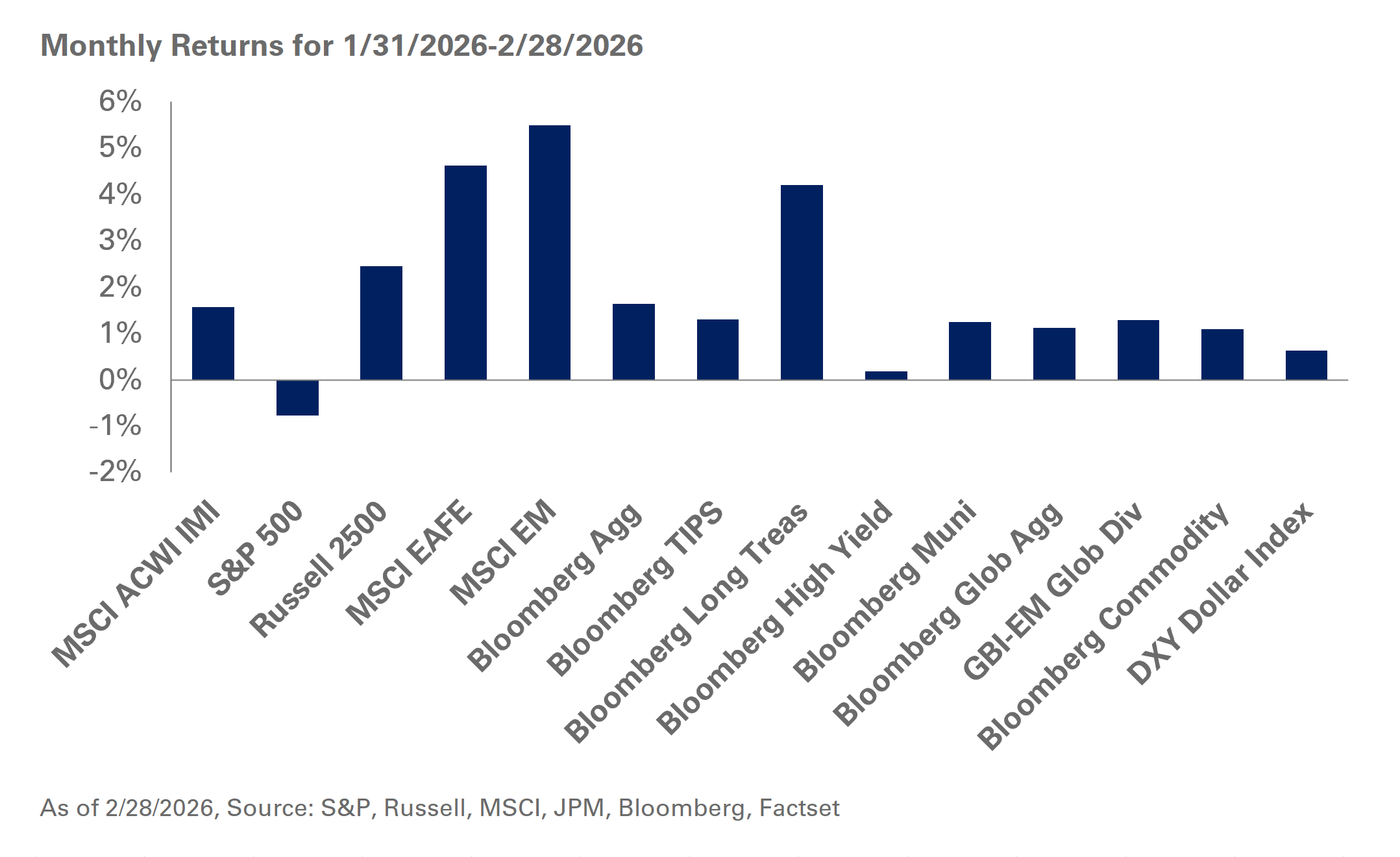

Investors shied away from U.S. mega-cap technology stocks in February as the S&P 500 fell 0.9%; meanwhile U.S. value, small-cap equities and international stocks posted gains, reflecting a preference for breadth over concentration. In addition, investors are looking beyond the infrastructure buildout of AI to assess its disruptive effects on other established sectors in the technology space. While many of the top 10 names of the S&P 500 delivered strong earnings in February, the market reaction was muted as the broader index outperformed relative to the top 10 names.

On the economic front, data released in February painted a constructive but complicated picture. January CPI decelerated to 2.5% year-over-year while January core PPI accelerated to 0.8% month-over-month, signaling that producer inflation pressures are edging up above consensus. Fourth quarter real GDP came in at 1.4% as the government shutdown and exports detracted from robust consumer spending and business investment.

In fixed-income markets, the Bloomberg U.S. Aggregate Bond Index was in the black, benefiting from a rally in rates. Yields on 10-year Treasuries reached 4.04%—their lowest level in months—amid demand for safe-haven securities. Credit spreads widened in February and leverage loans lagged due to weakening sentiment.

Meanwhile, two events injected significant uncertainty into the macro economic outlook. First, the Supreme Court ruled 6–3 that tariffs imposed under IEEPA were unconstitutional; the ruling has immediate implications for trade policy as revenues collected from the tariffs are now potentially subject to refunds. The administration responded by swiftly reimposing a 10% baseline tariff under Section 122 of the Trade Act of 1974.

Geopolitical tensions intensified on February 28 with coordinated U.S. and Israel airstrikes on Iran. The price of oil moved sharply higher as capital markets around the world responded. We believe Iran has a limited impact on the global economy and investor portfolios with oil exports estimated at less than 2 million barrels per day, and the bulk of its exports delivered unofficially to China. There appears to be sufficient spare capacity of oil that can be sourced globally from the Middle East and other parts of the world. While oil and natural gas prices may reflect an elevated geopolitical risk, we believe the bigger uncertainty for capital markets is the severity of Iran’s response. Markets may respond with greater volatility in the event of a significant attack on Middle Eastern oil facilities or a blockade of the Strait of Hormuz. We encourage investors to be open to rebalancing opportunities in the event of a temporary drawdown across global equities.

We also recommend investors remain disciplined and stick to long-term strategic asset allocation targets. We advocate maintaining exposure to equities and seeking opportunities to rebalance across market segments should stocks materially under- or out-perform. Within equity portfolios, we suggest balancing exposure of the earnings power from the largest S&P 500 names with value and quality companies across the globe. However, we advise being mindful of portfolio equity positions and monitoring outsized tracking error levels associated with the top 10 index names of ACWI IMI. Furthermore, we prefer investors hold high-quality, liquid assets, are underweight non investment grade public debt, and maintain appropriate safe-haven fixed income exposure for liquidity and downside protection.

Data as of 2/28/26, Sources: Factset;

U.S. Energy Information Administration (EIA), “World Oil Transit Chokepoints” (Accessed 2/28/2026) Retrieved from https://www.

eia.gov/international/analysis/special-topics/World_Oil_Transit_Chokepoints