This is the fourth of a four-piece series under the heading, “Investing in Private Markets: Best Practices for Family Offices.” In the series, we focus on the unique challenges of investing in private markets and how family offices can most effectively address them.

Private markets can be complex; to be successful in this space, family offices can benefit greatly from sophisticated tools, dedicated investment teams, and an advanced operational structure. We believe this is particularly true in three key areas:

- Manager selection

- Governance structures

- Performance evaluation

Family offices that are just beginning to engage in private market investing can learn a lot from more experienced family offices and institutions about how to best set up a private markets program. But even family offices who have a long history in the private markets need to constantly update their procedures to take advantage of evolving technology and consultant relationships. That’s especially true today, as family offices may feel ongoing pressure from their principals to add more professional capabilities.

Why Manager Selection is Uniquely Consequential

In public markets, the difference between a skilled and an average manager is meaningful but bounded. Beta exposure does much of the work, and in our experience, the dispersion between top- and bottom-quartile managers is relatively modest. In private markets, however, outcomes are largely driven by manager skill – and the skillset goes well beyond good financial analysis.

To be successful in private markets, managers need to have proprietary sourcing networks that give them access to high-quality investment opportunities. As owners, they need the execution capabilities that help the businesses they invest in build value, guiding them toward profitable exits. The spread between top-and bottom-quartile private markets managers is dramatically wider than in public markets.

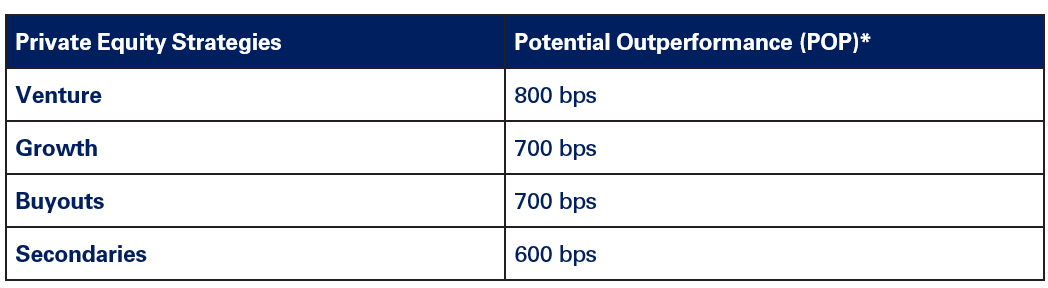

NEPC maintains a measure called POP – potential outperformance due to strong manager selection. This measure captures the spread between the 25th percentile manager and the 50th percentile manager, as a way of demonstrating the excess return above median attributable to strong manager selection. POP data consistently shows that manager selection is a key driver of return variation across portfolios.

This reality carries an important implication: if a family office cannot access top-tier managers, it is generally better off not investing in private markets at all. Without access to those managers, the illiquidity and complexity of private markets are difficult to justify.

Manager Selection

Best Practice #1: Use Consultants to Expand Manager Access

Manager access is a common challenge, because the best managers are frequently capacity-constrained, or may be closed to new investors, or may prefer investors with whom they have long-standing relationships. This is one of the most tangible benefits of working with an established investment consultant: consultants can bring relationship capital and institutional standing that open doors which would otherwise remain closed.

Consultants can also perform manager selection due diligence using a broad and comparative lens. Their experience identifying appropriate managers for a wide range of investors can help ensure better outcomes for family offices that have moved into this space.

Best Practice #2: Don’t Chase Performance

Chasing standout performance can be as problematic in private markets as in public. A strong recent track record is an unreliable guide to future results in private markets, where vintage timing, market conditions, and portfolio maturation all influence reported returns. In our experience, the more durable indicators of manager quality are the consistency of the investment process, the depth and proprietary nature of the sourcing network, and the stability and alignment of the team.

Best Practice #3: Perform Due Diligence Every Time

One highly valuable discipline in the private space is to underwrite a manager at each new fund commitment, rather than simply re-upping on the basis of familiarity. Markets evolve, teams change, and strategies drift. Ongoing monitoring between commitments ensures that the family’s private markets portfolio reflects deliberate, current judgment rather than accumulated inertia.

Beyond Manager Selection: Governance

Best Practice #3: Detailed Liquidity Forecasting

Although manager selection is often the primary differentiator of private market outcomes, the impact of governance can’t be ignored. Governance guidelines are an essential tool to help family offices and their principals make consistent, disciplined decisions in a marketplace that can be hard to predict. Again, investment consultants can be tapped to identify and compare governance tools and recommend options.

Best Practice #4: Expand the Investment Policy Statement

Investing in private markets requires a governance framework that is meaningfully more sophisticated than what most families have in place for public market portfolios. Families should ensure their investment policy statement (IPS) explicitly lays out policies and guidelines related to their private markets holdings. These might include:

• Articulating goals and objectives specific to private market ownership

• Liquidity requirements, including data or other criteria that will be used when making liquidity decisions

• Portfolio details, such as position sizing parameters and asset-allocation guardrails

• The specific criteria by which new commitments will be evaluated

Without that foundation, it becomes easy for short-term concerns to overtake long-term planning and discipline.

Best Practice #5: Ensure Clear Decision-Making Authority

Family offices need to make sure that the right voices – whether internally, through a trusted advisor, or both – are performing oversight and contributing to private market decisions. Often, the right people to make those decisions or contribute to the discussion differ from those involved in public markets decisions. All stakeholders need to recognize that investing in private markets may very likely require a different decision-making process.

Evaluating Success

Best Practice #6: Use the Right Performance Evaluation Tools

Measuring performance in private markets requires a different toolkit than public markets. Standard metrics include:

• internal rate of return (IRR),

• distributed to paid-in capital (DPI)

• total value to paid-in capital (TVPI)

• multiple on invested capital (MOIC)

• public market equivalent (PME)

Each of these measures illuminate different aspects of a fund’s performance, and fluency with all of them is necessary to form a complete picture. Note also that performance should be evaluated in relation to vintage year and strategy.

Best Practice #7: Recognize the Limitations of Benchmarks

In our experience, benchmarking isn’t as helpful in private markets as in public. Private markets indices are subject to reporting lags, survivorship bias, and valuation smoothing that make direct comparisons imprecise. Benchmarks can provide useful context, but they are not a good proxy for success in a private markets program.

Best Practice #8: Look at the Big Picture

Ultimately, we believe the most important assessment in private markets is determining whether progress is being made toward long-term goals. Private markets portfolios are built over decades, and short-term valuations often don’t provide adequate insight into the success of the portfolio’s underlying holdings.

But there are ways other than performance to determine if a private markets program is effective. Is the family gaining access to high-quality opportunities? Are they building strong relationships with top-tier managers? In our experience, these program qualities are highly correlated with success and provide valuable feedback to the family office.

Building a Program That Endures

Best Practice #6: Use the Right Performance Evaluation Tools

Enhancing your evaluation capabilities and governance toolkit may not be the first thing a family office thinks of in its private markets program. In this piece, we have outlined why it is an essential component to success and how family offices can level up their game. Other pieces in this series address further best practices, including portfolio construction and liquidity.

A well-designed private markets program is a powerful tool for family offices, but that power comes with complexity, and complexity rewards thoughtful design and consistent execution. The families who benefit most from private markets are those who approach it with patience, discipline, and a trusted partner like NEPC who can provide both the framework and the ongoing guidance to navigate it well.

Sources: As of Dec/31/2025. Sources: NEPC, World Federation of Exchanges database, World Federation of Exchanges (WFE) https://data.worldbank.org/indicator/CM.MKT.LDOM.NOend=2025&locations=US&start=1978. *Potential Out-Performance (POP): upside potential from strong manager selection (25th percentile to 50th percentile spread). POP is for illustrative purposes only and no client has achieved these results.