Not all value stocks are created equal.

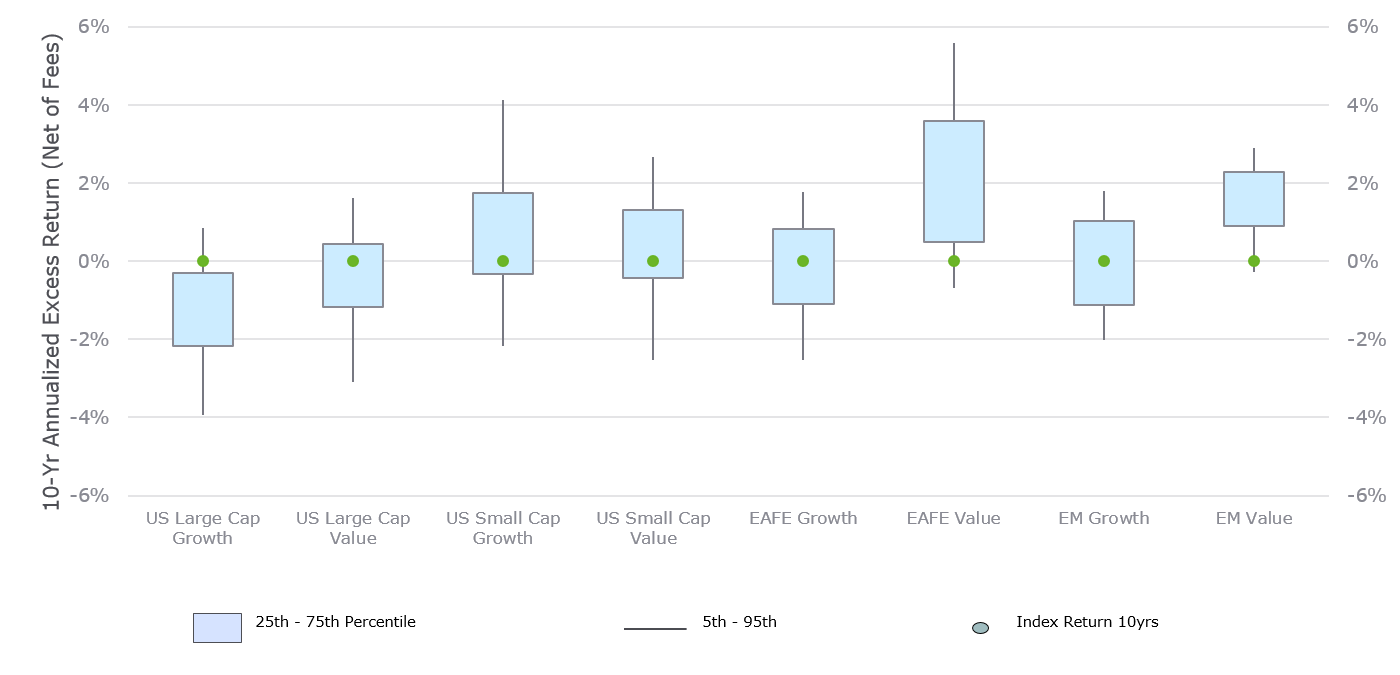

Nuances of their business models and patterns of capital expenditure have contributed to lackluster returns. Performance has been further exacerbated by COVID-19, which has fueled a seismic shift in the consumption of goods and services in favor of growth stocks. For investors frustrated with the continuing underperformance of value stocks relative to growth equities, the answer is to not give up on value equities entirely. The key: an active investment strategy with the capability to extract alpha from this space, especially since our analyses show that in the last 10 years, active value managers can be more adept at outperforming passive benchmarks than their growth counterparts (Exhibit 1).

Exhibit 1: Excess Equity Returns Over a Trailing 10-Year Period

Source: eVestment (data as of 12/31/2019; net of fees)

At NEPC, we believe value equities have a role to play in portfolio diversification and balance. To that end, we recommend investors take a closer look at their value holdings and the underlying investment strategies to better understand past performance during different economic environments. When evaluating active strategies, we think there is greater opportunity for excess returns in asset classes that have a wide dispersion of returns between investment managers. We also advocate areas where active management has historically outperformed the passive index benchmark, net of fees. Once you find these pockets of opportunity, look for characteristics of skillful managers: examine past performance and the factors the manager has exploited – attempt to parse market factors from unique insights, and further parse unique insights from random luck. Additionally, one should evaluate the abilities of the investment team to manage the portfolio effectively, assess the team’s skill at adapting to different market conditions, and, finally, understand the benchmark that will be used to evaluate active management’s performance.

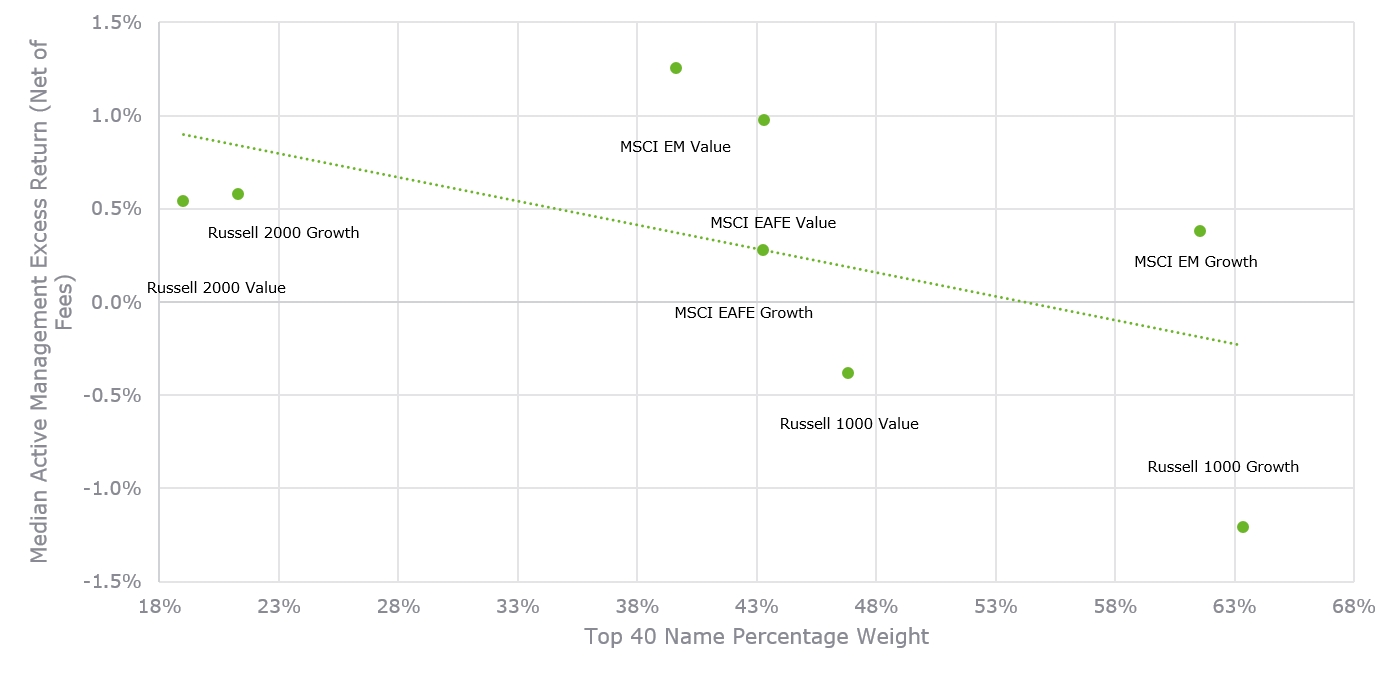

To be sure, active managers have received flack for their failure to outperform their benchmarks, with 83%-to-95% of them underperforming over a trailing 15-year period (net of fees but excluding loads), according to data from S&P Indices Versus Active, commonly known as SPIVA. The struggles of active management may be attributed to a host of factors, ranging from the rise of exchange-traded funds and passive options, to increased competition and the top-heaviness of benchmark indexes. NEPC analyses around benchmark concentration show that when a few individual names account for most of the performance of a benchmark—for instance, Microsoft, Apple, Amazon, Facebook, and Alphabet make up nearly 33% of the Russell 1000 Growth Index—it is harder for managers to outperform because of the outsized impact on performance exerted by these top-heavy names (Exhibit 2).

Exhibit 2: Index Concentration versus Median Excess Returns Over a Trailing 10-Year Period

Source: FactSet, eVestment (data as of 12/31/2019; net of fees)

To that end, it is important to not only reevaluate active management’s role across the investment spectrum, but also pick the appropriate benchmark to ensure it truly represents the current investment options for the active manager. It is also pertinent to point out that the underperformance of active strategies is likely exaggerated as the data from SPIVA encompasses all fund options, including retail mutual funds which typically charge higher fees. These relatively higher fees can distort results by understating returns; institutional investors can bolster performance with their access to lower-fee options like separate accounts, institutional class mutual funds, or commingled funds.

NEPC takes a long-term approach to evaluating active management in public markets. As we consider exposure to value and growth in diversified equity allocations, we acknowledge that the tremendous run of growth strategies relative to value can make investors question whether value strategies will make a comeback. To the doubters, we say that we take comfort that value managers have, in general, delivered alpha to their investors. Further, we have seen factors, like value and growth, move in long cycles; at some point, we expect this cycle will turn, and value will outperform again, especially given the degree of its underperformance and the apparent attractiveness of value stocks relative to growth equities. We believe continued balance between value and growth, and active implementation in alpha-rich segments, for instance, small cap and global equities, will improve investors’ chances of meeting and exceeding long-term return objectives in their equity allocations.

Capital Allocation

Decisions around capital allocation, for instance, debt issuance, dividend payouts, stock buybacks, investing in research and development, expenditures and mergers and acquisitions, could contribute to the return differential between value and growth stocks. In the current environment, companies with lower leverage or a cash chest—an attribute shared by many growth companies—have proved to be more resilient, while companies with relatively high debt levels—typical of value companies—have been punished. The recession has put a damper on dividend payouts, a mainstay of value companies such as banks, as new regulations compel financial institutions to sock away funds for a potentially rainy day. Similarly, many companies have also suspended stock buyback programs which may aid in the potential recovery of value, giving investors an opportunity to snap up relatively underpriced value stocks. Investors should assess companies based on their respective capital allocation philosophies and set expectations accordingly.

Business Models

The ongoing structural shift in personal consumption patterns towards services and away from goods in the United States has been accelerated by the pandemic. In the last 10 years, traditional asset-heavy sectors such as energy and materials halved their index weights in the US and beyond, yielding proportions to information technology, communication services, consumer discretionary and healthcare. The disruption of new business models and technologies presents fundamental headwinds to traditional value. Market leaders and former industry titans who fail to innovate and adapt face the risk of obsolescence, which means a broadening of value traps for investors. While evaluating active strategies, seek out managers incorporating these complexities in their analyses.