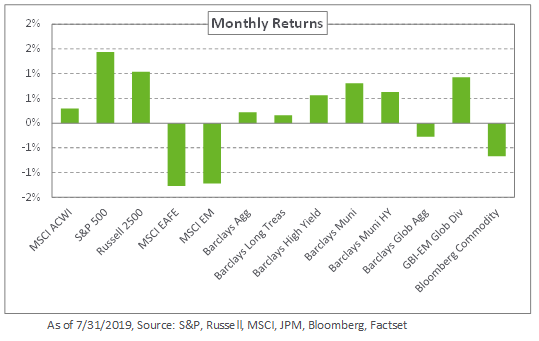

Most asset classes recorded modest returns in July on the heels of stellar performance in the first half of the year. Domestic equities outperformed with gains of 1.4%—bringing year-to-date returns to 20.2%—as the S&P 500 Index hit a record high fueled by expectations of lower rates in the United States. Internationally, a strong dollar detracted from non-US equities with the MSCI EAFE and MSCI Emerging Markets indexes posting declines of 1.3% and 1.2%, respectively.

As widely anticipated, the Federal Reserve lowered rates by 25 basis points – marking the first rate cut by the central bank since 2008. In addition, the European Central Bank indicated a more accommodative stance as the region’s outlook for growth continues to deteriorate in response to trade and political noise. Despite these changes, global rates were relatively flat for the month with the 10-year US yield increasing two basis points and the 10-year German yield declining 10 basis points. In emerging markets, local- and dollar-denominated debt rallied on expectations of lower rates in the US. The JPM EMBI Global diversified and JPM GBI-EM Global Diversified indexes increased 1.2% and 0.9%, respectively, last month.

In real assets, oil experienced another volatile month amid escalating geopolitical tensions. Spot WTI Crude Oil ended the month slightly higher – adding 0.5% in July for year-to-date gains of 29.6%.

Though renewed central bank accommodation provided a temporary boon to markets, escalating global trade rhetoric and slowing growth temper our excitement for risk assets. To this end, we encourage rebalancing overall equity exposure and reducing return-seeking credit.