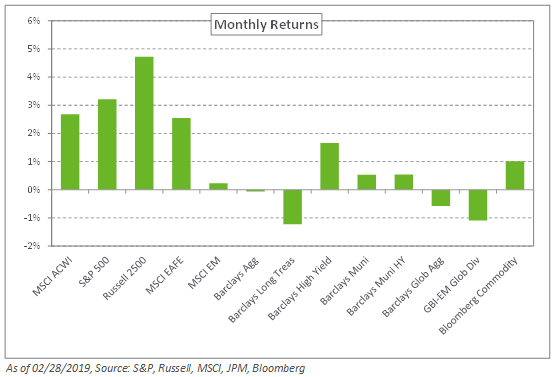

Global equities continued their winning streak in February as concerns surrounding US economic growth faded and the outlook for a US-China trade deal improved. As a result, the S&P 500 Index increased 3.2% during the month. Chinese stocks returned 3.5%, according to the MSCI China Index, relative to broad emerging markets which rose a modest 0.2% as measured by the MSCI Emerging Markets Index.

Despite the renewed popularity of risk assets, a dovish tilt from the Fed caused fixed-income yields to remain relatively stagnant with the 10-year US Treasury yield increasing nine basis points to 2.72%. In credit, US high-yield spreads, as measured by the Bloomberg Barclays US Corporate High Yield Index, continued to decrease relative to the beginning of the year, returning 1.7%. In emerging markets, local-currency bonds fared worse than hard-currency debt amid modest dollar strength, fueling losses of 1.1% in the JPM GBI-EM Global Diversified Index and gains of 1% in the JPM EMBI Global Diversified Index.

As we move towards the end of the first quarter of 2019, we remind investors that volatility is likely to persist in the near term with slowing global growth and a US economy that is in the late stage of its expansionary cycle. To this end, following a few months of strong returns from risk assets, we encourage investors to maintain a diversified, risk-balanced portfolio and consider increasing exposure to safe-haven fixed income.