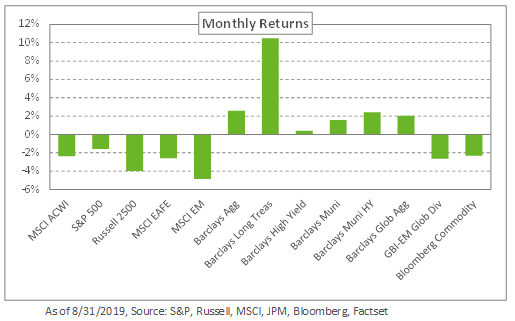

Equity markets lagged in August as trade tensions between the US and China resurfaced and investors fretted over slowing global economic growth. The S&P 500 Index declined 1.6% last month as the US manufacturing sector grew at its slowest pace since 2009, according to Markit’s Manufacturing Purchasing Managers’ Index. The MSCI EAFE Index lost 2.6%, while the MSCI Emerging Market Index fell 4.9% as currency weakness in China put a damper on the rest of the EM Index.

Global bond yields continued to decline as demand for safe-haven assets rose. In the US, 30- and 10-year Treasury yields dropped 57 and 52 basis points, respectively, causing the yield curve to fully invert. As a result, the Barclays US Long Treasury Index shot up 10.5%, its fourth-highest monthly return since inception in 1973. In emerging markets, a stronger US dollar caused hard-currency bonds to outperform local-currency debt, resulting in a 0.7% gain in the JPM EMBI Global Diversified Index and a loss of 2.6% in the JPM GBI-EM Global Diversified Index.

Meanwhile, in real assets, gold prices got a shot in the arm, rising 7.5% in August, amid concerns around global growth and a lower-yield environment. Additionally, spot WTI crude oil fell 5.9% to $55.06 per barrel but remains up 21.9% for the year.

With slowing global growth and the United States in the late stage of its economic cycle, we maintain our recommendations to rebalance equity exposure, reduce return-seeking credit, and consider shorter-duration maturities within safe-haven fixed income.