WHEN IT COMES TO SPACs, YOU HAVE TO LOOK BEFORE YOU LEAP

An abundance of issuance and the unpredictable performance of special purpose acquisition companies (SPACs) should give investors pause. However, these investment structures remain an effective means of exit for private equity companies, while offering investors a chance to gain exposure to young, potentially promising companies. With a frothy pace of issuance, SPACs are appearing in portfolios across a wide spectrum of asset classes, including hedge funds, private equity, and traditional bond funds. Additionally, a throng of SPAC-dedicated strategies and exchange-traded funds have launched in the past year. Their proliferation makes it vital for investors to learn how to approach them.

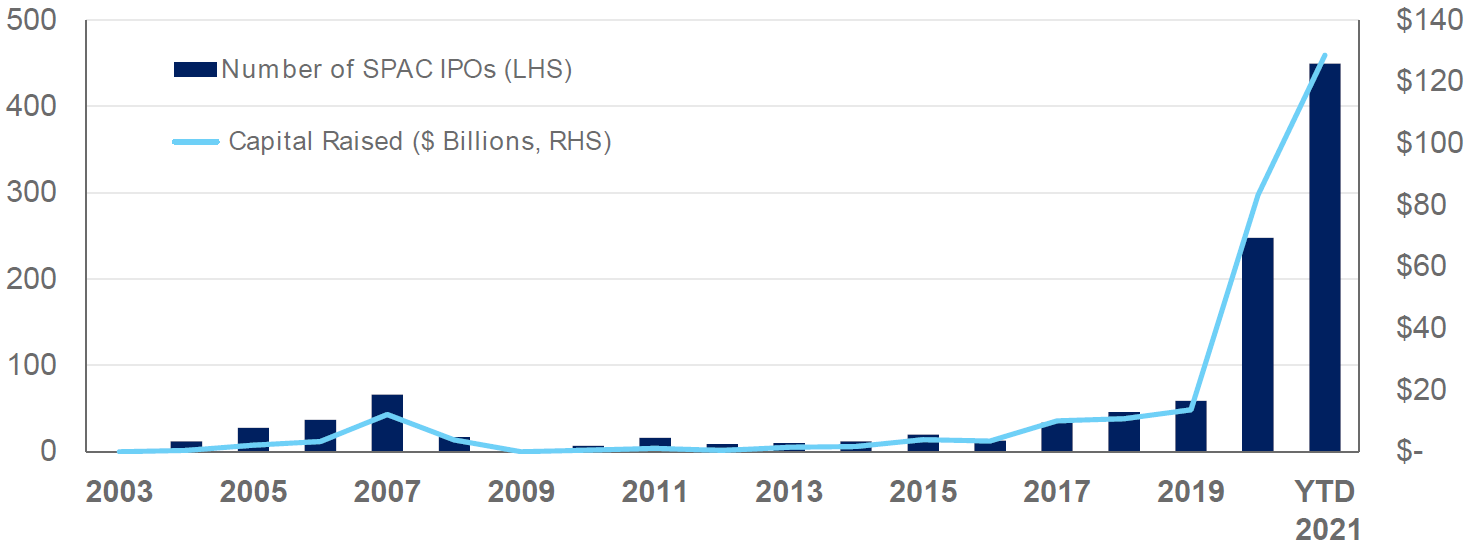

SPACs exploded back onto the capital markets scene last year (Exhibit 1), setting records for issuance while accounting for approximately half of all initial public offerings. So far this year, issuance has already exceeded that of 2020; through the third quarter, issuance of SPACs totaled $129 billion through 450 offerings, up from $83 billion through 248 offerings in 2020, according to data from SPACInsider. And although new SPAC formation dropped significantly after the first quarter, the subsequent two quarters were the third- and fourth-largest quarters on record in terms of number of SPACs raised in history. The resurgence in SPACs can potentially be traced to a number of factors: a handful of early successes, including space tourism start-up Virgin Galactic Holdings Inc. and sports-betting operator DraftKings Inc., excess liquidity driven by unprecedented and extraordinary levels of fiscal and monetary support—outlined in NEPC’s key market theme of permanent interventions—and rock bottom interest rates that are fueling demand for higher-yielding growth assets.

EXHIBIT 1: SPAC ISSUANCE BY CALENDAR YEAR:

Attractive deal economics are also a draw. Sponsors of SPACs—investor groups that launch the vehicle and then seek a private company to take public—typically receive 20% to 25% of a deal’s value in equity while putting up only a small amount of risk capital to get the vehicle off the ground. Sponsors usually have two years to close a deal or pay back the SPAC’s investors and forfeit the risk capital. Typical sponsors include well-known private equity funds, hedge fund managers, public-market investors and business executives; the popularity of SPACs and their lucrative terms have attracted the likes of Shaquille O’Neal as well.

Demand for SPACs pushed the average premium to a net asset value above 25% and average yield to maturity to -3.4% in mid-February, according to data from Accelerate Financial Technologies, before the threat of rising interest rates put a dent to growth assets in March. Since, investor ardor has cooled. As of September 24, the average SPAC price had dipped to a -1.8% discount to NAV. While finding quality companies to hold for the longer term may be the goal of some investors, other investors may have different objectives. Fixed-income and absolute return-oriented investors, for example, tend to be shorter-term SPAC buyers, owning the securities for yield while enjoying the downside protection provided by the cash held in trust while the sponsor seeks a combination. Others will wait until a SPAC’s shares separate into units and warrants, selling the units ostensibly above the $10 issue price while holding the warrants for additional upside upon a merger announcement.

To be sure, not all SPACs are created equal. Post-merger public-market performance has been all over the map. While median performance of post-merger companies since 2019 has been positive, the dispersion of returns has been material. As is often the case with speculative areas of the market that have drawn significant amounts of new capital and catalyzed new fund and product launches, investors should proceed with caution. Simple supply and demand dynamics should raise eyebrows – as of September 24, there were 580 active SPACs outstanding with a total market cap of $186 billion; 453 of those were actively seeking a deal, with an additional 306 S-1 filings waiting to IPO, according to data from Accelerate. Given the vast dry powder chasing a potentially limited universe of quality targets, there will invariably be duds underperforming the broader market or outright losing money alongside companies that go on to perform well in the public market. There is no doubt that the SPAC structure offers an asymmetric upside return profile given the downside protection of the cash in trust. However, this is contingent on the ability of an investor to participate in a SPAC’s IPO. The fervor with which the market has bid up pre-deal SPACs underscores their speculative nature, at least in the current market environment. Their volatility and downside potential have been on display, with the SPAK ETF falling 24% in a matter of 20 days from mid-February to early March.

At NEPC, we advise against buying a basket of SPACs or another form of SPAC beta. Instead, investors should rely on the ability of their investment managers to participate prudently in the SPAC universe. For example, if a manager in your portfolio sponsors a SPAC, you might question whether the manager has the resources, ability and experience to launch the vehicle. You also want to examine the manager’s track record of structuring and executing private investments, and whether there is a deal pipeline robust enough to support a SPAC sponsorship. If these questions can be answered in the affirmative, a SPAC may provide an attractive investment opportunity for both the manager and limited partners.

Please contact your NEPC consultant if you have questions on these investment structures or are looking to evaluate an opportunity in this space.