Investors today are getting less money than expected from their private market investment funds.

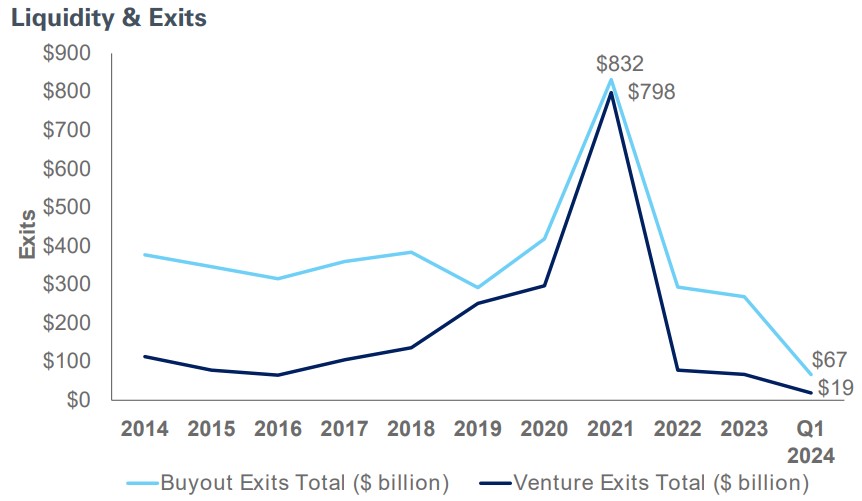

As higher interest rates and the increased cost of financing hobble exits from buyout, venture capital and real estate strategies, the cash coming back to investors is down 70% or more from its peak in 2021, according to PitchBook1. This can be challenging for limited partners in these funds, particularly because general partners continue to call capital while distributions have slowed.

At NEPC, we maintain a watchful eye on private markets and have offered our outlook on the marketplace to Bloomberg, Institutional Investor and Nasdaq. We believe these market dynamics offer promising opportunities. Historically, environments like today—characterized by scarce liquidity and high uncertainty—have yielded strong returns.

Private market investors have ramped up allocations meaningfully over the last 15 years as an era of low interest rates incentivized riskier investments to achieve required rates of return. Deal activity was robust, peaking in 20211. Today, higher interest rates have put a wrench in the system, hampering deal activity within buyout, venture capital and real estate strategies in the following ways:

Buyouts:

The higher cost of financing is straining the ability of GPs to sell their portfolio companies. The cost of debt used to be 4%-to-5% in a lower rate environment, but buyout debt—typically tied to a floating rate—is currently closer to 9%. This ratchets up interest expense, eating into the profitability and cash flow of underlying portfolio companies. This, in turn, holds back valuations at exit. Buyers and sellers are struggling to agree on a transaction price, and while the IPO market is open, it is not being broadly used for exits.

Venture:

Valuations peaked in 2021-20221, and one venture capital investor we spoke with described this time as being a frog in boiling water. Typically, venture funds hold on to valuations determined at the last round of financing, so marks of many portfolio companies are still high and will likely decline when the company raises its next round of financing. Venture has always been a long-term investment with lower liquidity and longer lifecycles because building companies from the ground up usually takes 10-to-12 years.

That said, the current pace of exits and venture liquidity is slower than normal. To be sure, venture LPs have seen liquidity from their venture portfolios in the last year, but that was mainly from venture funds selling public positions still held in their funds after exit (some funds had up to one-third of their fund in public equities). This pulled forward liquidity in the system and NEPC is closely watching what the next two-to-five years will look like. (Note: AI was 40% of funding of global total capital raised in May and commanding high valuations, according to data from Crunchbase through Axios Pro Rata.)

Private Debt:

Deal activity continues, and these strategies are cash flowing and have shorter fund lives than buyouts or venture. For now, private debt is holding firm and providing liquidity to investors. Still, it remains to be seen how long companies can pay 12%-to-14% in interest against their borrowings. This dynamic makes manager selection key in today’s environment.

Real Estate:

Higher interest rates increase the burden on cash flows coming from properties. Real estate valuations lag, taking longer to mark down because they are based, in large part, on transaction figures and, when there are limited transactions, there are limited comps.

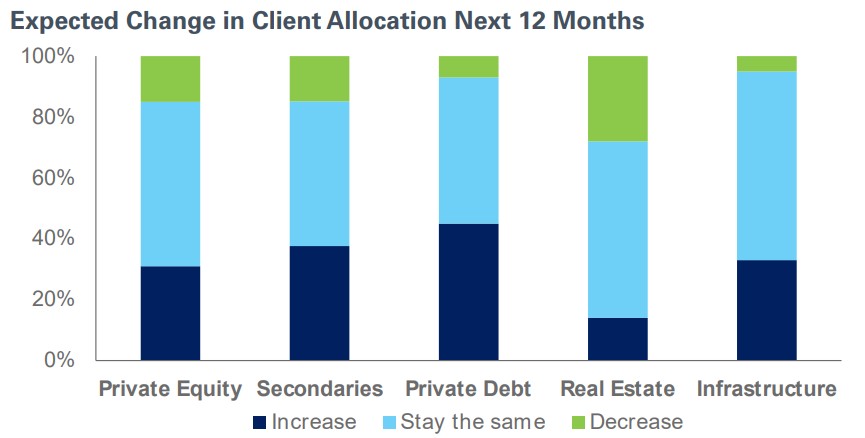

At NEPC, we believe that despite these market dynamics or, perhaps, because of them, there appear to be abundant opportunities for buyers (and lenders). History has repeatedly shown that in environments like today, vintage year returns can be quite strong. We are not alone in our belief: A June 2024 study by Coller Capital2 shows that over 80% of investors plan to hold or increase their exposure to private market investments.

Our investment team sees promise in the following parts of private markets:

- Buyouts: We prefer buyouts with value orientation, and those that do not rely on a buy-and-build approach and/or have a record of using leverage to create value. We are looking for private equity value creation from earnings growth and multiple expansion, not an excessive use of leverage.

- Venture Capital: Early-stage venture offers more opportunities than later stage, with more reasonable valuations and upside potential.

- Private Debt: With the right partners, particularly those with experience through cycles and work out capabilities, private debt offers an attractive risk-adjusted return.

- Real Estate: Now is a good time to be a lender, PROVIDED the underlying property is healthy and can manage interest expenses. We also like opportunistic strategies that can invest across the capital stack.

As investors stay the course, we urge our clients to keep the following best practices in mind:

- Do not try to time vintage years. It is important to continue to commit throughout the cycle if you have the liquidity to support these commitments.

- We encourage strategic targets but allow space for opportunistic investments.

- Re-up with strong managers when you can, lest you skip a fund and lose access permanently. If needed, write a smaller check.

- Conduct a pacing plan annually.

- Monitor NEPC’s custom liquidity guardrails regularly to ensure you are not getting in over your head with an uncalled capital commitment.

As always, please reach out to your NEPC consultant for any questions you may have or to discuss your private markets portfolio.

1 https://pitchbook.com/news/reports/q1-2024-pitchbook-analyst-note-surfing-turbulent-cash-flow-waves

2 https://www.collercapital.com/coller-capitals-40th-global-private-capital-barometer-summer-2024/