Rated note feeder structures are becoming increasingly common across private market strategies offered to insurance companies.

These structures can meaningfully improve capital treatment by allowing a portion of a private market investment to be held on Schedule D rather than Schedule BA1. As a result, we have observed that they are often viewed as a compelling solution for insurers seeking to expand their private market allocations while managing capital charges. At NEPC, we believe rated note feeders should generally be viewed as a secondary consideration rather than a prerequisite; the starting point should always be identifying the most appropriate private market strategy based on its underlying investment merits. Only after that determination is made should insurers consider a rated note feeder (if available) and whether it adds value given the specific structure, cost, and complexity involved.

To be sure, our views primarily reflect the experience of insurance companies—well-capitalized organizations with relatively modest private market allocations—we typically advise, but we recognize that rated note feeders may play a more central role for other segments of the insurance industry. Larger insurers with more complex capital frameworks may view rated note feeders as a vital component of balance sheet management, where even incremental improvements in capital efficiency can be meaningful when scaled. As a result, our intention is not to be universally prescriptive, but rather to lay out our process around how we evaluate rated note feeders within the context of our client base and investment philosophy.

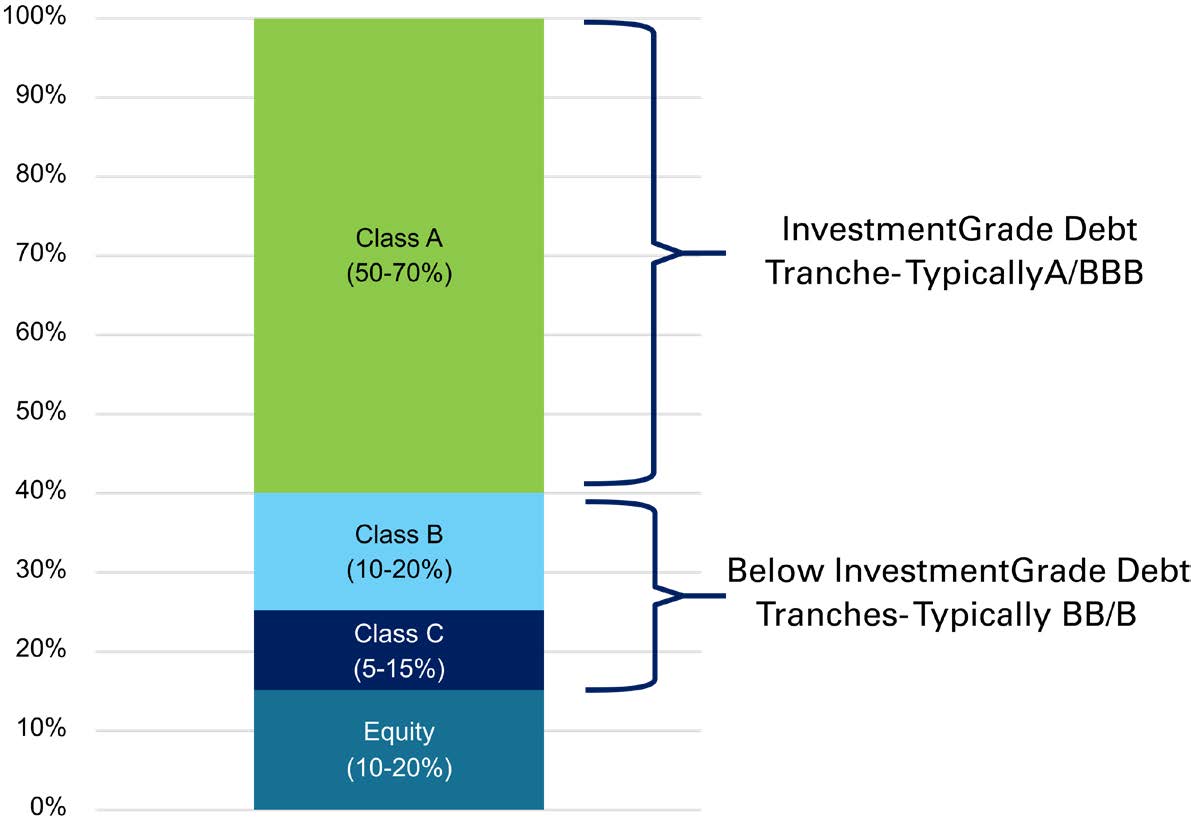

Illustrative Rated Note Structure

NEPC Internal Example provided for illustrative purposes only. This graph is not representative of any actual client portfolio investment.

Source: NAIC, based on latest published RBC framework as of the date of this publication.

Strategy, First…Structure, Second

Our philosophy is simple: start with identifying a strong private market strategy, and then assess the structure. We do not believe the availability of a rated note feeder should drive strategy selection. Fur-thermore, while rated feeders are becoming increasingly common, they still aren’t offered for every (or even most) private market funds.

We find that insurance clients that use a consultant are well capitalized and, for many, private market exposure is typically modest – often less than 10% of total portfolio assets. Against this backdrop, ab-sorbing a higher capital charge by investing directly into a traditional Limited Partner (“LP”) vehicle is rarely punitive, particularly if the strategy is otherwise attractive.

That said, there are instances where rated note feeders can play a role. In cases where two or more strat-egies are otherwise comparable across return expectations, risk profile, manager quality, and fit within the broader portfolio, the availability of a well-structured rated note feeder can serve as a reasonable tie-breaker. In those situations, improved capital treatment may justify favoring one strategy over another.

Not All Rated Note Feeders are Created Equal

While rated note feeders can be helpful, they introduce an added layer of structuring that requires scrutiny. We have observed significant variation across rated feeders, and in some cases, the plain vanilla LP vehicle may be preferable despite the potential capital benefit of the rated structure.

At NEPC, we prefer simply and elegantly constructed rated note feeders; we tend to be more cautious as complexity increases or if structuring is too aggressive relative to the quality of the underlying collateral. These are the points we keep in mind while evaluating different rated note feeders:

1. Tranches

One of the first structural features we examine is the number of tranches in the rated note. Our preference is for fewer tranches rather than more, ideally consisting of:

- Two-to-three debt tranches (typically a mix of investment-grade and below investment-grade ratings), and

- A residual (equity) tranche

While we can get comfortable with structures that include additional tranches, simplicity matters. One practical consideration is cost: in some cases, insurance investors are required to pay for each tranche to be independently priced on a quarterly basis2. As the number of tranches increases, so do the valuation costs.

Beyond cost, we have found a simpler capital structure tends to be easier to understand, monitor, and explain internally, which is particularly important for less liquid long-term investments.

2. Alignment of Interest

Another critical consideration is who owns which part of the capital structure. From an alignment-of-interests perspective, we prefer rated note feeders where all investors receive a vertical strip of the structure, meaning each investor has the exact same exposure across debt and equity tranches in proportion to their investment.

We become more cautious when different tranches are sold to different investor types (for example, one group holding only the debt tranches, and another holding only the equity ones). In these situations, questions arise:

- Is the asset manager optimizing the strategy for debt holders or equity holders?

- Are there implicit incentives to prioritize the preferences of certain investor groups?

- Does this create misalignment in how risk is taken and managed?

In addition, we have seen cases where investors have the option of blending different combinations of tranches to manufacture a desired return outcome. For example, ratcheting up the equity exposure to boost returns or increasing debt exposure to dampen volatility. From our perspective, this begins to feel like an exercise in financial engineering rather than a pure investment decision.

We recognize that some insurers view this flexibility differently, using tranche selection as a way to align a strategy with internal capital constraints rather than alter the underlying economics. While this perspective may be reasonable in certain contexts, our preference remains to evaluate strategies based on their inherent return and risk characteristics rather than post investment financial engineering.

3. Underlying Economic Interest

We also pay close attention to the type of strategy being placed into a rated note feeder. Certain strategies, such as direct lending, are often a natural fit for rated structures given their contractual cash flows and debt-oriented risk profile.

Where we become more cautious is when the underlying strategy begins to look less like debt and more like private equity yet still benefits from partial bond treatment through a rated note feeder. We have seen examples where strategies with more meaningful equity risk are placed into rated feeders simply because the underlying investments generate recurring cash flows.

At NEPC, we are looking for the economic risk of the strategy to closely mirror the rated structure. Our view is that rated note feeders should be used to obtain improved capital treatment for fundamentally debt-like strategies, not as a means to repackage higher-risk equity strategies as bond investments.

4. Anchor Investors

We place significant weight on whether there is a committed anchor investor. We have seen instances where managers announce plans for a rated feeder that ultimately never materializes due to insufficient scale. Given the cost and effort involved in establishing these structures, having one or more anchor investors can materially improve confidence that the feeder will actually be launched.

5. Ratings

We prefer rated note feeders ranked by one of the so-called Big Three ratings agencies—Fitch Ratings, S&P Global Ratings, or Moody’s Ratings—as a starting point. Kroll (KBRA) is another ratings agency that commonly rates structured notes and is viewed as credible by many insurance investors. Beyond these agencies, we will consider other providers, though doing so typically warrants heightened scrutiny.

Conclusion

We approach rated note feeders from a position of open-minded skepticism. We are supportive of their use when they are thoughtfully designed, well-aligned, and appropriately paired with the underlying investment strategy. However, we do not view them as a requirement for most insurance portfolios, particularly those that are well capitalized and maintain relatively modest private market allocations.

As always, every insurance company will have its own set of considerations, constraints, and priorities. Our role is to help clients evaluate both the strategy and the structure, ensuring that decisions are driven by long-term investment outcomes rather than capital efficiency alone.

To learn more about private market investing or how rated note feeder structures may (or may not) fit within your portfolio, please contact your NEPC consultant.

1Schedule BA assets carry a higher capital charge relative to Schedule D assets. A traditional LP investment without a rated note structure typically receives full Schedule BA capital treatment (~30% capital charge for P&C insurers and ~40%–45% capital charge for life insurers), whereas a rated note feeder can significantly reduce the blended charge closer to 10-20% depending on the structure and insurer type.

2In some cases, the asset manager will pay for the cost to price the tranches each.