Key Takeaways

- Rebalancing and diversification remain critical to successful portfolio construction

- This can be a time for investors to take on risk, but careful deployment and

frequent reassessment are vital - Set aside at least one quarter of spending needs in cash

- Virus Trajectory is our dominant and new key market theme; it will likely drive pricing in capital markets over the next 12-to-18 months

- Permanent Interventions remains an important key market theme as central banks and governments step in to contain the economic fallout from the global pandemic

These times are without precedent as we collectively experience the velocity and ferocity with which the new coronavirus ravages towns, cities, states and countries. This global pandemic demands unthinkable sacrifices and impossible choices.

At NEPC, above all else, we hope for the wellbeing and health of our families, friends, colleagues, clients, neighbors and those on the front lines battling the virus. We hope that our actions of today—social distancing, self-isolating and voluntary quarantining—will slow and, eventually, alter the destructive path of COVID-19. We also hope that the investment decisions our clients and we make today in the face of this tumult will set us on the course to not only preserve capital, but also grow it in the years to come, such that the losses of today pave the way for the gains of tomorrow.

To that end, we present this update of our 2020 asset allocation letter—typically an annual feature—as the investment landscape is virtually unrecognizable from just a few months ago. In a handful of weeks, the onslaught of the virus and the efforts to contain it have had a profound impact on our investment outlook. In addition, they have not only intensified and disrupted our key market themes, but also presented a new one. While the volatility ripping through markets will likely give rise to new investment opportunities, our steadfast commitment to disciplined rebalancing and diversification stands unchanged. Also unchanged: our belief that attempting to time the market is a fool’s errand; we will know the day of the bottom only in retrospect and well into a recovery. Accordingly, we believe this can be a time for investors to begin to carefully lean into risk, be it through an outright increase in targets for risky assets or by adding lower-quality credit, distressed exposure, or high-conviction active strategies. At the same time, we also recommend keeping aside cash equaling at least one quarter of spending needs.

To be sure, it is important for us to acknowledge the uncertainties related to every aspect—social, economic and political—of COVID-19. Thus, our suggestions on potential strategies and courses of action are just that: suggestions. However, we also acknowledge that investments during periods of great uncertainty are often, in retrospect, the most lucrative. These challenging times can be the best ones for investment returns over the long term, but careful placement of risk and regular reviews are critical for success.

Key Market Themes

Our outlook and market valuations for the long term are informed by our key market themes that influence asset allocation and portfolio implementation. COVID-19 has not only had a significant impact on these themes, but also become one itself. The virus has terminated our key market theme of the United States being in the Late Stage of the market cycle, as it will likely tip the US and many others into recession.

Conversely, our theme of Permanent Interventions is amplified as central banks and governments step up efforts to offset the severe economic disruption brought about by the virus.

While our other themes—China Transitions and Globalization Backlash—remain relevant, they move to the background as these two dominant ones take center stage:

- Virus Trajectory: This is a new key market theme to come out of the COVID-19 pandemic. The virus’ path is clearly the most pressing concern in the world, jeopardizing the health and wellbeing of millions, whipsawing capital markets and economies, fueling drastic monetary and fiscal measures, and compelling investors to seek the safety of cash. As cities, states and countries go through their individual cycles of infection, spread and containment of the virus, protocols for social distancing and lockdowns are being put into place, throwing into turmoil businesses while rendering millions jobless. The effectiveness (or lack of) of these restrictions will determine the pace at which they may be eased, marking the potential return to normalcy, or whatever the new normal may be – this path itself, much like the trajectory of the virus, is riddled with uncertainties.To be sure, new cases of infection will not dissipate in a matter of weeks. However, a decline in their numbers that reverses the trend of exponential increases is a strong sign that the restrictions are starting to work. Indications of an initial “bend in the curve” have already brought a measure of calm—temporary, perhaps—to markets. A potential slowdown in the spread of the virus will likely allow investors to start the process of quantifying the economic and financial fallout from COVID-19.There is also concern that lifting or loosening restrictions around movement and social interaction may fuel a second wave of the virus, forcing another spell of stringent stay-at-home measures in the fall. This theme may subside as many regions see cases wind down, but is unlikely to end until a vaccine can be effectively administered.

- Permanent Interventions: We introduced this theme at the start of the year, based on the willingness of central banks and governments to step in to bolster market sentiment. At the time, we had no idea how aggressively and quickly this theme would manifest across the world as coronavirus tore through economies. We are encouraged by the wide-ranging response—moving rates to zero, unlimited and expanded quantitative easing plan, primary dealer credit facility, money-market liquidity facility—from the Federal Reserve and its peers. These measures will inject liquidity into markets, providing stability as investors reprice risk amid the pandemic.In addition to using its handbook from the financial crisis, the Fed can also lend support to banks to stimulate economic activity; unlike 2008, when banks contributed to the crisis, they can be part of the solution this time around as they remain well capitalized. We believe the Fed’s actions will have a positive, supportive impact on markets and the economy over time. While these actions alone cannot trigger a turning point, they are part of an important set of initial actions needed to get us to one.Moving on to fiscal intervention, in the US, this has taken the form of the wide-ranging CARES Act, which is offering checks to promote spending, enhanced unemployment benefits, and loans/equity to the most challenged industries; at $2.2 trillion, it is close to 10% of GDP. Additional components will likely be tacked on as the extent of economic damage becomes clear in the coming weeks and months. Early indications show that other countries are following suit with even fiscally conservative Germany delivering a major fiscal response; France, Spain, Korea, Japan and China are also working on plans to bolster their economies during this challenging time.Even with these massive monetary and fiscal initiatives, we wonder if they will be enough to pull the US economy out of a likely recession. What we do know is that these measures are strong, positive indicators of economic support that markets have been quick to price in.

Broad Opportunities

Using these key market themes as guiding posts, we find return expectations across risky assets more attractive than just a few months ago. At the same time, we see great uncertainty and a wide range of potential outcomes. Balancing these competing forces, we suggest these potential investment opportunities and actions:

- Commit to diversification and disciplined rebalancing

- Favor areas with the strongest response against the virus and aggressive monetary and fiscal measures

- Carefully increase targets to risky assets

- Tactical investors can enhance risk posture within beta groups, particularly credit

1. Commit to diversification and disciplined rebalancing:

Investing entails going head-to-head with uncertainty. Investors earn a return in exchange for holding assets subject to a wide range of economic outcomes whose fate over time reveals a (hopefully) positive outcome. So, while risky assets offer greater promise today, there is also higher potential for an “L-shaped” recovery or even a severe depression-like environment. Should that scenario play out, the path of risky assets would appear unattractive today. Conversely, a robust recovery would mean strong prospective returns for equities and credit.

We manage some of this uncertainty by building portfolios that can withstand adverse environments. A diversified mix of assets can participate in market returns should the more favorable path play out and protect capital should more adverse scenarios emerge. Even if the diversification dampens returns, the role it plays can still be incredibly valuable.

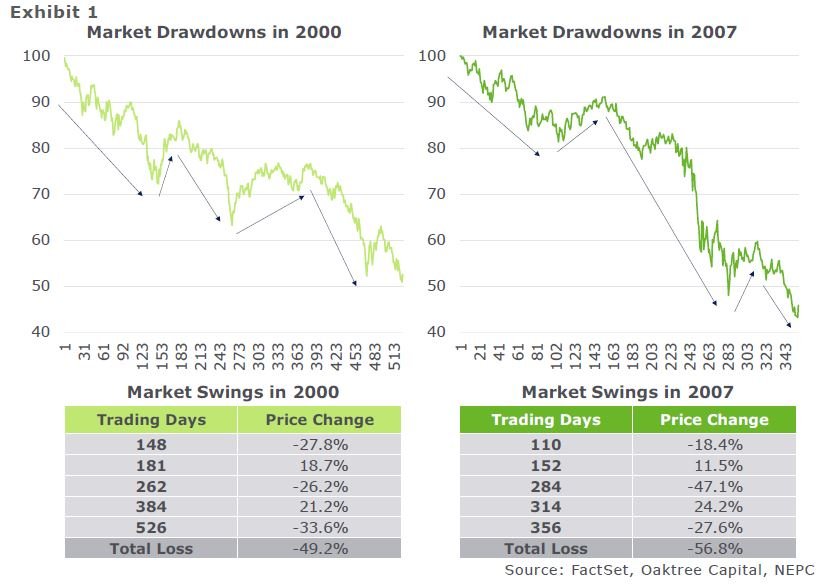

As part of that diversified approach, the next step for investors is to rebalance towards long-term targets, and to remain committed to rebalancing as markets oscillate. While markets have calmed since crashing in mid-March, it is unlikely that recovery will be just as fast. The last two major drawdowns—the tech crash and the financial crisis—show multiple periods of substantial losses and sizable upswings, only for markets to further crater (Exhibit 1). This makes rebalancing a disciplined two-way undertaking involving leaning into asset classes that have experienced losses and trimming gains as they occur, while factoring in market dynamics/liquidity and the need for cash. To that end, we recommend investors hold a quarter’s worth of cash to avoid potentially high transaction costs amid disruptions in market liquidity.

2. Favor areas with the strongest response against the virus and aggressive monetary and fiscal measures:

Countries and regions that have responded most forcefully on these fronts will likely emerge the most successful. This means the United States has a head start in an economic recovery even though it is currently roiled in the coronavirus pandemic. This also means countries like China, Korea and Taiwan that have effectively managed the outbreak are more likely to come out less scathed than other emerging economies. To be sure, the widely varying conditions in emerging countries make an overweight to emerging equities less effective. However, with a 10-year return forecast of over 10% for emerging market stocks, we continue to believe in a modest overweight; allocations to non-US developed market equities can be a funding source for an overweight to US and emerging market stocks.

3. Carefully increase targets to risky assets:

For investors comfortable with the risk profile of their asset allocation and portfolio construction, these uncertain times can offer up potentially lucrative investment opportunities. Indeed, our return expectations for equities and credit are now higher than they were at the start of 2020, with an extra 1%-to-1.5% expected annually over the next 10 years because of the recent drop in prices (Exhibit 2). Additionally, the relative attractiveness of these betas appears enhanced as falling Treasury rates erode the return prospects for safe-haven assets. Still, it is important to proceed with caution in these turbulent times as one’s confidence in forward-return expectations could be misplaced. Accordingly, investors increasing targets to risky assets should balance their exposure with safe-haven assets.

4. Tactical investors can enhance risk posture within beta groups, particularly credit:

As an alternative to adjusting risk exposure at an asset allocation level, investors can consider structure-related maneuvers within beta groups; credit allocations could be especially interesting (though these still require further study).

To that end, our Research team is currently hard at work to uncover these opportunities across the world and the capital stack. Here is a list of possible actions:

- Shifting exposure of some investment-grade fixed-income to lower-quality credit, for instance, high-yield or emerging market debt

- Carving out fixed-income allocations to credit opportunities to capitalize on areas that have taken a recent hit but carry the potential for strong returns

- Committing to new areas of opportunity like distressed investments

- Pivoting hedged equity exposure to higher beta exposure

- Investigating high-conviction, capacity-constrained strategies for potential new commitments

We expect the coming months will bring some of these opportunities into sharp relief as we begin to grasp what lies ahead; some will be compelling while others will be passed up. We look forward to working through them and communicating ideas to our clients as we build conviction.

Conclusion

The battle between the uncertainties and dangers laid bare by COVID-19 and the defensive measures adopted by governments and central banks are likely to dominate markets in the weeks and months ahead. Making sense of this environment and assessing potential outcomes are a challenging exercise, making it even more important to proceed with caution. As our key market themes of Virus Trajectory and Permanent Interventions dominate market pricing, we are presented with an impossibly wide range of outcomes. To that we say: stay diversified, have the courage to rebalance into risky assets, and consider opportunities as they emerge. This will help position investors for long-term success.