world began reopening and relaxing restrictions. While COVID-19 remains a dominant headline, news of progress in developing a vaccine and signs of a rebound in economic activity bolstered market sentiment.

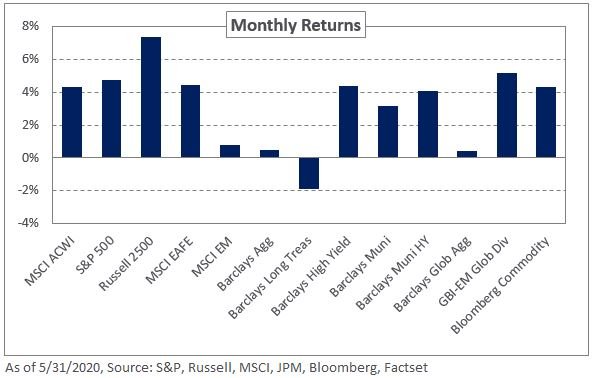

Over the past month, the US has been hit by a slew of weak economic data: the unemployment rate hit 14.7%, corporate earnings contracted significantly, and the CPI increased 0.3% year-over-year. Despite the bleak data, domestic equities pushed higher – extending their recent rally. The S&P 500 Index increased 4.8% for the month, though it is still down 5% so far this year. Further, small caps benefitted from the wave of risk-on sentiment, with the Russell 2000 Index gaining 6.5% in May.

International and emerging market equities also increased last month, with the MSCI EAFE and MSCI Emerging Markets indexes up 4.4% and 0.8%, respectively. International developed market assets experienced a currency tailwind as the dollar weakened relative to local currencies including the euro, Australian dollar, and Swiss franc.

In rates, global yields ended the month moderately higher. US rates experienced modest curve steepening with 10-year and 30-year Treasury yields increasing two and 18 basis points, respectively. In response, the Barclays US Long Treasury Index fell 1.9% during the month. Within credit, spreads broadly declined, with the largest tightening occurring in lower-quality areas. The option-adjusted spread on the Barclays US Corporate High Yield Index decreased 107 basis points in May to 6.37%, corresponding to a 4.4% return. Within emerging markets, hard and local currency debt increased 6.1% and 5.2%, respectively, according to the JPM EMBI Global Diversified Index and JPM GBI-EM Global Diversified Index; the recent performance can be attributed to a significant decline in spreads for the hard currency index and modest dollar weakness providing a tailwind to local returns.

Real assets broadly rallied this month as the Bloomberg Commodity Index increased 4.3%, with the largest gains coming from energy. Spot WTI Crude Oil recovered 83.7% for the month, reflecting a bounce back in demand as quarantine restrictions are eased and oil supply tightened; midstream energy also benefitted from the positive sentiment. The Alerian Midstream Energy Index increased 6.9% for the month, though it remains in the red with losses of 26.6% so far this year.

While the recent performance of risk assets has been encouraging, we remind investors of the significant uncertainties still surrounding the global economy. As such, we expect heightened volatility to continue across capital markets given the wide range of economic outcomes. To that end, we encourage investors to be disciplined and mindful of market liquidity.